Of course those risk are there. But with experience one can easily find if a company is declaring false numbers; particularly in SME stocks where business is simple. It is more difficult to identity false numbers in complicated large businesses.

Operators play are there, hype is there. But one can avoid that through strict valuation yardstick.

I am not saying that researching SME stocks is easy, all that I am saying that researching SME stocks is more likely to be useful.

Posts tagged Value Pickr

Sumit’s Portfolio (28-08-2024)

Praveg Ltd: Play on Indian Tourism Industry! (28-08-2024)

All projection number on excel sheet looks promising. But one need to be cautious more about weaknesses of the business when one is paying very high price to buy it ! –

Big red flag: Company business is highly depending on the government. Most of land lease deal is with government and change in government could have serious impact on this company!

Most of locations has seasonality and fixed cost is going to remain round the year for maintaining it. Company has increased more fixed cost (man power, etc.). Promoters are not focused on core business earlier they entered in TV business and now they entered in advertisement business, etc.

Sumit’s Portfolio (28-08-2024)

@Investor_No_1

I do my own research, and therefore avoid widely known stocks. I understand that every widely known stock is researched by hundreds or thousands of full time analysts working on those stocks only. With my a few hours of research, I don’t think I can learn anything market don’t know. So there is no advantage in studying those stocks. Even theoretically, market is much more efficient in widely known stocks.

SME sector is different. When I research there I feel I am one of the few person researching that, and if I find anything good, probably I will be among the very first to enter there. Now a days annual reports of all the companies are easily available and what more one can read even if you are researching SBI!!

How to find those SME stocks? Well, I don’t know those companies. I just use screener to find stocks having certain quantitative attributes… May be high profit margin, good ROCE, Sales growth etc etc. Some of those stocks look interesting. Then I visit their website and try to understand their business, specifically if they have some competitive advantage or pricing power. If yes, I go to whatever document is available on their filing, investor link etc. If things look good, look for valuation, expected growth, scalability. Look at market cycle, sector headwinds/tailwinds etc. Do some scuttlebutt if possible.

Some sort of competitive advantage is a must before I pick up any SME stocks.

Liquidity is not a problem for small investors looking for a few lots. Further, one can always wait for the market downdays to pick them at a good discount.

Tata Motors – DVR (28-08-2024)

Do you plan to buy the regular Tata motors shares with the proceeds? I had purchased the DVR shares in Dec 2020 for 75. Had no intention to sell. But now it looks like if I held onto the DVR, I have to pay more taxes so I sold them. The PE seems cheap and with the cancellation of DVR the EPS of regular shares get a 18 percent or so gain. That would make the PE

Sumit’s Portfolio (28-08-2024)

Portfolio Update:

I’ve made a slight adjustment by reducing my exposure in Caplin Point, bringing it down from 20.90% to 19% following the recent run-up in its price. I’m reallocating this capital to acquire a small position in Transteel Seating Technologies Ltd, an interesting SME stock.

Brief Thesis:

Transteel Seating Technologies Ltd. operates in the office furniture space, particularly focused on ergonomic seating solutions. With the increasing trend towards hybrid and flexible work environments, there’s a growing demand for quality office furniture that combines comfort with durability. Transteel has a solid reputation for delivering innovative and affordable products, and they’ve recently shown strong growth in both revenue and market presence.

What excites me about this company is its potential to scale, given the ongoing shift towards remote and hybrid work setups. More companies are investing in ergonomic office solutions for their employees, and Transteel seems well-positioned to capitalize on this trend. Additionally, their focus on design innovation and direct-to-consumer sales channels could help them maintain competitive pricing while expanding their market share.

While still a small player in the overall furniture market, Transteel has the potential to leverage its niche positioning, innovative product line, and a growing brand presence to achieve substantial growth over the coming years.

I’ll continue to monitor their performance closely and look forward to seeing how they execute on their growth plans.

Sumit’s Portfolio (28-08-2024)

Hey, thank you so much for your message. A cursory look at your journey tells me we are very aligned in our investment philosophy, except you have much more courage than I do, given that you have a significant sum invested in private equity. As a fellow angel investor, I can only stomach about 5-10% of my over all net worth in startups. I have started angel investing very recently and have managed to get into BluSmart, Zypp Electric in their later funding rounds.

I totally get why you’d want to keep your identity under wraps for now. Running a startup takes enough focus as it is, and I respect that you want to keep the attention on that. But whenever you’re ready to share, I’m sure you’ll have some incredible insights about scaling a platform business with venture capital. Would love to hear that story someday!

I am very inspired by Pulak Prasad’s book, same as you. Thinking in bets is another favourite read of mine. It seems we have a lot in common and a lot to learn from each other.

I’m looking forward to more conversations with you down the road. ![]()

Cheers to compounding, both in business and in wealth!

P.S. Anytime you want to chat more, just let me know—I’d love to hear more about what you’re building!

Sumit’s Portfolio (28-08-2024)

I totally get where you’re coming from—those reasons are exactly why I got into the SME space myself! But lately, I’ve found myself a bit more cautious, and here’s why:

- Quality of Information: Sure, there’s more information available today, but with SMEs, I’m not always confident about how accurate or transparent it is. Sometimes their financials feel a bit shaky or inconsistent, and that makes it tough to really dig deep and trust the numbers.

- Liquidity Issues: The low trading volume in these stocks can be a double-edged sword. It’s great when you’re buying undervalued stocks, but not so much when you want to sell, and there just aren’t enough buyers. That can make exiting a position tricky and potentially costly.

- Governance Risks: I’ve noticed that corporate governance can be hit or miss with SMEs. There’s always that worry about the alignment (or lack thereof) between the promoters and the minority shareholders. It makes me think twice, especially when it comes to trusting the management’s decisions on how they handle money or related party dealings.

- Funding Constraints: Many of these companies struggle with access to capital, especially during tough economic times. This can limit their growth and, in some cases, even threaten their survival. I’ve also seen instances of frequent equity dilution to raise funds, which can really hurt returns for those who got in early.

- Sector Risks: SMEs tend to be concentrated in a few sectors, which can be pretty cyclical. I’ve seen this especially in manufacturing or real estate—one bad turn in the economy or policy shift can hit hard. So, there’s a bit of a risk in being overexposed to these fluctuations.

- Hype and Overvaluation: In bull markets, it’s easy for some SMEs to get caught up in the hype and end up overvalued. It’s exciting at first, but I’ve seen corrections that are brutal when prices snap back to reality.

Don’t get me wrong, I still believe there are hidden gems in the SME sector, and I love finding them! But I’m trying to be more selective now, looking for companies with solid governance, a real competitive edge, and a sustainable growth path.

Moneyboxx Finance – Good compounder for our money? (28-08-2024)

How I think of MB now?

@Apandey

Firstly I would like to discuss on the industry side a bit, plz note I can be very naive in my analysis due to the complexity of the industry

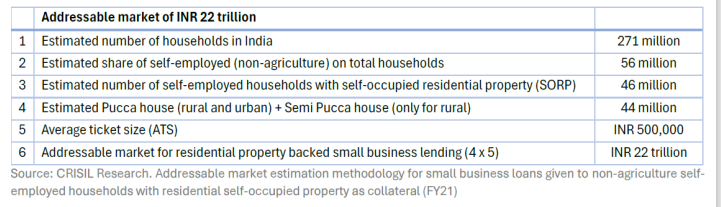

So the total addressable market as per the below screenshot is 22 trillion INR

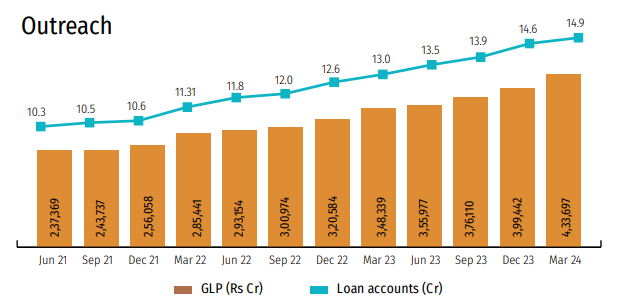

Some industry numbers for MFI

Portfolio outstanding of MicroFinance industry as on 31st March 2024 is `3,77,706 crore with 1,238 lakh active loans and 6.6 crore unique live borrowers.(From another report)

So what we can see is the loan account are 2x of active borrowers which is like every borrower has 2 loan accounts

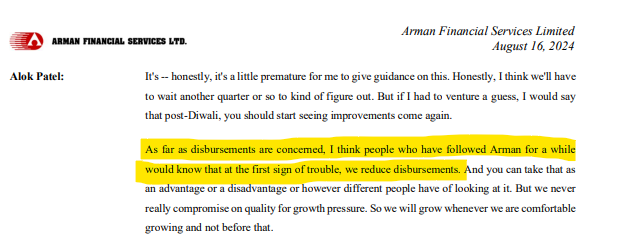

So looks like MFI borrowers are overburdened and on top of this we had election, heat wave, school fee paymet etc etc this is damaging the ability to pay so the MFI are now forced to slow down this growth which would derate them. Below snippet is from armaan call

But the thing is money boxx is not MFI , though the rural distress is a PAN india phenomena I think moneybox kind of model would have faster recovery than MFI borrowers. Here are the following reasons

- 30% of moneyboxx borrowers are new to credit, so there borrowers just have 1 loan account which is with moneybox and their underwriting is more difficult.

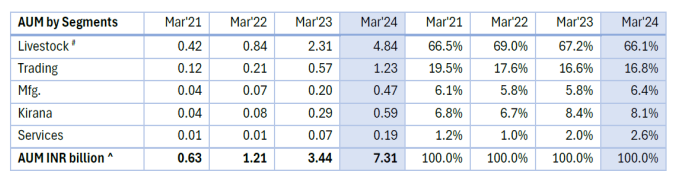

- Below is the screenshot of how the MFI portfolio is spread at an industry level and how is moneyboxx portfolio spread. I think again moneyboxx has an upper hand here because livestock as a segment is less seasonal and more cash generating that agriculture (my guess)

- Their secured book is 27% as on june 2024 which would go to 40% by March 2025, currently about 30-35 branches of MB only do secured. Do read the below snippet from five star.

- On one side we have aarman who doesn’t want to comment on guidance and on the other side we have five star who are very confident of 30% growth. This shows growth varies across ticket size.

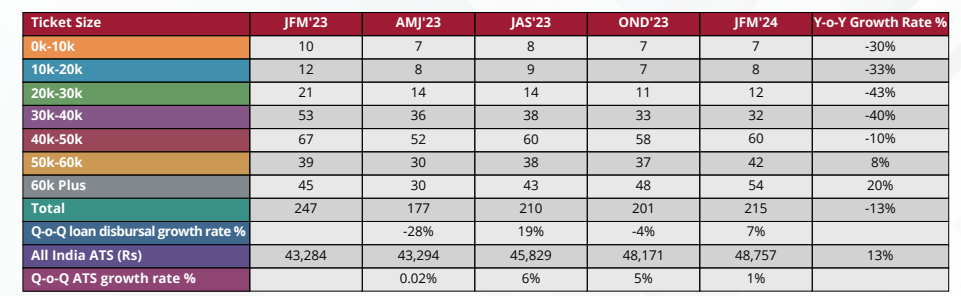

Even if we take different ticked size in MFI we can see marked difference as the ticket size increases

What moneyboxx has to say on growth?

- If we see about 45% of moneybox disbursement came in Q4 for FY24

- Last FY 664cr of disbursement added 386cr to AUM so 60% so to reach an AUM of 1400 cr this year they will have to roughly disburse 1100 (should be less due to secured % increasing) If the number of branches increase to 130-150 by dec 2024 (growth of 30% -50%) Q4 disbursement can grow by 50%-70% implying 450 to 500 cr disbursement in Q4 FY25 (should be more than this)

- So for us key monitorable is branch opening and employee headcount growing

Conclusion

My overall understanding is rural is under distress but the segment which moneyboxx catres to will have a recovery much faster than MFI. Aarman says from Q4 they are positive that growth my revive so we can kind of assume from Q2-Q3 MB will turn around in terms of asset quality and growth

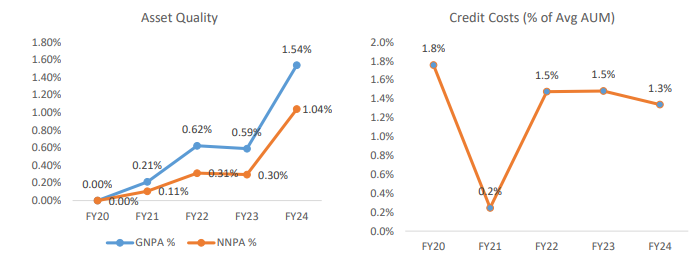

Asset quality

- This is definitely a concern but it is still under management guidance of 2% to 3% credit cost and given that the secured business would pick up the blended credit cost should definitely reduce going forward

Execution capability

This is something very difficult to judge but below is a relative analysis I have performed

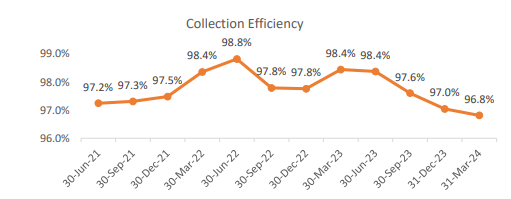

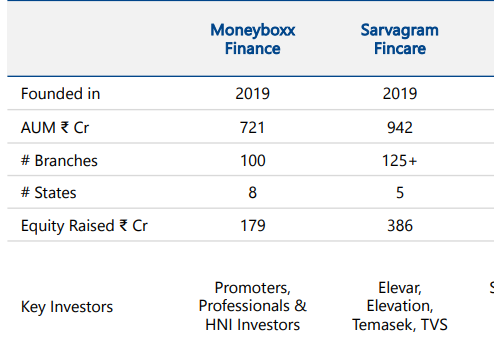

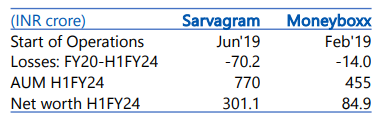

- Comparison with Sarvagram fincare and moneyboxx

Moneyboxx doing 130cr of income on same asset base where sarvagram is doing 80cr. The business model by default is a 20-25% ROE business if u see their interest spread , hence with moving more towards secure and opex/cost of borrowing reducing I see them moving towards achieving those numbers (contingent to asset quality)

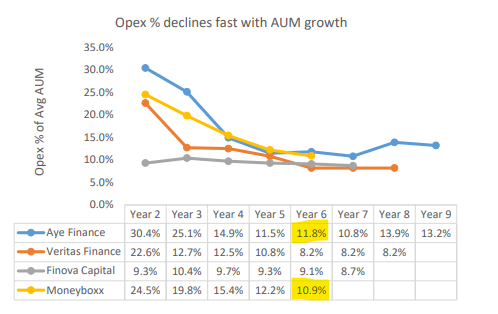

- It is projected on the opex front that MB should do better than Aye and through MB has always had a better asset quality then Aye thought we cannot have a direct comparison as Aye has a larger book but this also something we can track going forward

All in all MB also has valuation comfort and if the grow at 100% while maintaining asset quality they definitely deserve a 3.5 to 4 PB (five star getting 4) which would imply a 50-100% gain from current levels

Dic – invested, can be wrong

Moneyboxx Finance Ltd_Stock Idea_Final.pdf (2.4 MB) (wonderful report to have a look on)

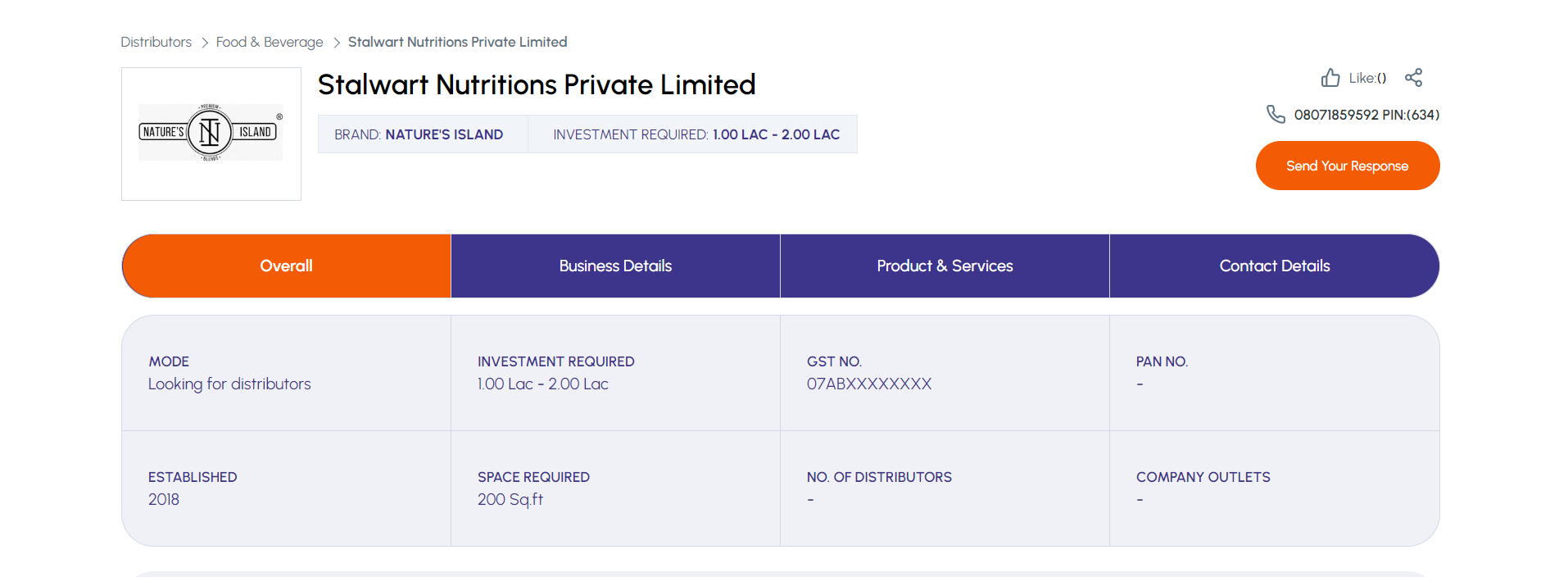

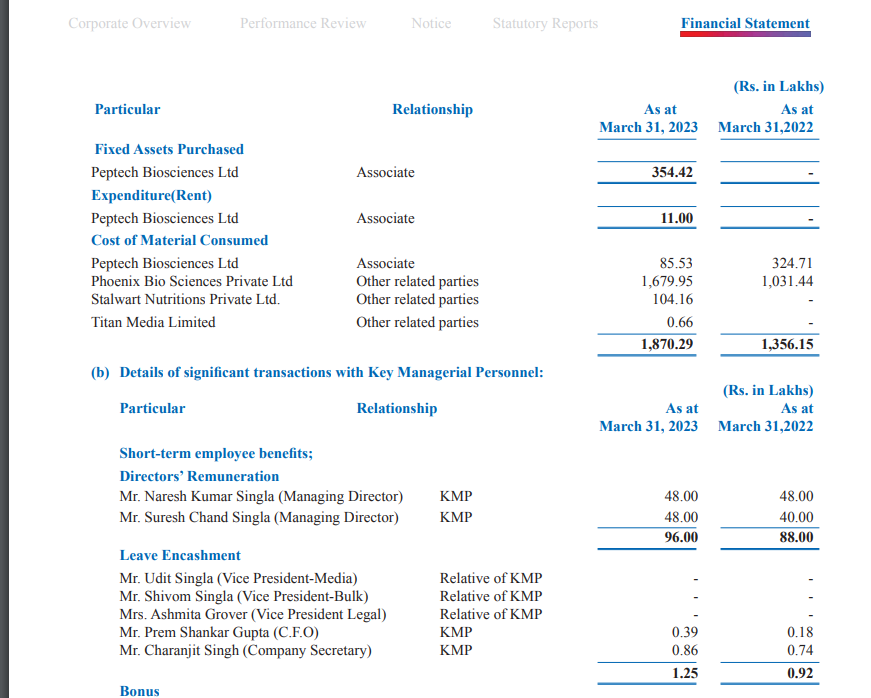

Titan Biotech Limited (28-08-2024)

It’s basically the brand name of their “Other related Party Company” – Stalwart Nutritions Private Ltd.