Posts tagged Value Pickr

Kilburn Engineering – Huge undervaluation (30-08-2024)

It is the firstview trade that’s been adding from open markets and getting the warrants. But Amritanshu Khaitan does make appearances in concalls also along with Mr Ranjit Lala, if I am not wrong. Thanks for the info.

CL EDUCATE – Less Down side and unlimited upside (30-08-2024)

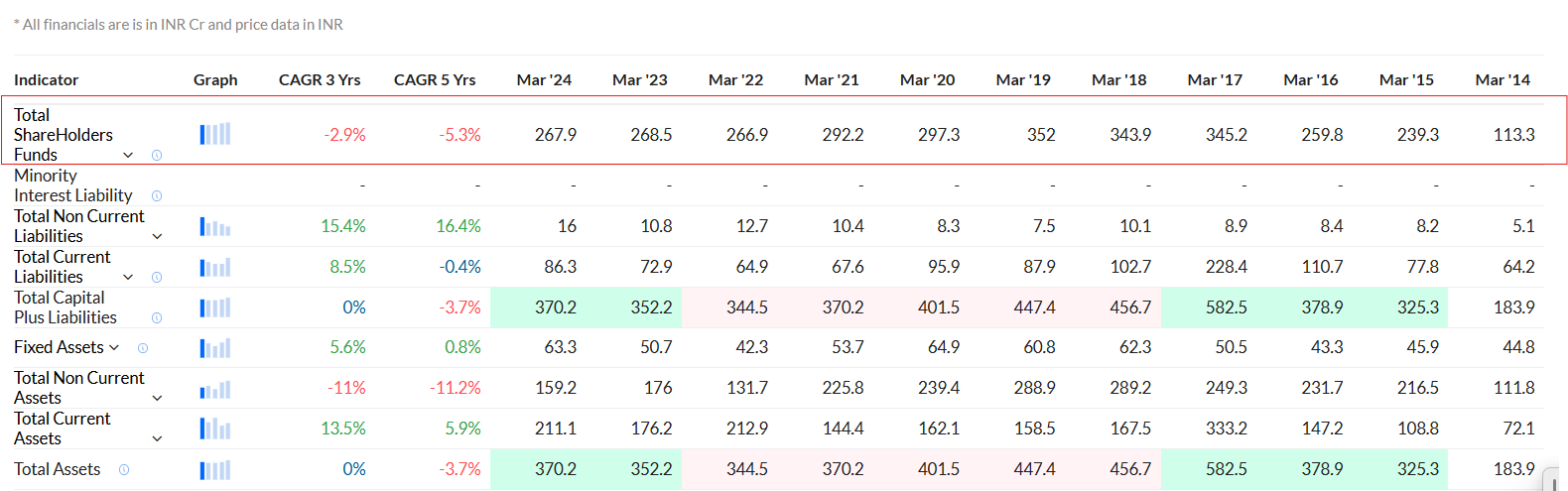

Quick question – why is their balance sheet (shareholder’s equity) not improving over the past 5+ years? Apologies as I didn’t have time to dig into. But would love to hear views if any of you have already analyzed it.

Sterling Tools (STL): Fasteners & EV MCUs (30-08-2024)

`Yes, I have taken a position in the last two weeks. While there is no significant moat here, they have competitive strengths and add products through the JV route.

Buy Unlisted Shares (30-08-2024)

Any one tracking urban tots? Price of urban tots falling everyday…so anyone pls guide me…is this good time to buy? Rsn behind price fall?

Tilaknagar Industries- Potential Turnaround Candidate (30-08-2024)

From recent conference call transcript.

Sterling Tools (STL): Fasteners & EV MCUs (30-08-2024)

They are making the control units and buying + integrating them with the motors. Even that is a specialised job. And their customers have no complaints wrt the MCUs supplied by them

So – that’s where it stands

Sterling Tools (STL): Fasteners & EV MCUs (30-08-2024)

Hi…

Yes – I am holding onto this. Their business is doing well – specially the MCU business. Not sure if they have great technological advantages / other tall entry barriers in this business. However, they do enjoy good customer relationships and first mover advantage. That should be enough to build on from here

Disc : I m biased

Sterling Tools (STL): Fasteners & EV MCUs (30-08-2024)

Sterling Tools –

Q1 FY 25 concall and results highlights –

Revenues – 283 vs 223 cr, up 27 pc

EBITDA – 34 vs 27 cr, up 27 pc ( margins @ 12 vs 12 pc )

PAT – 18 vs 13 cr, up 38 pc

Company is the second largest manufacturer of fasteners and the largest manufacturer of MCUs in India. Has 04 manufacturing plants for fasteners and 01 plant for making MCUs

Results of SGEM ( their subsidiary that makes MCUs – Sterling GTAKE E-Mobility ) –

Revenues – 120 vs 75 cr, up 60 pc

EBITDA – 10 vs 6 cr, up 66 pc ( margins @ 8 vs 7.5 pc )

PAT – 7 vs 5 cr

Company expects that the EV penetration in the LCVs should improve once right products come to the market and that should happen shortly ( like it happened with E- 2Ws ). Company should be a big beneficiary via their subsidiary – GTAKE Mobility

Revenue contribution from top 10 customers in the SGEM is > 90 pc as the E-2Ws and 3Ws mkt is a concentrated market ( with top 4-5 players having lion’s share of the mkt )

Company’s current export share @ 3 pc. Company acknowledges it to be their weak link. They intend to take it up in future

Company has added Hyundai and Kia to their list of customers for their fasteners business. This should give a descent bump up to their base business

Have added E-3W customers to their GTAKE business. That should also help in ramping up their revenues by end of FY 25

Consolidated capex plan for FY 25 stands @ 55 cr ( almost equal split between Fasterners and MCU businesses )

In the EV segment, company aspires to sell additional range of products to their customers wef FY 26 – that should aid revenues in next FY

In the 2W – EV segment, OLA is their largest customer. Company is the single source supplier to OLA electric

An avg MCU costs aprox 8-12 pc of the cost of a two wheeler – depending on model to model

Company is the single source supplier of MCUs for all the 2-wheeler models that the company is supplying to ( this is a big deal – IMO )

Company aspires to be present in all aspects of power electronics and control electronics – as far as EV eco-system is concerned. That’s their ultimate aim and these are the areas where their new product line up will be coming from

Company has announced setting up of Greenfield capacity in India to make magnetic and electronic auto components in a JV with Yangin Electronics. Yangin is a major supplier to Kia and Hyundai Motor companies. Aim to generate a 200 cr/ yr kind of business from this initiative ( inside next 5 yrs ). A partnership with Yangin is expected to help company have firm visibility on orders from the Korean OEMs in India. Beyond the Korean OEMs, company will also target the Indian OEMs for these Electro-Magnetic components

EV business margins are likely to remain in single digits for the foreseeable future

Disc: holding, biased, not SEBI registered, not a buy/sell recommendation

Ranvir’s Portfolio (30-08-2024)

Sterling Tools –

Q1 FY 25 concall and results highlights –

Revenues – 283 vs 223 cr, up 27 pc

EBITDA – 34 vs 27 cr, up 27 pc ( margins @ 12 vs 12 pc )

PAT – 18 vs 13 cr, up 38 pc

Company is the second largest manufacturer of fasteners and the largest manufacturer of MCUs in India. Has 04 manufacturing plants for fasteners and 01 plant for making MCUs

Results of SGEM ( their subsidiary that makes MCUs – Sterling GTAKE E-Mobility ) –

Revenues – 120 vs 75 cr, up 60 pc

EBITDA – 10 vs 6 cr, up 66 pc ( margins @ 8 vs 7.5 pc )

PAT – 7 vs 5 cr

Company expects that the EV penetration in the LCVs should improve once right products come to the market and that should happen shortly ( like it happened with E- 2Ws ). Company should be a big beneficiary via their subsidiary – GTAKE Mobility

Revenue contribution from top 10 customers in the SGEM is > 90 pc as the E-2Ws and 3Ws mkt is a concentrated market ( with top 4-5 players having lion’s share of the mkt )

Company’s current export share @ 3 pc. Company acknowledges it to be their weak link. They intend to take it up in future

Company has added Hyundai and Kia to their list of customers for their fasteners business. This should give a descent bump up to their base business

Have added E-3W customers to their GTAKE business. That should also help in ramping up their revenues by end of FY 25

Consolidated capex plan for FY 25 stands @ 55 cr ( almost equal split between Fasterners and MCU businesses )

In the EV segment, company aspires to sell additional range of products to their customers wef FY 26 – that should aid revenues in next FY

In the 2W – EV segment, OLA is their largest customer. Company is the single source supplier to OLA electric

An avg MCU costs aprox 8-12 pc of the cost of a two wheeler – depending on model to model

Company is the single source supplier of MCUs for all the 2-wheeler models that the company is supplying to ( this is a big deal – IMO )

Company aspires to be present in all aspects of power electronics and control electronics – as far as EV eco-system is concerned. That’s their ultimate aim and these are the areas where their new product line up will be coming from

Company has announced setting up of Greenfield capacity in India to make magnetic and electronic auto components in a JV with Yangin Electronics. Yangin is a major supplier to Kia and Hyundai Motor companies. Aim to generate a 200 cr/ yr kind of business from this initiative ( inside next 5 yrs ). A partnership with Yangin is expected to help company have firm visibility on orders from the Korean OEMs in India. Beyond the Korean OEMs, company will also target the Indian OEMs for these Electro-Magnetic components

EV business margins are likely to remain in single digits for the foreseeable future

Disc: holding, biased, not SEBI registered, not a buy/sell recommendation