Posts tagged Value Pickr

Samhi Hotels – Turnaround with Tailwinds (29-08-2024)

try to give my two cent on samhi hotel try to look RevPar,occupancy ratio, ARR is incresesing or not, samhi hotel available 4500 mkt cap around with keys 4800( 0.9x) valaution on keys, peer chalets hotel available at 6x valuation with 3052 keys at 17000 mkt cap, majority hotel in TIER 1city so little barrier to entry, hotel in bussiness segment,Q1is not good for hotel sector but samhi hotel very good results to peer, preESOP is over , interest cost is also reducing, majority capex is over,try to look EBITDA MARGIN you get better picture, next three quarters would be good, marging expansion & debt reduction story can play out , disc not sebi registerd in last 7 days taken the postion , due your due diligence.

Hariom Pipes Ltd: A Capex Play! (29-08-2024)

New Investor Presentation released today is worth a look

Very Detailed one

Link: https://www.bseindia.com/stockinfo/AnnPdfOpen.aspx?Pname=83f2e395-b656-4467-a544-7816d617362a.pdf

Almost all the triggers are covered in this 2 slides + management is very much focused on such incentives

Better time ahead

Enjoy the Ride ![]()

Kiri Industries: Loan reduction and demand surge (29-08-2024)

Have recently started studying this business. Sharing my analysis here, comments welcome:

Why? – Special Situation investing

- Company has been involved in a legal tussle with Longshen group over one of their JV subsidiaries for ~10 years

- This has led to lack of focus on existing business and material legal costs over the years

- Finally in 2024, the case looks to be headed towards resolution as per Singapore Commercial court by Dec-25

Pros:

- Singapore court case vs Senda (Longsheng group china with 35k Cr Mcap)

- The company has won the case and is entitled to receive the $603 mn by Dec-25. Even with 10% cap gains tax, this is 2.25x the current market cap.

- On 29-Aug, they have also been awarded the legal fee (~2.5 Cr) which is quite low. I am sure they have spent more and are expected to spend 15-20 Cr more till resolution

- Company can get additional ~500 Cr if they win their appeal for interest rate (which wasn’t awarded) on 603 mn (@5.33% per annum for 2 years)

- Dystar valuation:

- Cash on books: $570 mn !!

- Debt: ~0

- Revenue CY23: $735 mn and PAT CY23: $72 mn

- Valuation: Even at a low 9 PE, the valuation should be around $1,220 mn (650+570 mn) or ~10k Cr. A good deal for most PE investors.

- Promoter increasing their stake from 27% to 42% with an infusion of 492 Cr via preferential warrants (can be converted over next 18 months) at 369 (measly 6% discount to CMP) is a sign of their trust in the issue finally being resolved soon. However, few key considerations:

- It doesn’t seem like the promoters have made any initial commitment while obtaining warrants so they might choose to walk away if things don’t materialize as per their expectations.

- They had increased their stake previously in FY18 by 5% (stock went up by 50%) and another 2% in FY19 (stock went up by only 18%) then the stake got reduced to 27% due to FCCB conversion to shares at very low prices

- Existing standalone business

- Revenue (FY24) – 633 Cr and FY 25 (E) – 750 Cr (20% YoY)

- Long-term debt ~24 Cr only

- Guidance: 1200 Cr with 3% EBITDA (highly unlikely)

- Valuation of a languishing business at 0.5x sales multiple = ~350 Cr.

- MD’s remuneration in FY23 was just 1.56 Cr which is not high for a company with 1500 Cr+ mcap and 0 dividends

Cons or Risks:

-

Primary FII investor (Lotus Global Investments Limited) is the same ones as in Hindenburg’s report on Adani. Mysteriously it sold all its stake on 21st Aug at 374. I wonder why when the court looks likely to be resolved.

-

No plan to award existing shareholders with cash from the proceeds

-

Company is planning to venture into unrelated business with new cash. They have ventured into manufacturing of Copper rods, cathodes, copper coils and Fertilizers. Had previously indicated their interest in EV, Renewables, etc

-

Company plans to invest money in 2 phases:

-

Phase-1: 2.4k Cr capex. Expected Sales: 15,000 Cr and Profit – 1.4k-1.5k

-

Phase-2: 6-7k Cr capex. Expected Sales: 25,000 Cr and Profit – 2k

-

Overall revenue (E): 40k Cr with Profit – 3K Cr

-

-

These numbers look a little high to me looking at Hindalco which has ~6% EBITDA margins in their copper vertical. But someone else can guide me here.

- Using Hindalco’s numbers, the profit comes to ~1.5-2k Cr to me. But this is too soon. A lot of execution is left.

-

Expected ROCE : They had previously guided for 25% IRR (internal target is 30%). Looking at other players this seems unlikely. Also, EV slowdown.

| Company | ROCE |

|---|---|

| Hindustan copper | 18% |

| Hindalco | 11% |

| Bhagyanagar | 21% |

- Standalone business going down the drain and company giving unrealistic guidance of 2x sales and 3% EBITDA margins in Q4FY24 concall, EBITDA was ~0% in Q1FY25.

- They have another JV with Longsheng, Lonsen Kiri, which entails a possibility of another legal tussle in the future. Lonsen Kiri is in fluorine dyes, indigo

Triggers:

- Nov-23: Interest rate and priority settlement appeal

- Apr-25: Sale of Dystar

- Exercise of warrants by promoters

- Entry of big investors. As per management, no big investor has invested because they’re waiting to see if Kiri will receive the money

- Revival of margins and sales in existing standalone business. Some sales has come back in last 2 quarters but nothing to write home about

Motilal Oswal Financial Services (29-08-2024)

Correct. Most of their multiple rerating is because of their wealth management business. If you look at multiples (market cap/EBITDA) of Nuvama, there is still quite a bit of runway left for MFS stock.

BLS International (29-08-2024)

How is Aadifidelis acquisition related to existing business?

The Anti-Portfolio (29-08-2024)

Actually its a 2.63 annual multiplier for last 4 years. I am also amazed to see. ![]()

![]()

![]() Some contributors Tata Motors 10X, AGI green 5X, SHIL 5X, Apollo Tyre 4X, Kalyan running 6X with large Capital still holding 25% of PF, Force Motors 8X. Rotating capital was the key with new buy with large base. Also leverage played an important role here. 50% of PF average all the time.

Some contributors Tata Motors 10X, AGI green 5X, SHIL 5X, Apollo Tyre 4X, Kalyan running 6X with large Capital still holding 25% of PF, Force Motors 8X. Rotating capital was the key with new buy with large base. Also leverage played an important role here. 50% of PF average all the time.

Samhi Hotels – Turnaround with Tailwinds (29-08-2024)

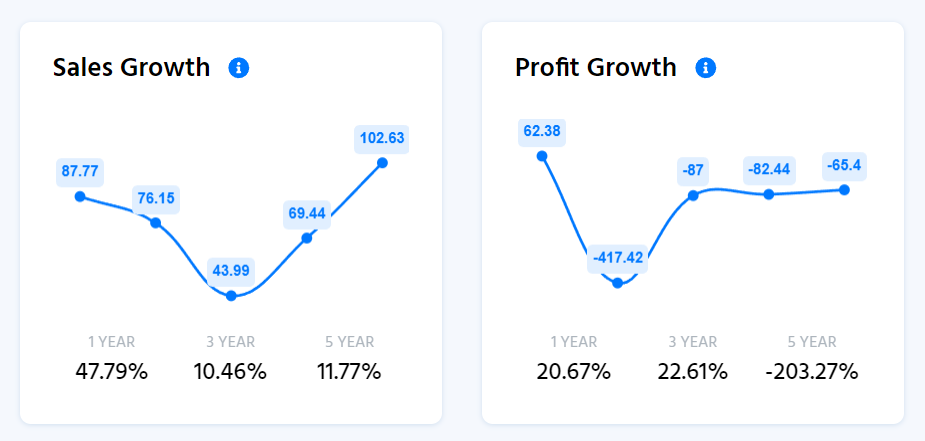

Clearly, Samhi Hotels is facing significant challenges in their business.

Let’s see some key points that we found out through some due diligence while analysing the standalone data of the company:

Profitability Challenges – Samhi Hotels has struggled to generate profits over the past 5 years. This reflects management’s inability to efficiently grow the business. Consistent profitability is important in the hospitality industry.

(Source: Finology Ticker)

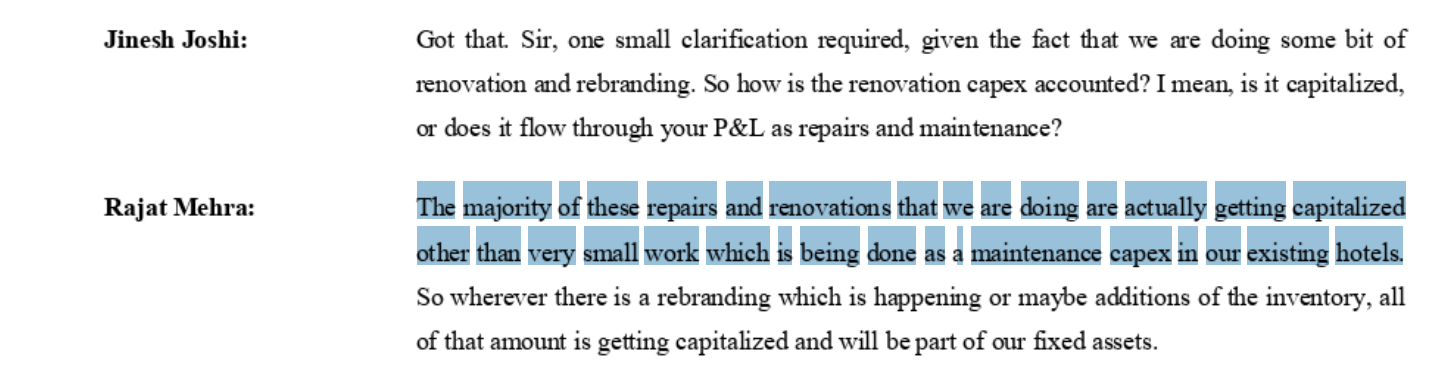

Questionable Accounting Practices – The mention of capitalizing maintenance capex in the latest concall raises suspicion. Maintenance expenses should typically be expensed and treated as operating expenses. This distorts the financial statements and misleads the investor.

(Source: Latest Concall)

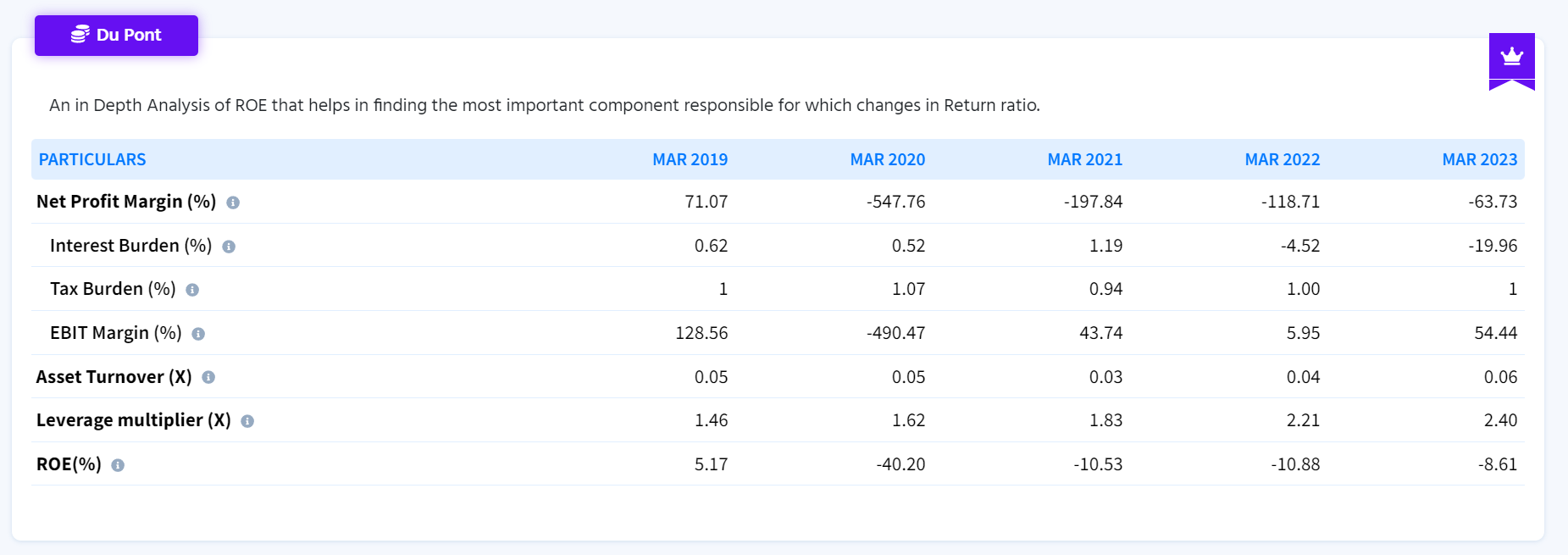

Du Pont Analysis(insight into drivers of ROE) –

- Asset turnover: Poor asset turnover suggests that the company is not efficiently utilizing its assets to generate revenue.

- Net Margins: Weak net margins suggest challenges in managing costs and pricing.

- Leverage: The debt burden is evident from the leverage component.

(Source: Finology Ticker)

Debt to Equity Ratio and Interest Coverage Ratio- The Low statistics are a red flag for financial risk. It warrants attention as it suggests that the company is accumulating losses and indicates that the company’s earnings are insufficient to cover its interest and debt.

(Source: Finology Ticker)

What do you think about the future of the company?

Investing Basics – Feel free to ask the most basic questions (29-08-2024)

How the intrinsic value of shares is calculated? Also please explain what factors to consider for calculation of intrinsic value of BFSI sector?

Srivari Spices and Foods Limited (29-08-2024)

There is nothing good or bad in rights issue. I was expecting rights issue @ Rs. 100… They are offering @175. It is good in the sense that the company will get enough capital to sustain the growth for some time. Once they reach a topline of 150-200 crores, they will be able to generate a profit of Rs. 20-25 crores, which will be sufficient to sustain growth without much capital dilution.

It is also good as it shows that the management is valuing it’s shares properly.

Let us see how they perform in H1-2025.