You can register with http://www.researchbytes.com/ & get all the details.

Posts tagged Value Pickr

Deccan Cement : Dull company.Dull business.Big wealth creation opportunity (05-10-2015)

Both are different kind of plays on the same theme. Sagar is more financially adventurous and aggressive. Deccan is more sedate. It depends on ones own investment comfort which one to choose.

Deccan Cement : Dull company.Dull business.Big wealth creation opportunity (05-10-2015)

Can somebody give some reasons of its clear preference over sagar cements because it’s debt levels are at .42 . So it’s not too high and also pe levels are comfortable .

Deccan Cement : Dull company.Dull business.Big wealth creation opportunity (05-10-2015)

i had visited hyderabad in 2012.

we are travelling from tirupati to hyderabad.its a 12 hour journey but due to strife, the train stopped just outside hyderabad for 8 hours. we need to change the train in between the tracks. our entire schedule got disturbed and we never ever thought of going back again.

so this telangana strife is disastrous. no new power pplants, construction, property market at rock bottom.

it is going to lookup definately.

POKARNA LTD ( Stock opportunities ) (05-10-2015)

I think following are the important things that we have to get clarifications about…

1)Who are the Quartz stone suppliers from India to USA?

2)Whats the current raw material contract for Quartz , who else are the suppliers and how has the company planned to mitigate risk of raw material supply constraints?

3)Among different dealers in US that Quantra sells (Daltile, Bedrosians, IGM, and Oregon Tile) what is their share? Which dealer is the source of increased Quantra sales in last 1 year?

4)Current capacity for Quartz and current utilization?

5)Whats their vision for Quantra brand in next 5 years?

I think they have done a good job of understanding Quartz business, building capacity and developing markets, where will they take it from here is a big question.

I will prepare to write them..

Deccan Cement : Dull company.Dull business.Big wealth creation opportunity (04-10-2015)

leading to increase of price of cement to 320-340 per bag from 220-240.

it is goodd as well as bad

Deccan Cement : Dull company.Dull business.Big wealth creation opportunity (04-10-2015)

i come to my knowledge that a entry tax is imposed on material from telangana in andhra pradesh and vice versa

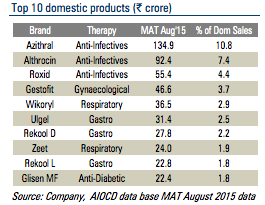

Alembic & Alembic Pharma (04-10-2015)

I see Althrocin in the not-so-good-quality list shared by @wpf123 . This one generates 7.4% of Domestic formulations sales. Not sure if the liquid version mentioned in the list is different from the one in this chart. Anyways, i don’t see any other big pharma companies name in the not-go-good list.

Disc: invested

Kitex Garments Limited (04-10-2015)

Hope management also closes the merger topic and minority shareholders get a fair deal.

Disclosure- invested

Canfin homes ltd (04-10-2015)

It is opening now. Thanks Ayush for sharing the url.

Salient points:

- RBI has reduced risk weight will result in reduction in cost of borrowing and hence conservation of capital, HFC will pass on benefit to borrower

- Avg ticket size 18 lakhs for home loand and 13 lakhs for loan against property

- Interest spread of 2 to 2.5% will be maintained

- They have increased borrowing from NCD/CP 9% to 37% and reduced from banks from 38% to 21% yoy. Further plan increase borrowing from NCD/CP to 50%. This will help margin expansion

- Business is as usual in Bangalore and Hyderabad. Subdued in NCR and Tamil nadu

- 95% borrowers are first time borrowers

- Current GNPA 0.17% NNPA 0%

- Aiming for Loan book growth to 35,000 crore by 2020

- Do not see need for raising capital till April 2017

Disclosure- have some exposure to canfin