Thanks Sumit for elucidating your thesis on Anand Rathi. I had guessed that trust would be a factor as people do not give their money to people they do not trust. However, the asset light model and the dependency of other financial companies on debt or the stock market was news to me

Posts tagged Value Pickr

Tracking Special Situations (29-08-2024)

@Vishal_Jajoo Can you please help where we can check the acceptance ratio, once the offer is closed? Any link for BSE / NSE?

Sumit’s Portfolio (29-08-2024)

I am curious about Transteel as well.

My trouble with this company is that its difficult to track how well are they growing. The last order notification was of June 12th.

The Space as a service sector is booming and that makes me feel that Transteel will benefit. But i can’t exactly figure out if that is actually going to be the case or not. Good thing is that they are out of hyderabad and Hyderabad is has a huge commercial space under development.

Regarding end to end service: It is not an uncommon service. Most of the players provide this.

Google maps review are bad: Google Maps (blr), Google Maps (chennai)

Eldeco Housing and Industries (29-08-2024)

Harsh,

- These are some facts that I came across while researching about the company.

- These are more facts and less opinions.

- Previous posts do not talk about unrelated firm called Eldeco real estate limited.

- Previous posts do not talk about cheap interest rates on loans.

- Previous posts do not talk about the ownership of brand trademark.

- Multiple previous posts are expressing opinions on promoter group, even calling it “shady”.

- I dont think it is illegal to form opinions based on facts.

Tejas Networks – Product based IT business in a favored sector? (29-08-2024)

Intel’s decision to cut 15% of its workforce could significantly impact its telecom business, particularly in the Open RAN segment, where key customers include Nokia, Ericsson, and Huawei. Intel dominates the chips market, holding a 99% share of all virtual RAN deployments as of early 2023. This workforce reduction could weaken Intel’s stronghold in the Open RAN market, valued at around $40 billion in 2023. This situation could create favorable opportunities for Tejas in the coming years.

https://www.lightreading.com/open-ran/an-intel-crisis-is-a-crisis-for-open-virtual-ran

Eldeco Housing and Industries (29-08-2024)

I am sharing few facts that i came across while reading about some of the projects of Eldeco.

This is a project in Noida

First i was happy that Eldeco is doing a project which is selling it around 10-11000 per sqft.(checked offline)

After taking a closer look came across this

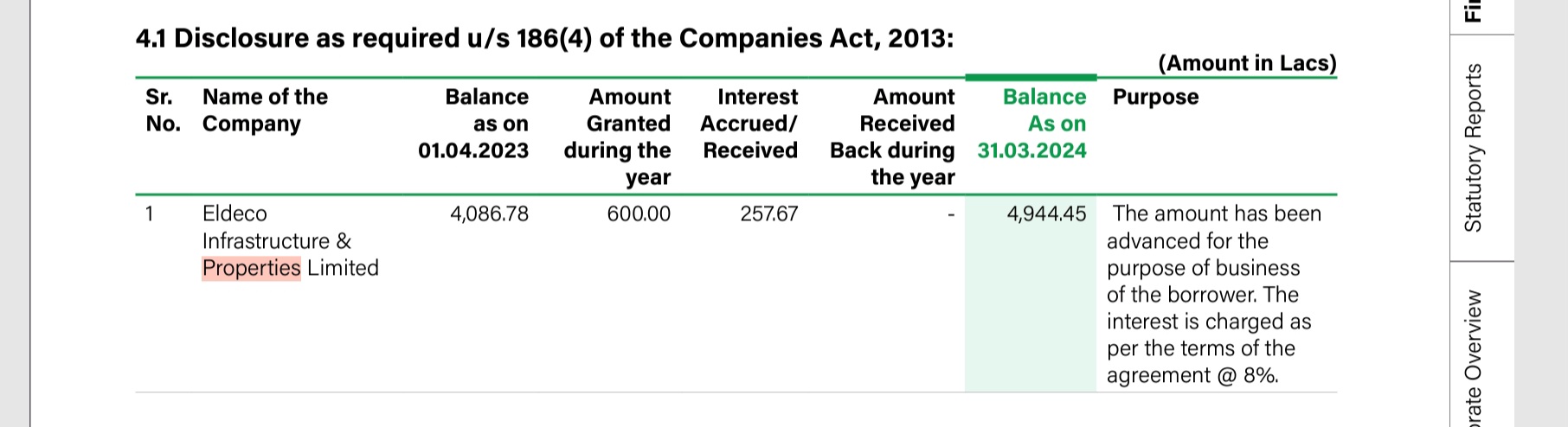

This project is using ELDECO brand name but is not a subsidiary of the listed entity. It is a separate company called Eldeco infrastructure and properties limited having the same KMPs.

Reading through the annual report, i found that this company owes ~50 crores to the listed company and accrues interest at 8% pa.

8 percent!!!

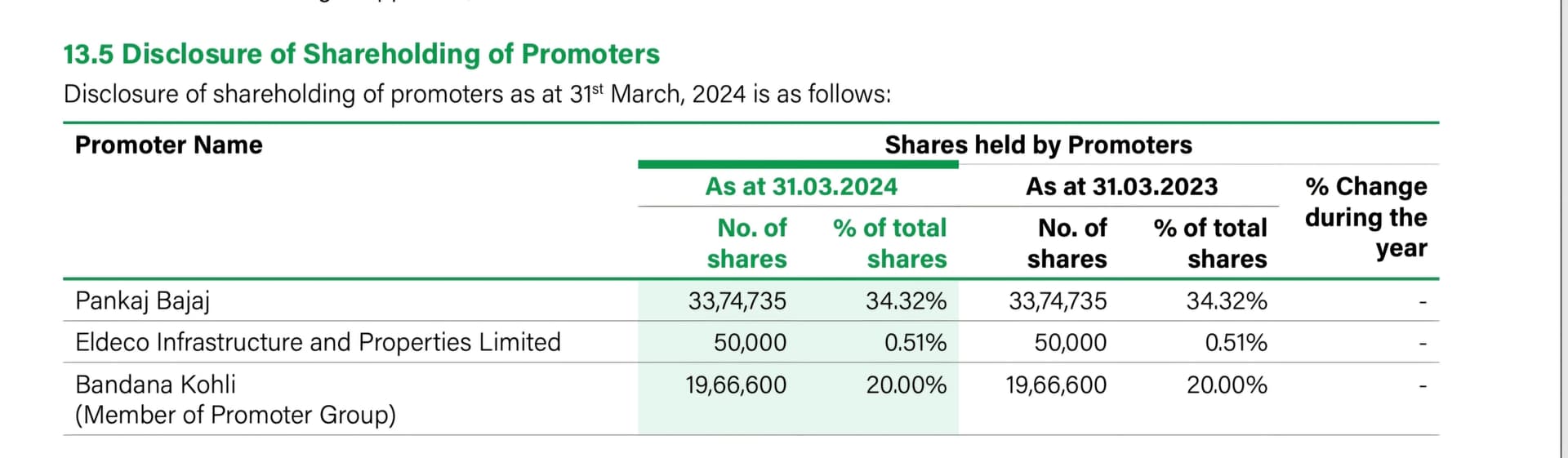

Also this 3rd party companies owns 0.51% stake in listed company. Which roughly translates to 50 crores.

Speaks a lot about intention. The related party could have sold its 0.51% stake to repay that cheap loan.

One more mystery that i encountered was eldeco la vida bella project.

This project is on their website. This project is currently quoting 10,500-11,500 per sq ft in market.(checked offline) But the promoter of this project is entirely a new firm called Eldeco Real Estate ltd, which is neither subsidiary nor related party as per annual report of the listed firm.

Tens of high realization projects are being done outside of the listed entity and all are using ELDECO brand name. As per zauba, the directors of this company are not KMP of the listed firm.

https://www.zaubacorp.com/company/ADHIKARI-INFRASTRUCTURE-AND-BUILDERSLIMITED/U45400DL2007PLC163848#:~:text=Directors%20of%20Eldeco%20Real%20Estate,Gupta%20and%20Vimal%20Kumar%20Behl.

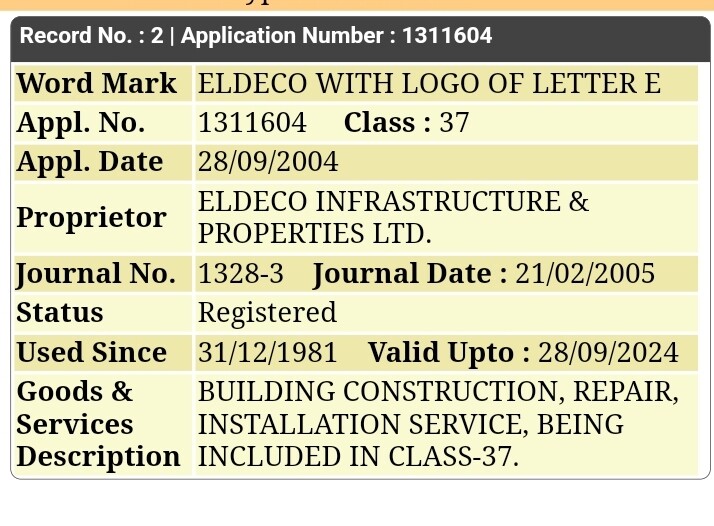

Then why this project is listed on Eldeco group website? Why are they using same logo? According to govt data eldeco trademark is owned by the listed firm

No royalty is being paid to listed firm either from related party (Eldeco infra & properties ltd) or the unrelated party (Eldeco real estate limited).

These are only 2 projects that i have discussed. Please do your own research before trusting your money with such promoter.

Rajesh’s portfolio (29-08-2024)

Key is to enter stocks before they run, may like to study K2 infragen and cellecor gadgets both have guidance of 100% CAGR and have not run much

Sumit’s Portfolio (29-08-2024)

Warren Buffett has famously categorized businesses into three types: Great, Good, and Gruesome. Great businesses require little to no capital to grow (asset-light) and generate consistently high returns on capital while maintaining a durable competitive advantage. Good businesses deliver reasonable returns on capital but demand ongoing capital investment to fuel their growth. Gruesome businesses, on the other hand, are capital-intensive and produce poor returns on capital.

In this framework, Anand Rathi Wealth Limited stands out as a Great business. It operates with an asset-light model, demonstrates a high return on capital, and benefits from a robust competitive edge in the wealth management industry.

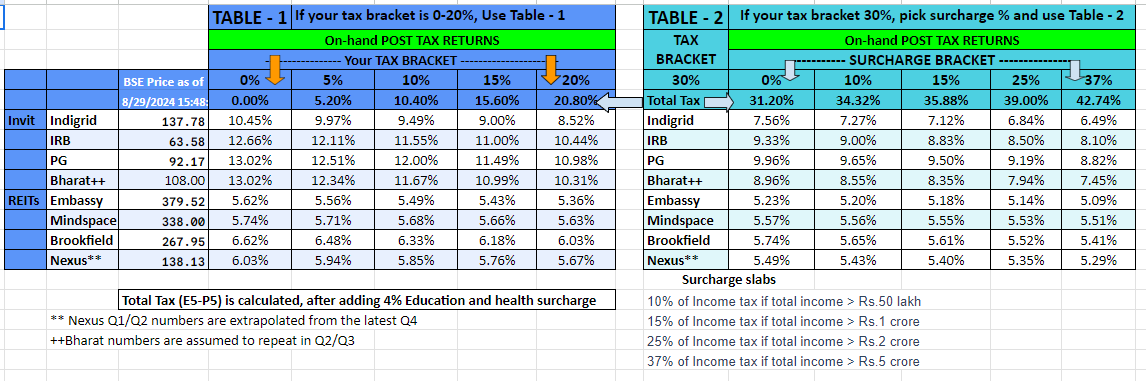

Indigrid InvIT: High yield on stable and predictable revenues (29-08-2024)

I have added Bharat Invit (assuming that the remaining quarters, will continue with same distribution, as their recent annoucement…in fact, that is their guidance as well) to the table

IRB INVIT TRUST- new game in the town! (29-08-2024)

I have added Bharat Invit (assuming that the remaining quarters, will continue with same distribution, as their recent annoucement…in fact, that is their guidance as well) to the table