Posts tagged Value Pickr

Varun 2020 portfolio – 2 strategies (16-09-2015)

HI @varvp14

Your stock selection is very good can you tell how do you decide the price levels. I am novice and your comments might help me a lot. Thanks in advance

Query about spinoffs/de-mergers (16-09-2015)

This might be a very basic question. I was wondering if there is a way in which I can be up to date with the spinoffs / de-mergers scenario. Like arvind infrastructure at the moment, marico kaya in the past etc. Is there any website or tool which will tell me about the recent spinoffs/de-mergers and the upcoming ones

Thanks

MM Forgings- May shape the portfolio in the right way (16-09-2015)

This is my first post on ValuePickr so all the veterans please advise, if anything is missed out to start a new discussion.

MM Forging seems to be a good story in the making.

The Company was originally started in 1946 as ‘ The Madras Motors Ltd ‘ as an importer and distributor of the products of Royal Enfield Motors from UK. The current forgings business was started in 1974 and later stopped the dealership of Royal Enfield in 1990 and decided to concentrate solely in forgings production. (Focus in one domain)

MMFL now producing forgings mainly for auto , engineering and oil industries . The Company has increased its forging capacity step by step and now operating four factories in Tamil Nadu. The Company is one of the largest forgings exporter from India and more than 70 % of total income is currently coming from exports.

Below chart clearly shows good signs of dividend and two time bonus of 1:1 clearly indicates shareholder friendly Company practices across 15 years of time span:

In my opinion, following are the positives:

1) Good Cash sitting in balance sheet for current year;

2) Sales and Net profit has almost doubled in 5 years; and

3) Profitability ratios in mid teens year on year and improving.

In my opinion the following are concerns:

1) Volume of shares traded – But I think for small cap that will always remain a question; and

2) Debt has increased year on year.

CMP around 520, 52 week high @ 751, 52 week low @ 421

Discl: Not invested yet but seeing the growth prospect coupled with Shareholder friendly practices tempted to invest.

Veterans – Please share your opinions.

Regards,

Gaurav

Page industries (16-09-2015)

Sumit, Page in 4 digits. I thought 13400 was a good price some time back. Had bought some then. So much of FII holding and if they start to unload then why not…

Lawreshwar Polymers (16-09-2015)

Recently share price is moving fast..is there any updates..

Price moved up 4 times from my original recommendation but financials are not picked in the same manner,

currently valuations are stretched and thinking of exiting..any opinions..

REPCO home finance – another Gruh in the making? (16-09-2015)

“Mr. Varadarjan said that the Central Registrar of Cooperative Societies, a few days ago, had decided to give option to multi-state cooperative banks to relax the superannuation age of MD/Chief Executive Officers from 60 years to 70 years with the approval of Boards of respective institutions.

Repco Bank is one among the two such multi-state cooperative banks in Tamil Nadu coming under the option, which was aimed at retaining talented persons at the top.” – The Hindu August 20 2015

Hope that clarifies the MD issue(for repco bank).

CLSE – the next KRBL? (16-09-2015)

Very True..

But tht’s the reason behind such healthy BS of CLSE

1…CLSE is doing Asset Light Business

2..ie…Procuring Rice from domestic market without setting up Rice mills and selling in International market at premium

3..CLSE clearly states they will spend on Marketing now own-words to improve brand Value of Maharani Rice ..Agree it can not be Compare with KRBL or LT foods

4..CLSE operating cashflow Fy 15 is 20 cr against -21 cr

5..Only play in CLSE is Low Valuation, Increase in Export,Opening in Iran Market,& Healthy BS

6..Dont expect returns like KRBL its altogether in different League

(Invested at much Lower Level)

CLSE – the next KRBL? (16-09-2015)

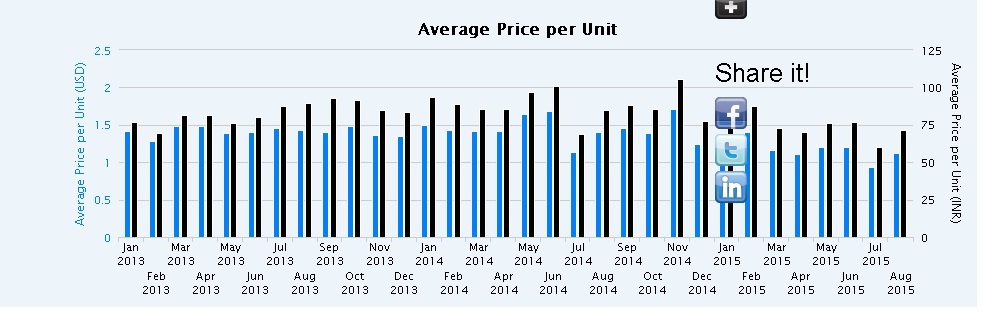

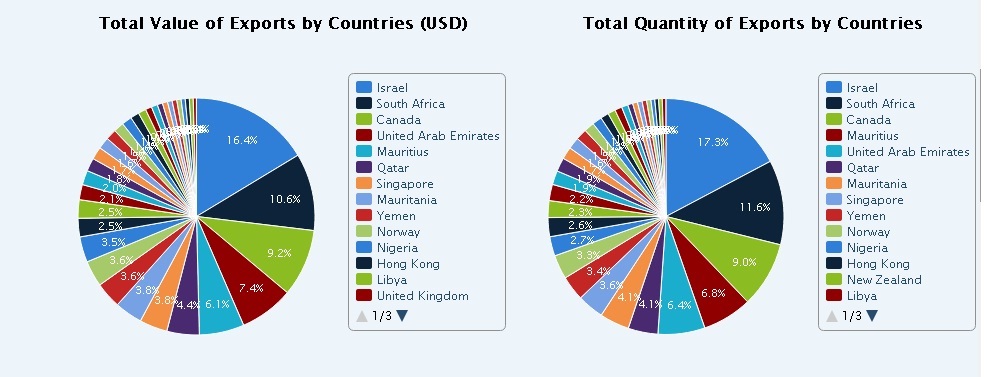

1..Chamanlal’s Maharani Rice Export Data :-Showing Increasing Trend YoY

2..Chamanlal Increase its production (Not Capacity) by 35 v% in fy 15

3.Only Concern with CLSE is decrease in Realisation ie..per unit export price showing declining trend but it is compensated with increase in volume

4this is part of commodity business

(Dis:- Holding at much lower level)