Just read an article with an interesting take on financial numbers. Decided to test it on these companies.

Posts tagged Value Pickr

POKARNA LTD ( Stock opportunities ) (17-09-2015)

@Sambath

I find your work outstanding and detailed. And unlike a lot, you do not seem to have a lot of endowment bias and make a balance case for it.

the key will be to find out details of this arrangement with chettinad group for quartz mines. And for the record, chettinad group is very close to AIADMK in tamil nadu. infact, her foster son’s marriage took place in theri schools and offices bringing the entire city to a stand still.

http://www.telegraphindia.com/1150527/jsp/nation/story_22396.jsp#.VfqUQd-qqko

and recently there was a mega raid in their offices

why would someone like that would sell to pokarna at what seems like prima facie, lower than market price is not something I have an answer to.

Accelya Kale Solutions-Niche & Sticky Business (17-09-2015)

Yeah, it can qualify as a good patient bet.

Disc. Not invested. This is not a recommendation.

Accelya Kale Solutions-Niche & Sticky Business (17-09-2015)

The management is highly ethical. My whole bet is that whenever there is a CEO change things do get shaken up a little and the new CEO wants to prove his/her mettle, especially if working under the guidance of the founder. In this case, theres a change that’s happened and for what’s worth, tail winds do exist and the only variable you need to track in this business is growth – since it’s a sticky, high margin, high EBITDA, recurring cash flows business.

I prefer to take those kind of bets – where there’s very little to lose and all to gain,, even if wait takes a little longer. I had the same thesis on infy when vishal sikka took over and so far it’s been proven right.

Varun 2020 portfolio – 2 strategies (17-09-2015)

Totally Agree Varun.

Yesterday’s winners identified by our esteemed senior boarders are not going to continue to give the same quantum of returns for the next few years as most of these names(Ajanta, Mayur,etc) are well discovered and trade at lofty valuations(Ajanta, Mayur were discovered @ single digit PE when our boarders identified them).

It is important to come out of the comfort zone to think of what may work tomorrow. It’s easier said than done. In my own PF, 60% of the names are Valuepickr top picks.

Thanks,

Ravi S

MM Forgings- May shape the portfolio in the right way (17-09-2015)

Hi Gaurav,

I agree with you that the volume of shares traded for a small cap company will always be less (atleast in the beginning). However that also increases the doubt that whether the price is operator driven or not. I think one way to check is that % of deliverable quantity(see link below) should be atleast >75% in such small companies. For MM Forgings it seems a bit low.

Varun 2020 portfolio – 2 strategies (17-09-2015)

Vivek – First of all Thankyou

Two reasons I got of Syngene – firstly I already have 4 other pharma stocks crossing almost 24% of my portfolio – as a rule I follow that no sector should cross 25-30% exception being financials and consumers

Secondly Syngene at 350 to me seems to be pricing 3 yrs ahead of good growth so margin of safety was not there and I needed to raise cash levels to buy into Supreme Inds and Care ratings

Probably at 300 or so and when I have better cash availability I would dig into it again – I absolutely love the stock and wont advise you to sell it unless you find a much better opportunity

Tata Elxsi – I bought at 600 levels – missed at 230 odd when I first looked into –

1989 established- 25 yr old, Debt Free, 50.09 promoter share is ok, Avg ROCE of 52% is excellent, ROE of 36% is excellent, MCap < 1900 crores when invested, Theme – NICHE IT player in new technologies like Embedded product design, Industrial design (product design, branded graphics and user interface systems), VLC and systems integration, Providing software development and system design services for automotive and aerspace industry – connected cars with in vehicle infotainment, active safety systems, telematics, powertrain and hybrids as theme is a big theme, Also complete product development lifecycle from R & D to services in broadcast consumer electronics segment helping them reducing enginerring costs, Huge opportunities due to advent of Internet of things, recent addition as a core industry is healtcare with started working on medical electronics like patient monitering devices, diagnostic devices and theuraptic devices- huge growth potential, unified communications like video and audio conferencing, tele presence etc, also identified new areas like semi conductor and chip design, new theme going ahead is convergence of consumer, markets and electronics to be one of the biggest disruptive changes which will throw up lots of opportunities for Telx

MM Forgings- May shape the portfolio in the right way (17-09-2015)

Hi Shivansh,

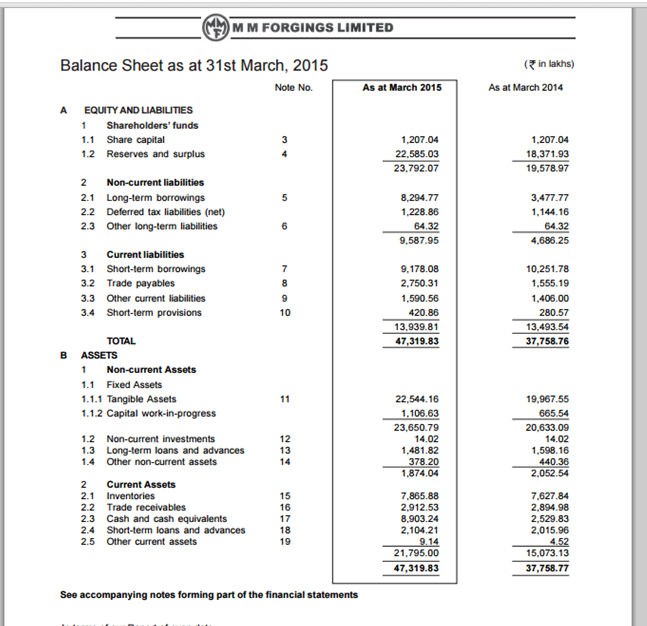

Thanks for your insights. I could not find Consolidated numbers on money control for 2015. Please find below the snapshot of current year Balance Sheet. 89 Cr is present as Cash and Cash Equivalents.

Please also find below link of the Annual Report for better understanding:

http://www.moneycontrol.com/annual-report/mmforgings/MMF/2015

I am not expert on Value Creation stuff. Can you please define more of that?

CLSE – the next KRBL? (17-09-2015)

I appreciate the logical way though which you saw the traded goods being significant and checked the shipping bill details. The indicator for the same gimmick are the small font,without coma used for the line item ” purchase of stock in trade” as compared to the cost of material consumed and the ratio of inventory to receivables. For this company it is close to 1.5 for LT Foods it is about 4.3 and for KRBL it is around 6. The other interpretation could be it could be trading, but since the shipping bill says a different story, even if it is to a small degree, it shown deceiving traits.

CLSE – the next KRBL? (17-09-2015)

I appreciate the logical way though which you saw the traded goods being significant and checked the shipping bill details. The indicator for the same gimmick are the small font,without coma used for the line item ” purchase of stock in trade” as compared to the cost of material consumed and the ratio of inventory to receivables. For this company it is close to 1.5 for LT Foods it is about 4.3 and for KRBL it is around 6. The other interpretation could be it could be trading, but since the shipping bill says a different story, even if it is to a small degree, it shown deceiving traits.