Private equity player GQG Partners hikes stake in GMR Airports to 5.17%-

Posts tagged Value Pickr

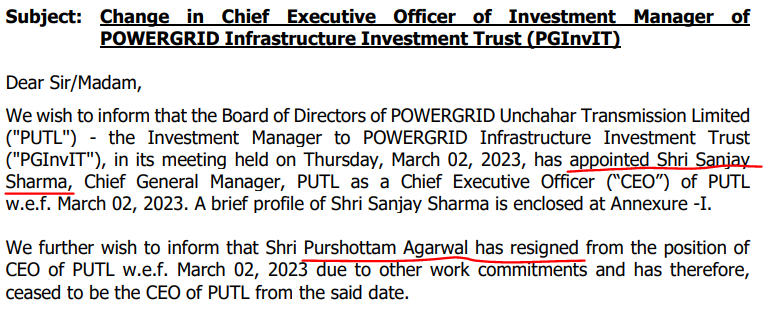

PGINVIT impairment of investments in subsidiaries and book value (29-08-2024)

This is a no event. PGINVIT has changed the CEO every year since 2022. I think these are dummy roles.

Companies with 20%+ growth guidance for next few years (29-08-2024)

net margin only 2% ?

Rajesh’s portfolio (29-08-2024)

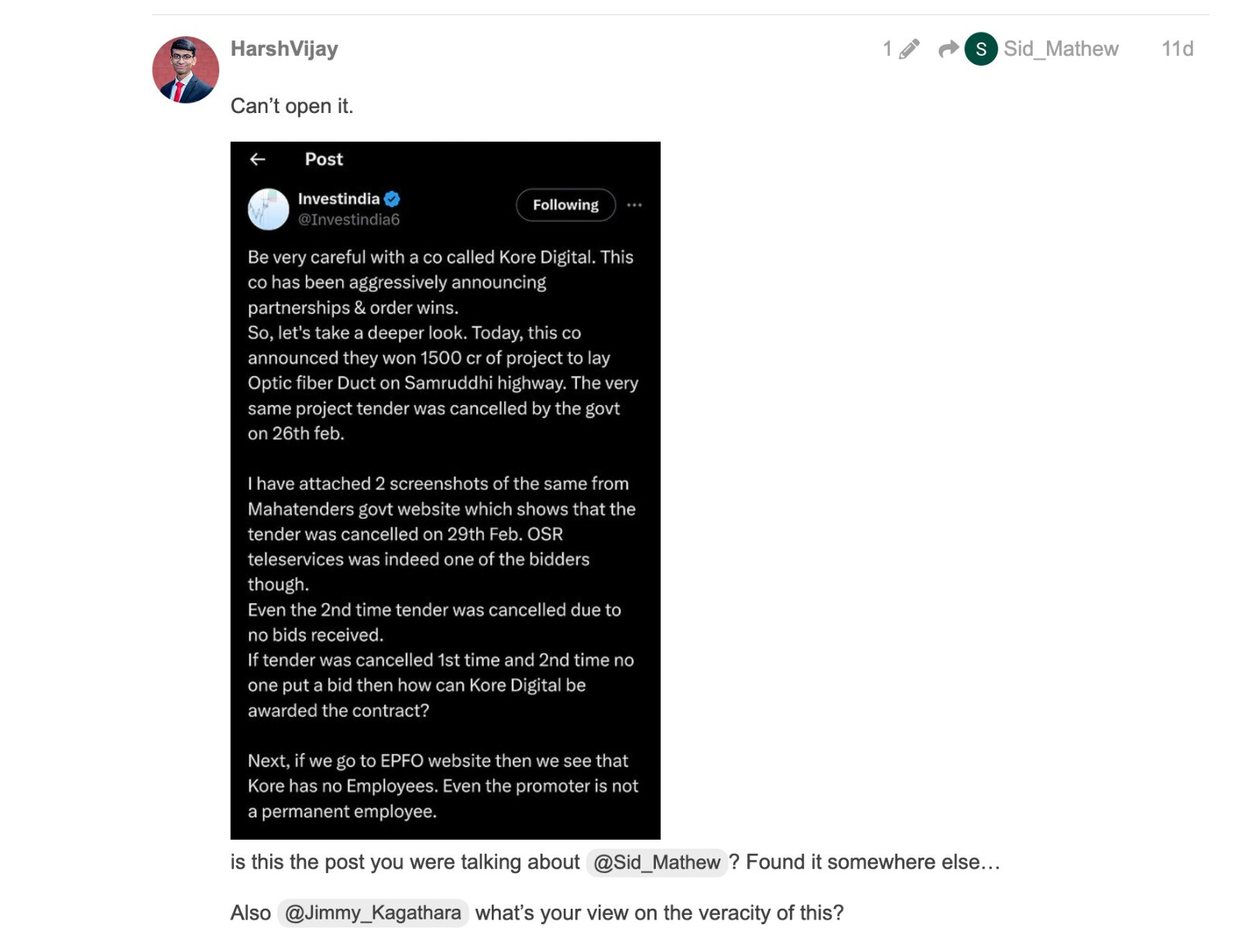

@Rajesh_Singh : Sir, came across this. Little concerned . Is everything alright with Kore?

Manappuram Finance (29-08-2024)

Over the past 8 to 10 years, Manappuram has proven to be a reliable asset for wealth generation, consistently rewarding its investors with dividends that have seen an increase over time. From dividends of less than 25 Paisa per share to now 1 per share, alongside a stock price that has multiplied sixfold from the 30s to present, plus dividends, it’s clear that Manappuram has provided numerous opportunities for long-term investors at various price points such as 60s, 80s, 120s, 170s. With anticipated Federal rate cuts potentially boosting gold prices, and the prospect of gold reaching 10K INR per gram in the next 3 to 5 years, Manappuram appears to remain an attractive investment for the coming 15 to 18 months. Any dip in its share price should be seen as a chance to invest more.

Pitti Engineering Limited: Is it on an inflection point? (29-08-2024)

2024 Annual Report is here

https://www.bseindia.com/xml-data/corpfiling/AttachLive/9fb520e5-7b19-487a-b264-393e320a8a33.pdf

Companies with 20%+ growth guidance for next few years (29-08-2024)

I have a 45 day trial period with them in the running. But it does not look like it is an early finder of multibagger stocks. Yesterday I was reading up on Jupiter Wagons and they have Titagarh Rail Systems’s info mixed with Jupiter Wagons.

So, if I have to extrapolate, there’s a chance that I will find such mistakes elsewhere as well.

Praveg Ltd: Play on Indian Tourism Industry! (29-08-2024)

Add on to above mentioned points, hotel industry is cyclical in nature,

A change in trend will drastically take away PAT

Companies with 20%+ growth guidance for next few years (29-08-2024)

Has anyone here used SOVERENN who claim to find multibagger stocks early on.

Sakar Healthcare – Tiny Pharma Company for promising Growth ahead (29-08-2024)

EPS has fallen 2 years in a row now. The March 2024 eps is lower than the March 2020 eps. Its trading at a PE of 60 (ind avg is 35). PB is 2.6.

No dividends being paid. Both ROE and ROCE are among the lowest in the industry. Don’t see how such a high PE is justified.