@jigar_punamiya ,

Since they are in manufacturing business, yes it is capital intensive.

Your assumption is true and company had spent 9cr in acquiring land from GIDC and awaiting govt approval for the same.

Posts tagged Value Pickr

Dynemic Products (08-09-2015)

Avanti Feeds (08-09-2015)

Such negative publicity is not good for the industry given that it is election time in USA. It’s the time when trade protectionist voices get stronger and politicians tend to agree with them.

Avanti Feeds (08-09-2015)

Such negative publicity is not good for the industry given that it is election time in USA. It’s the time when trade protectionist voices get stronger and politicians tend to agree with them.

Dynemic Products (08-09-2015)

Hi All,

Took a cursory look at this company on screener. If one observes the cash flows over last 10 years,

1. It has generated CFO of about Rs. 31.7 Cr. where as its capex is about Rs. 45.9 Cr.

2. Also, borrowings have increased over the years.

3. CFO over 10 years (Rs. 31 Cr) < Net Profit over 10 years (Rs. 41 Cr). Shows that lot of funds have been stuck in working capital.

Therefore, it seems to be a cash guzzling business. I am very skeptical about such businesses, which always require outside funds (debt/equity) to fund growth, which eventually does not convert into cash.

Let me know if I am missing something.

Dynemic Products (08-09-2015)

![]()

Recently i had spoken with couple of issues from management and here is the update

1. Current year there is inventory buildup 6.9 crores in 2015 why are you looking for setting up 3rd plant

Reply: The stock is mainly of Dye Intermediates finished goods due to slow market of Textile dyes. Please note that if market is slow right now it will not remain same always and we cannot stop from expansion and growth phase. Please note that Synthetic colors are stable less expensive than natural colors and much in demand so right now there is no threat to the Company.

Company skipped dividend because it plans to complete unit3 phase1 expansion in the current FY.

I calculated the Inventory Turnover ratio and it is coming > 2 indicating that company is able to generate 2rs sales for every one rupee of inventory. Management is also very good and a small debt on books with mouth watering valuation.

There is a good demand for synthetic colors from nestle,pedigree etc..

Source: Previous 4 years annual report.

Disclosure: Bought today @ 40 levels and increased my holding

Avanti Feeds (08-09-2015)

A perspective on US Shrimp consumption.

Dynemic Products (08-09-2015)

Thank you chaitanyak.

Can you please provide me some links related to pollution norms in europe and usa.

My richdreamz portfolio – visit my portfolio to learn together! (08-09-2015)

Absolutely nice time to shuffle your portfolio as I was indicating.

I have moved a wee bit from Page to PI Industries just to even out a bit on the allocations and as I build my conviction on PI.

I do not generally hold cash and stay invested 100%. So at these times, the best I could do is sit silent if my portfolio allocation is as per my expectations or tinker it to suit my required target.

As per the observation it looks like though the market levels have stabilised, price damage is happening is few stocks.

My disclaimer holds as always. I think there should be a thread level disclosure so members need not mention their disclosure with every post.

CAREERPOINT — double bottom confirmation (08-09-2015)

anybody attending forthcoming agm on 26th september.

Towards a Capital Allocation Framework! (08-09-2015)

A very good thread!

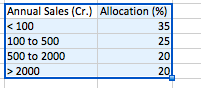

I have been struggling with capital allocation over last 2 years. This thread helped a great deal to put some structure to capital allocation. And then an idea appeared to me after discussion with friends. The idea is to look at Annual Sales of companies and use that in capital allocation.

e.g. something like this:

The simple idea is once you become big – you are going to run into hurdles for next phase of growth and upside may be limited. There will always be exceptions to this. Opportunity size is one factor in above discussion that covers above topic well but still when you grow above a certain size (2000 Cr is my threshold, it may be different for you or even based on industry), you have to work extra hard to get to maintain same % of growth.

Current rule I follow is, once company crosses 2000 cr, mark, I stop adding the new positions (but continue to hold previous position).

Within these categories, I follow excellent VP model which ranks stocks based on CR and VR. i.e. these categories are after we are convinced about Business Quality, Management Quality, Valuation etc.

Views invited.

Thanks,

Rupesh