Sorry Ravi, can’t help there since I’m from Maharashtra.

But it shall be easy to find out the prices. All one needs to do is visit a retail shop pretending to be a customer.

Sorry Ravi, can’t help there since I’m from Maharashtra.

But it shall be easy to find out the prices. All one needs to do is visit a retail shop pretending to be a customer.

dinakaran,

As far as I recall PI Inds ROE have been in the range of 30%. Where did you get those figures? If they are from any sites like moneycontrol u need to verify again.

Best way of calculating these ratios is thru figures provided in Annual Reports or Statement of accounts provided in annual and six monthly results.

I am not able to post this in Kitex thread as it is undergoing maintenance. Kitex is indirectly involved in Panchayat politics and has supported formation of an independent party by name Twenty20. The panchayat elections are scheduled to be held in Nov 2015. The Kitex MD Sabu Jacob has nurtured this political independant outfit from grass root level by supporting them at various levels to raise their standard of living and from what I understand he has very good support from common man in that Panchayat. I think Sabu is taking a calculated risk here. None of the mainstream parties support him openly. They can’t oppose him openly as the general public have recognized his contribution. If something goes wrong with the plant there, I am sure the political parties won’t support him. Is there any other business doing similar work? As an Investor I am worried about the outcome. I will appreciate if anybody could share their thoughts on this.

Thanks @NikhilJain

Since you had mentioned that your father is in cement retail business, what are the current price trends? Are the prices stable/have they corrected? (in case you are from south)

I agree that this is an opportunistic bet as NCL looks mis-priced at current P/E and not a long term growth story.

Thanks,

Ravi S

hi

If u look at q1 results which had a lot of revenues coming from US, the following is the composition of revenues

US 46% 880 cr

India 25% 490 cr

Brazil 7% 134 cr

Eurpoe 12% 230 cr

ROW 5% 90 cr

Now coming to Brazil, how much the currency depreciates is to be monitored and then one has to think about what kind of problem torrent could have. Luckily for the company, this Brazilian thing comes at a time when US and Indian markets are firing on all cylinders for the co. And hence the actual impact shold be negligible. But if this problem continues beyond fy 16 then next year US may not be such a huge contributor to overall revenues and then the Brazil contribution could increase. But for that management has some time to react and take remedial action.

Another interesting aspect for this year is that

if u look at consolidated figures, PBT was 859 crores on which co paid a tax of 410 crores. (this is due to regulatory requirements bcos whatever is shipped (even though it is not recognised as revenues prior to actual sales) entails tax payment.) Management has categorically stated in concall that tax rate will be as per earlier year on an overall yearly basis. So till the company makes PBT of around 2050 for the year, it will need to pay a tax of 410 crores on ball park tax rates of 20% as per last year. Now co has alread paid the 410 crores and hence the incremental nearly 1200 crores of PBT will not attract much by way of tax and hence the figures for next few quarters could look much better than expected.

disc: invested.

For any company, a balance sheet shall show total assets being equal to total liabilities. That’s why it is called a balance sheet.

If total assets are not exactly equal to total liabilities, you have an imbalanced sheet.

Thanks for doing the dirty work @ravimba31.

I wanted to start a thread on NCL but I’ve been too lazy to follow.

Anyhow, I’ll add some info as I’ve understood so far.

NCL also sells cement in other south states viz Karnataka and Tamilnadu. These two states have shown good retail demand in last few quarters according to K Ravi (MD).

Secondly, q2 being monsoon season may show lower sales as well as price realizations. At least that’s what I have witnessed in my father’s cement retail business, so far.

q3 and q4 are generally better than q2 for domestic cement industry.

There are rumors(?) that AP/south cement companies won’t opt for capex in near future, by mutual understanding. Need to verify this. If this is true, we have a pretty high MoS.

Lastly, there have been more than one instances in last couple of months when promoters have released their pledged shares. Latest being today itself. This is a positive in my stock picking method.

Disclosure :- This is held in my portfolio as an opportunistic bet. My views may be biased. Please do your own due diligence before buying or selling this stock.

ROE for PI industries has been shrinking over the recent time. Could some one please explain why it does not affect the share price?

ROE:

65.23 57.39 56.56 39.34 34.74 13.15 17.26

About The Company:

NCL Industries (NCL – Nagarjuna Cements Ltd) started in 1984 is a predominantly-cement company with its Cement plants in AP & Telangana. They have other business segments, but the revenue contribution from other segments is not meaningful.

It has five business segments –

1. Cements (81.56%)

2. Boards (11.86%)

3. Ready mix concrete (5.71%)

4. Energy (0.82%)

5. Prefab (0.05%)

Cement has been their mainstay and even if we look at the average revenue contribution for the last five years, the average is about ~80% from cements segment. Their sales is predominantly through the retail network, and their current dealer numbers stands at about 1500 dealers. As with any retail oriented business, they collect deposits from these dealers(interest payable @ 6%) before enrolling them.

Capacity:

They have a total of 2 million ton capacity. Capacity utilization for Q12016 was about 62%. This # looks optically low because NCL had shut down its plants during the first quarter to take up repairs and maintenance. (Per the company MD, they weren’t able to take this up during the last 2 years as they were facing difficult times financially). The company is looking at 75% capacity utilization for the full FY2016.

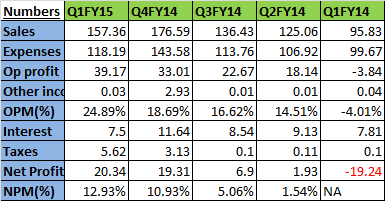

Here is a snapshot at their numbers for the last 5 quarters: (Sourced from Screener.in)

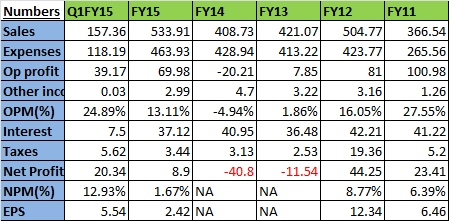

Here is a snapshot at their numbers for the last 5 years: (Sourced from Screener.in)

AP Cement Industry in FY14 & FY15:

Andhra Pradesh’ total cement capacity currently stands at 15 MT. Cement industry in the erstwhile AP underwent demand compression as political unrest, and societal disturbances due to bifurcation of the state, took a toll on the construction activity. As a result, Cement companies in this region, had sub-par capacity utilization for FY 15, & FY 14. As a result of this, there was a significant negative impact on cement demand, and hence cement companies from this state – Sagar Cements, Deccan Cements, KCP & NCL had a tough time in these two financial years. During these two years, the B/S of these companies worsened, and there was no incremental capacity addition in these two years.

NCL in FY14 & FY15:

NCL has a ~ 13.33 market share by capacity in AP. Due to the reasons discussed above, NCL reported poor set of numbers(refer to the above table) and in fact it was unable to service the interest obligations, and the company went into CDR – Corporate Debt Restructuring. It restructured its entire outstanding debt on July 2013(except 7.23 crores), to be repayable in 28 quarterly instalments starting from March 2014.

Current state of the AP Cement Industry in FY2016:

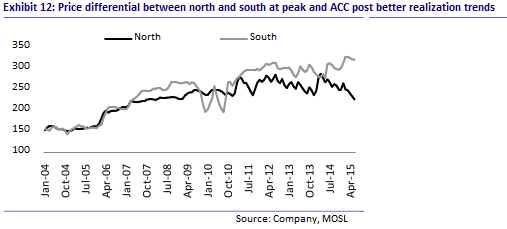

Now with bifurcation of the state over, construction activity has started picking up and as a result of which, Cement demand & prices have started improving. Please refer to the MOSL report which shows the price trends of cement prices in South. All the cement companies in this region have started reporting better numbers. -> The current cement price stability/improvement is attributable to absence of capacity addition in above 2 years & also due to inability of these companies to add capacity as their balance sheets were battered. (classic case of demand vs supply equation)

NCL in Recent Quarters:

NCL has turned around last september, and the full impact of the demand and improved prices are visible in the performance of NCL in the last 2 quarters. In the current quarter, their topline grew 65% and the company reported an operating profit of 39.14 crores. NCL also took up repair works in the last quarter which impacted their capacity utilization. Promoters recently infused capital by having a preferential issue of 17,95,455 shares, as per the terms of CDR.

CMP – 90

EPS TTM(Diluted) – 13.2

P/E – 6.89

EV/Tonne – Rs. 2600/Tonne(or ~$40/Tonne)

If the cement prices were to remain stable at the current levels in AP, and if NCL has a 75% capacity utilization as guided by the management, we are looking at ~ 4PE (at CMP) at the end of FY16.

The above #s were the key reason why this stock interested me. At a P/E(TTM) of ~7 and EV/Tonne of about ~$40, there is a reasonable Margin of Safety. But, what could make a mockery of this MoS? Here are some risks:

Cement price correction in AP – The probability of this risk materializing is low for now as the below articles show that cement demand is still intact in AP. This demand scenario might turn very quickly if many of Central + State government’s projects turn out to be mere announcements. – A case in point being smart-city project which is yet to take-off.

http://www.thehindubusinessline.com/companies/cement-sector-upbeat-as-telangana-ap-set-to-buy-3-million-tonnes/article7562242.ece – This article highlights the government’s(AP + Telengana) intention to procure 3 MT of cement.

http://www.motilaloswal.com/site/rreports/HTML/635756587693471670/index.htm – This article highlights the price trends in South.

Company’s culture of funding growth through debt – NCL historically has been a company which has been reasonable levered. In one of the recent interactions, management had commented that it was looking at getting out of CDR by July this year. Apparently they decided against this. A company in CDR, faces a lot of restrictions/controls on capacity expansion, imposed by the lenders. NCL wanted to expand capacity but they were unable to do so, as they are currently in CDR. – This is a big risk to me as the culture of taking debt to fund growth is detrimental.

@NikhilJain, I liked this pick after you had commented in one of the other threads that you were taking positions in this. This is a quick attempt at explaining the stock story – Please cover any opportunities/risks that I may have missed out.

Thanks,

Ravi S

Disclosure – Invested, My views may be biased. Please do your due-diligence.

Whats the view on the stock due to Brazil exposure ? It has around 13% sales from the region. Have not looked the at company closely but liked its last quarter numbers. So does the current fall in price a good entry point .