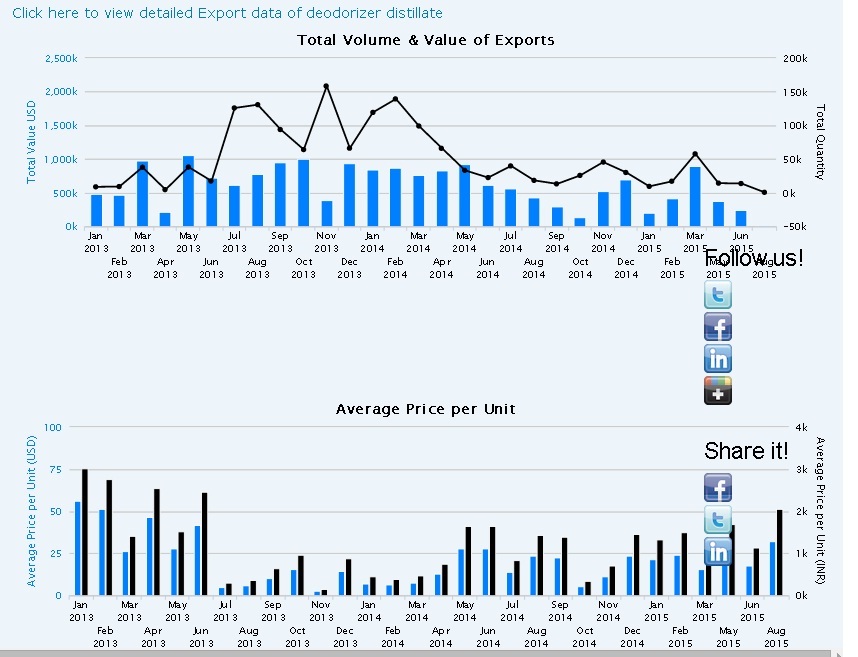

Adi Finechem exports DEODORIZER DISTILLATE (MIXED TOCOPHEROLCONCENTRATE) WITH 08.35% TOCOPHEROLS.

When I check export data it shows declining trend. Adi might be loosing market or demand for there product might be decreasing

Posts tagged Value Pickr

Adi Finechem- A good business or business having a good time? (27-08-2015)

P. I. Industries Ltd. – A Unique Business Model can make it a Great Play on Agri & CSM Space (27-08-2015)

I don’t know if PI discloses client dealings. In general, absence of merger is actually a good thing for PI since both companies will pursue R&D efforts separately.

POKARNA LTD ( Stock opportunities ) (27-08-2015)

Thanks Sam for your effort! looks promising

Disc: invested and added in the current dip

Aurobindo Pharma (27-08-2015)

Aurobindo Pharma receives USFDA Approval for Entecavir Tablets

Entecavir tablets are used to treat hepatitis B infection.

Aurobindo Pharma has received the final approval from the US Food & Drug Administration (USFDA) to manufacture and market Entecavir Tablets, 0.5mg and 1mg.

IMS data suggest, entecavir has an estimated market size of $294 million for the 12 months ending June 2015.

The company has now a total of 209 ANDA approvals from the US FDA.

entecavir approval.pdf (74.9 KB)

Ambika Cotton Mills (27-08-2015)

Hi Rohit – Agree that this will still be capex. But the point i am making is that it is not maintenance capex. On another note, this capex was not mandatory. An option available to Ambika mills was to go for a dedicated feeder and enter into a PPA with another wind power generator and simply buy wind power. Thus capex was not necessary.

This capex allowed them to improve their operating margins in long term and need to be viewed accordingly. Historical rate of increase in electricity tariff in India is 5.5% (CEA data). Few years down the line the wind mills will help in significant power reduction costs.

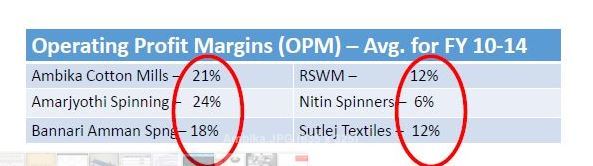

On a side note – As per an analysis that I have done on some listed companies in textile space, OPM for textile companies that have their captive wind projects is much higher for textile companies that do not have a captive renewable energy source. Companies on left have captive wind mills whereas companies in right do not (except RSWM which has commissioned a 20 MW wind mill an year ago. However even this 20 MW is equivalent to 4 MW of thermal power project. their existing thermal power project is of 50 MW. I am assuming therefore the impact is not much in this case even after having a windmill

Ambika Cotton Mills (27-08-2015)

A friend of mine called up and said as per his estimates Ambika cotton consumption is 10% of total production of Pima and Giza variety. I did my calculation independently and came to about same conclusion.

It’s quite possible that there is some error in the way I am looking at the data.

If not then we should worry about 1) opportunity size and possible growth going forward [Am looking beyond 30K spindles capacity expansion] 2) Availability of cotton itself owing to severe drought in California [it produces > 90% of US Pima cotton production]. In 2015 area under Pima has declined from 2 to 1 Lakh acre [read this article http://www.nytimes.com/2015/08/08/business/a-once-flourishing-pima-cotton-industry-withers-in-an-arid-california.html?_r=1] . Even in Egypt area under Giza cotton is declining due to removal of subsidies on cotton. [http://english.ahram.org.eg/NewsContent/3/12/119530/Business/Economy/New-subsidy-cut-may-be-the-end-of-Egyptian-Cotton.aspx]

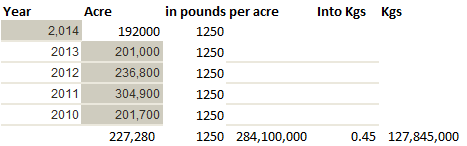

Here are my calculations:

For USA

So US is around 13crs Kg . See this link for US area under PIMA cotton http://www.supima.com/view-reports/acreage-estimate/ . Pounds per acre is from NYT article referred above.

Egypt produced 370,000 bales during 2014 . One bale = 225kgs. This amount to 8.3crs kgs

[see this link http://gain.fas.usda.gov/Recent%20GAIN%20Publications/Cotton%20and%20Products%20Annual_Cairo_Egypt_3-30-2014.pdf] 90% of Egypt cotton is extra long and long staple variety.

So Pima + Giza amounts to 21crs kg for 2014. As per Ambika website cotton consumption for 2014 was 1.89 cr kg and for 2015 2.23cr kg. So as per my estimates Ambika is already consuming around 10% of global production. Atleast for next 2-3 yrs it seems global production is not going to increase. So to repeat 1) Opportunity size ???? 2) Availability of cotton ????

Ambika Cotton Mills (27-08-2015)

A friend of mine called up and said as per his estimates Ambika cotton consumption is 10% of total production of Pima and Giza variety. I did my calculation independently and came to about same conclusion.

It’s quite possible that there is some error in the way I am looking at the data.

If not then we should worry about 1) opportunity size and possible growth going forward [Am looking beyond 30K spindles capacity expansion] 2) Availability of cotton itself owing to severe drought in California [it produces > 90% of US Pima cotton production]. In 2015 area under Pima has declined from 2 to 1 Lakh acre [read this article http://www.nytimes.com/2015/08/08/business/a-once-flourishing-pima-cotton-industry-withers-in-an-arid-california.html?_r=1] . Even in Egypt area under Giza cotton is declining due to removal of subsidies on cotton. [http://english.ahram.org.eg/NewsContent/3/12/119530/Business/Economy/New-subsidy-cut-may-be-the-end-of-Egyptian-Cotton.aspx]

Here are my calculations:

For USA

So US is around 13crs Kg . See this link for US area under PIMA cotton http://www.supima.com/view-reports/acreage-estimate/ . Pounds per acre is from NYT article referred above.

Egypt produced 370,000 bales during 2014 . One bale = 225kgs. This amount to 8.3crs kgs

[see this link http://gain.fas.usda.gov/Recent%20GAIN%20Publications/Cotton%20and%20Products%20Annual_Cairo_Egypt_3-30-2014.pdf] 90% of Egypt cotton is extra long and long staple variety.

So Pima + Giza amounts to 21crs kg for 2014. As per Ambika website cotton consumption for 2014 was 1.89 cr kg and for 2015 2.23cr kg. So as per my estimates Ambika is already consuming around 10% of global production. Atleast for next 2-3 yrs it seems global production is not going to increase. So to repeat 1) Opportunity size ???? 2) Availability of cotton ????

Ramana’s portfolio (27-08-2015)

Update on the portfolio

PolyMed: Reduced my exposure in PolyMed

– Current weitage in portfolio too high

– Don’t see any near term triggers

– like the medical disposable industry, however I think company should have been more successful enough in expanding their product basket

Kitex: closed my position in Kitex.

– feel company should have been more forthcoming clarifying the doubts raised by some our members.

– I don’t doubt the management, but I think the reluctance to answer the questions made me rethink about transparency (am I nitpicking?). May add it back in portfolio when the dust settles.

NBCC: added more shares in July to August period. I think it is in a sweet spot. I usually don’t invest in public sector companies. However, in the case NBCC interests of GOI and other shareholders are in sync.

Paushak: added in July. It is almost like a monopoly with huge entry barriers.

Shaily: added in July. Good industry segment. Liked it when I saw Ikea and other big MNCs as some of the customers.

Hitesh portfolio (27-08-2015)

your views on vakrangee Hiteshbhai

POKARNA LTD ( Stock opportunities ) (27-08-2015)

I had a conversation with a representative of the company. Below is a summary

- For the new quartz plant, the average utilization rate in the previous year was about 40-50% and for granite it was 70-80%. Quartz utilization will improve going forward as sales pickup

- For the recent quarter, the quartz plant was shut down for ~20 days. Without this, their production and utilization would have been higher. (Possibly sales also would have been higher but this is my assumption)

- No immediate plans to add capacity and therefore they dont expect any additional funding for another 2 years. This is the status as of now but may change.

- Cash generated would go to service the debt and bring it down. That is the near term plan.

- Vizag plant has provision for adding lines so any expansion will use lesser capital as it will be a brownfield expansion

- Quartz uses a polymer and is not a straight extraction like granite. Polymer is driven by Crude prices. This is a positive as Crude price falls. (Not a big positive in my view as I read somewhere that polymer is a small component. Will need to check)

- Branding is through Quantra and it is doing well. Pokarna will have step up efforts to improve this.

- Primary competition is other companies having access to Breton technology (5-6 companies). Market is very large in US and Canada to accomodate all.

- Chinese quartz is of inferior quality and is not direct competition to them (not sure if this is correct. need someone from US to confirm this)

- Recent data on housing starts a positive. Company expects demand to grow (very generic on this so not much insight)

All in all, most of the data was a reconfirmation of what we know with 1-2 additional insights. Will have to watch the sales growth and debt reduction closely.

Disc – Invested. Please do your own due diligence