Focus on last row… this is from premier energies RHP… Its Shakti… Shows, execution is in full swing

Focus on last row… this is from premier energies RHP… Its Shakti… Shows, execution is in full swing

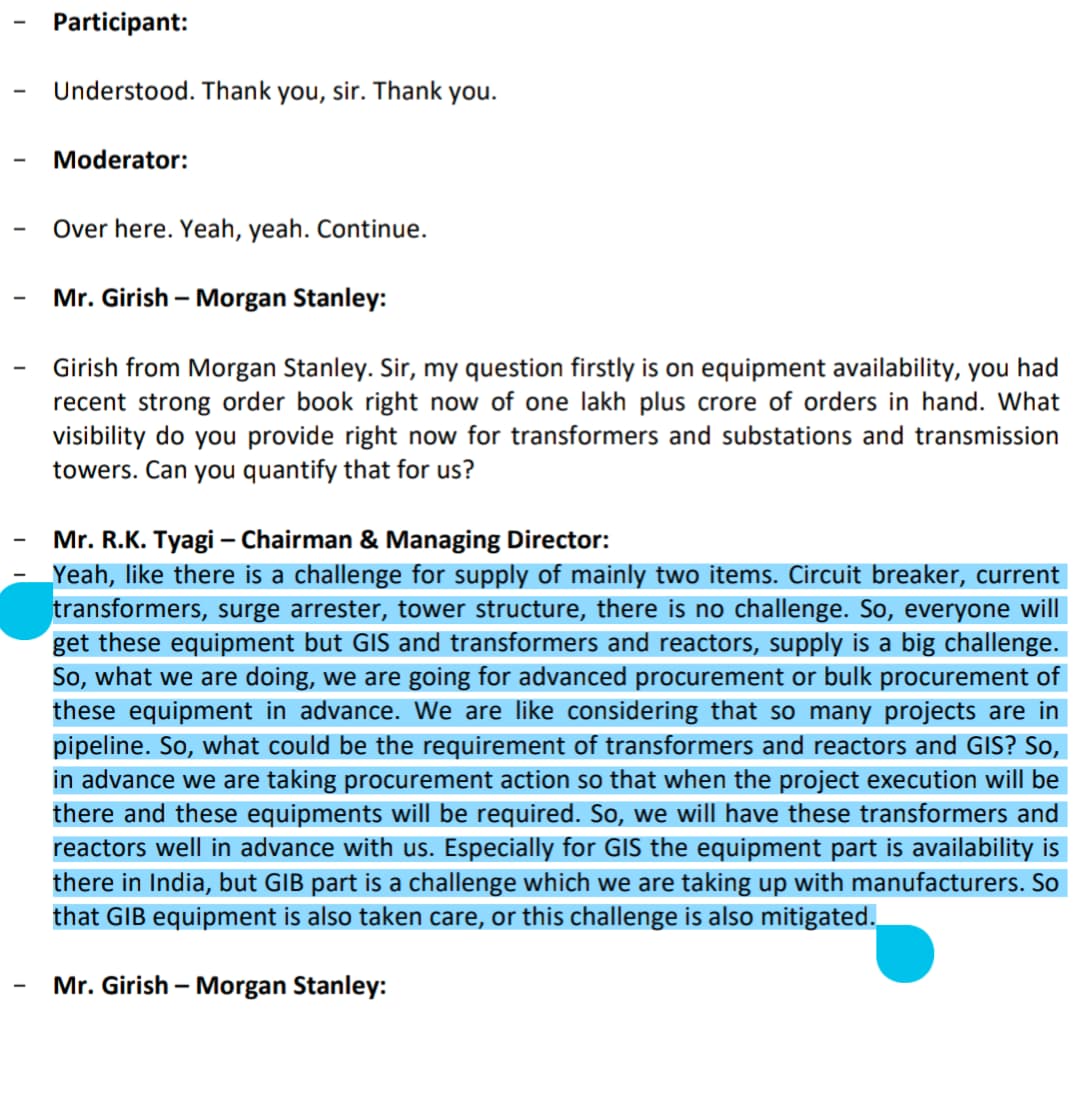

That’s the snippet from concall of Power Grid

(post deleted by author)

This is an excellent reason and way of looking at SME stocks

Problem is I have not even heard of any of the names you mentioned as “the first” or they must have done very well in their areas…How did you know or rather begin to know about these names and businesses?

update on buyback and NSE listing

Below is an except from AR 22-23 page 148. With so many related parties, how can a minority shareholder be confident that the company is acting in the best interests of the shareholder and not in favor of one of the related parties particularly those companies in which the promoters have significant ownership?

List of Related Parties:

i. Associate

(a) Peptech Biosciences Limited

ii. Significant influence over, the entity;

(a) Titan Securities Limited

Corporate Overview Performance Review Notice Statutory Reports Financial Statement

Annual Report 2022-23 | Page149Titan Biotech Ltd

iii. Other related parties

(a) Tanita Leasing & Finance Limited

(b) Connoisseur Management Services Private Limited

(c) Tee Eer Securities & Financial Services Private Limited

(d) Titan Media Limited

(e) Phoenix Bio Sciences Private Ltd

(f) Stalwart Nutritions Private Ltd.

(g) Emprise Production Private Ltd.

(h) Mbon Nutrients LLP

(i) Suptex Industries Pvt. Ltd.

(j) Simtex Mart Pvt. Ltd.

(k) SR Infratech

(l) Titan Agritech Limited

Monarch has initiated research on Praveg –

They have forcasted –

FY22A Sales, PAT & PAT Margin – 45cr, 12cr & 26%

FY23A Sales, PAT & PAT Margin – 84cr, 28cr & 33%

FY24A Sales, PAT & PAT Margin – 91cr, 13cr & 14%

FY25E Sales, PAT & PAT Margin – 223cr, 28cr & 13%

FY26E Sales, PAT & PAT Margin – 410cr, 87cr & 21%

FY27E Sales, PAT & PAT Margin – 500cr, 110cr & 22%

But, Company has given guidance for 300cr topline in FY25.

For me, FY25 sales – 300cr

FY26 sales – 420cr (+40%)

FY27 sales – 590cr (+40%)

40% – my own expectations.

PAT margin expectations – 25-26%

So, FY27 PAT – 150cr

Current Mcap – 2300cr

FY27 Forward P/E – 15.33

What is the relation of Nature’s Island with Titan Biotech? Is it a subsidiary or associate company, or is it an entity controlled by the promoters but in which Titan Biotech has zero or limited stake?

Disclosure: Not invested.

With P/E > 26 and P/B > 8 , this looks really expensive . Also I am unable to pin point the reason of why this would continue to grow with EV threat . I haven’t seen any investments by sharda in EV industry so far . Is it time to book profits and exit completely or is there still a spark that management can turn into fire ?

Have congratulated you earlier for holding Trent for last 2 decades and I am sure these petty reasons like inclusion in any particular index/funds buying etc. were never the main criteria for your hold.

Why I call them petty is because LTIM exclusion does not warranty its bad performance and neither Trent’s inclusion means anything over long term. While its a good feeling to see the companies we hold grow in size and get included in bigger & bigger indexes with time, point to note here is that LTIM if now getting excluded was once included ![]() so its a cycle and what’s important is the business to remain on right track and promoters to remain true to their vision & ethical…I think these were main reasons that you could held for 2 long decades…or they were something else or add to these reasons…would be good to know…

so its a cycle and what’s important is the business to remain on right track and promoters to remain true to their vision & ethical…I think these were main reasons that you could held for 2 long decades…or they were something else or add to these reasons…would be good to know…

Now valuations rating & de-rating is another animal which no one is able to tame and it happens when it happens…many momentum investors enter or exit at these times…I am yet to fathom how to prepare for valuation de-rating or if there is any need to consider this in my investing strategy…

Disc: Trent has become top holding recently, hence highly biased & critical. Hold LTIM also. Thoughts are personal and only for learning purposes. Not a buy/sell recommendation and I can be wrong in all my assessments