Posts tagged Value Pickr

RBM Infra – a less discussed SME (27-08-2024)

Compiled some notes, few days ago, Enjoy:

18.08,2024

Listed on NSE Emerge, Lot Size 200

Establishment in 1993, RBM Infracon Limited is a distinguished engineering and infrastructure company. Over the years, it has evolved into a Specialist highly professional, reliable, and safe service provider in the infrastructure service arena, aiming to provide innovative, integrated, and customized solutions tailored to client-specific needs.

Specializes in comprehensive services in engineering, execution, testing, commissioning, operation, and maintenance, primarily in the mechanical and rotary equipment sector.

This co. basically used to do the shutdown/overhauling of Nayara(Essar) and Reliance. These two companies are too big to do these kind of yearly shutdowns on their own and hence use companies like RBM to perform shutdown. But lately RBM has grown its business line and has become an EPC player.

Its expertise spans various industries, including Oil & Gas Refineries, Gas Cracker Plants, Coal/Gas/WHR based Power Plants, Petrochemical, Chemicals, Cement & Fertilizers.

Major Clients:

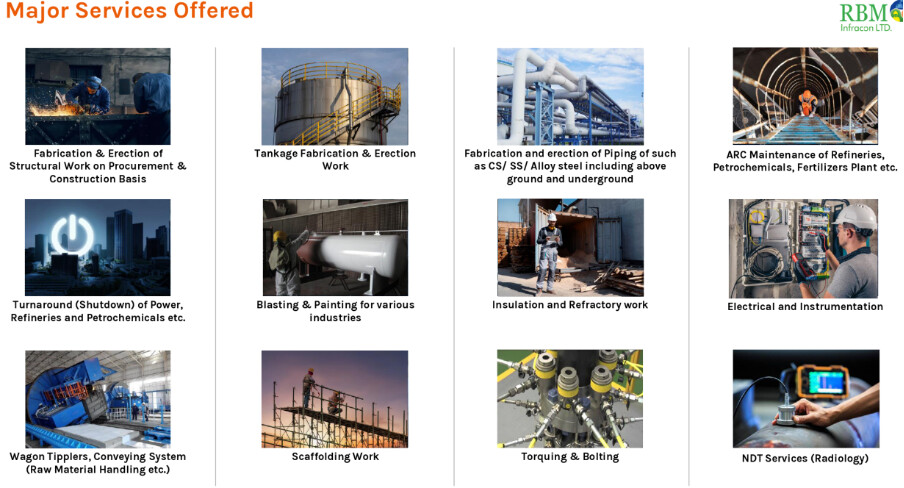

Main Lines of Work:

Piping Services

Plate Work Fabrication and Erection

Structural Steel Work

Civil Construction

Coke Plant Maintenance

Tanks, Silos, and More on EPC Basis:

Erection of Plants and Equipment:

Blasting Cleaning and Painting:

Insulation and Refractory Work

Work shop Specialists

Rail wagon loading

Operation and Maintenance services

Turnaround services

Operation & Maintenance of Heater & boiler

Operation and maintenance of Fertilizers and cement plant

In today’s interview with Tiger Assets, the management spilled some beans . It was an online event and I attended it.

Highlights:

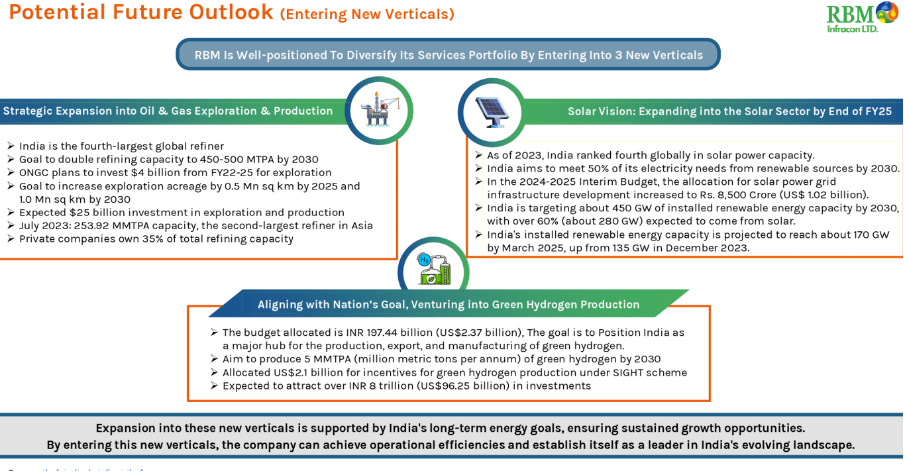

Mr Jaybajrang Mani, Chairman & MD, told that they have clinched a Rs 2000cr, 15yrs deal with ONGC for Oil exploration. The LoI is expected by 30th August. The contract will state that ONGC will allot RBM with 132 wells for digging crude oil and natural gas and they would share it a ratio of 65:35.

65% of the output would go to RBM and the rest 35% would go to ONGC. This means that for 15 long years, RBM can keep on digging crude oil and natural gas from those wells and the chairman has also assured that the revenue potential from this contract can very well go beyond 2000cr. In his own words:

“Yeh Project Toh Samander Kee Tarah Hai, Jitna Chaho Paani Nikaal Lo”

Also he told that they have almost clinched a deal of Rs 500cr, for a Solar project with Reliance. Company has worked on Solar for the past 1 year with Kalpataru and other companies.

He said that PAT can grow upto 10% from next year onwards as ONGC project is higher margin (20-25%) although Reliance can be only 6-8%.

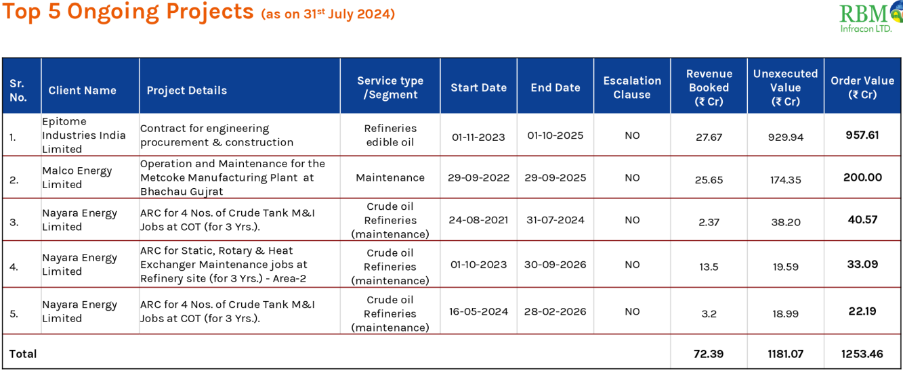

Also explained the reason for realisation of lower revenue this Q, the left over revenue will be added in coming Qs. Epitome order is done around 200cr but invoice is not generated and from next month the work will start.

The revenue guidance is Rs 400cr for the current financial year and Rs 1000cr for the next. Targeting 5000cr revenue in next 5 yrs.

The company is in negotiations with Greenzo Energy, a Gurgaon based company for Green Hydrogen project. The good news may come in few weeks. He sounded confident.

Greenzo has Govt. approvals for Green Hydrogen & Ammonia Projects.

https://www.greenzoenergy.com/

Challenges & Working Capital:

- Delays in material delivery

- High working capital needs

- Debt funding options: Rs.250 Cr preferential issue planned along with funding from bank.

Management & Operations:

- 1,700 employees (500 contract-based)

- Ex ONGC executives hired for project execution

Auditor changed due to excessive delays at the auditors end. They were not able to comply with compliances on time.

Sector Expansion Plans:

- Exploring coal mining and gas sector opportunities

Capex Strategy:

- Future plans to reduce Capex by engaging more subcontractors for larger projects

The Promoter holding is shown wrongly here, its 60.53%, reduced from 72.4% as 1662000 shares have been allotted at a premium of Rs.376 per share on Preferential basis to non-promoters in February 2024. There is no insider selling.

Compiled Notes from here & there, no position as of now. Do your own diligence.

Vinati Organics (27-08-2024)

I am adding my notes from last few calls of theirs.

08.12.2023

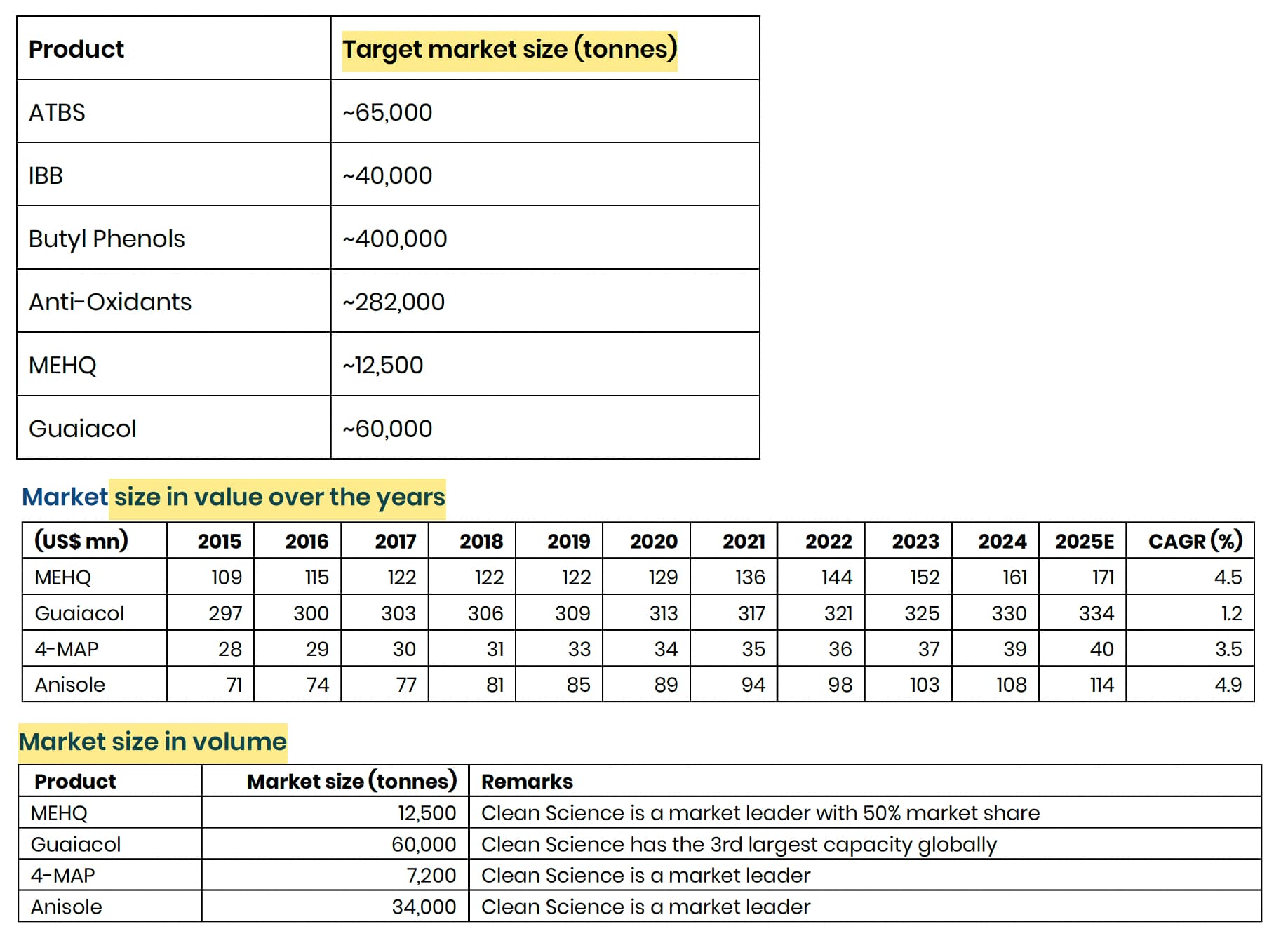

- Commercialized Ortho Secondary Butyl Phenol (OSBP) and Di-Secondary Butyl Phenol (DSBP) at Lote facility, only Indian manufacturer for both

- OSBP capacity: 5000 MT; $4-5/kg product; used in agrochemicals, polystyrene, perfumery & liquid solvent dyes

- DSBP capacity: 1000 MT; used in surfactants for agrochemicals, speciality liquid dyes

19.02.2024 CNBC

- Witnessing order book recovery starting February across products, FY25 will be better than FY24 (15-20% growth in sales)

- Anti-oxidant recovery is slower

- Revenue from new line of ATBS will start in FY26 (expect 1.5-2x asset turns on brownfield capex)

- 27% is sustainable EBITDA margin

FY24Q4

- Capacity utilization in ATBS (~611 cr.) and butyl phenols (~300 cr.) is near optimal levels

- Antioxidants: 130 cr., 25% utilization; expects to double to 50% utilization in FY25 (280-300 cr.). Facing pricing pressure from Chinese oversupply and weak demand (peak revenue potential of 700 cr.)

- FY24 Capex: 400 cr. (550 cr. in FY25); MEHQ plant (2000 MT) was commissioned in March 2024, and OSBP (5000 MT) and DSBP (1000 MT) in December 2023

- Commissioned 33MW solar plant

- CSM products contributed 150 cr.

12.06.2024 B&K

- ATBS expansion (40k to 60k tons) will cost 300 cr. and is expected to commercialize in H2FY25

- Antioxidants capacity of ~24,000 MT should generate 700 cr. sales

- Started manufacturing butyl phenols in 2020 and incurred capex of 250-300 cr. for setting up a 39,000 MTPA capacity

- MEHQ, Guaiacol, 4-MAP, anisole, and Iso-Amylene derivatives can generate 500 cr. sales with capex of 500 cr. capital expenditure (1x asset turns). Expected to contribute 50 cr. in FY25

- ATBS competition: couple of Chinese companies have added ATBS capacities for domestic consumption (combined capacity is 15,000-20,000 MTPA). Atvantic Finechem (a Meghmani group company) has acquired trademarks and rights of Lubrizol’s ATBS technology and have started manufacturing ATBS in India. Their current utilisation is ~10-20 tons/month. Clean Science had also applied for an environmental clearance to manufacture ATBS

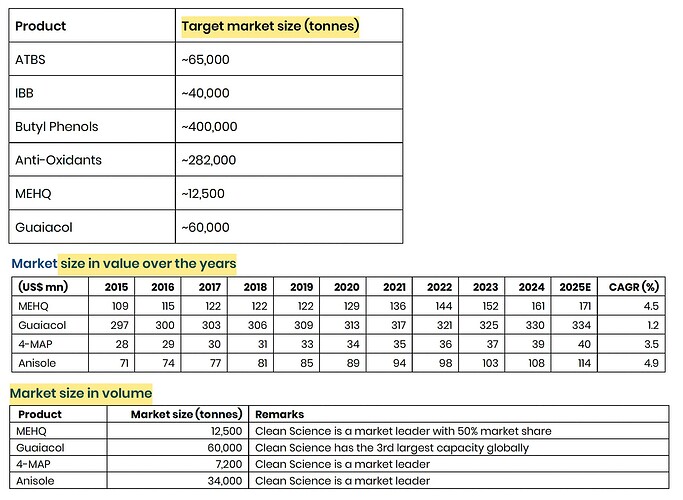

- Market size of their products

Disclosure: Invested (no transactions in last-30 days)

Sumit’s Portfolio (27-08-2024)

Excellent philosophy Sumit. I am sure it will do great.

Investing in SME sector requires real confidence in one’s own analysis (I largely invest in SME sector only). I prefer that for the following reasons:

- Unlike earlier days when information was not readily available, now information is easily available even about SME companies.

- When a widely known stock is looking undervalued, most probably it is because market knows something I don’t know. I have experienced these in many value stocks like DHFL, ITNL.

When a SME stock is undervalued, it is more likely to be a value pick. - New developing sectors start in SME only… We have Macfos, the first electronic e com operator, Anlon technology- the first listed service provider to airports, Zeal Global- the first listed GSSA… And we can give many examples. Probably I love to analyse new businesses, and try to guess it’s competitive advantage.

- Theoretically, small stocks does better than index in long run.

- Further volatility is higher, and thus we get more opportunity to buy at discounted price.

Thus, to an entrepreneur investors, SME does give a good opportunity. Once these stocks are recognised by market or bigger HNIs, it gives good return.

Ami Organics – Pharma Intermediates & Specialty Chemicals (27-08-2024)

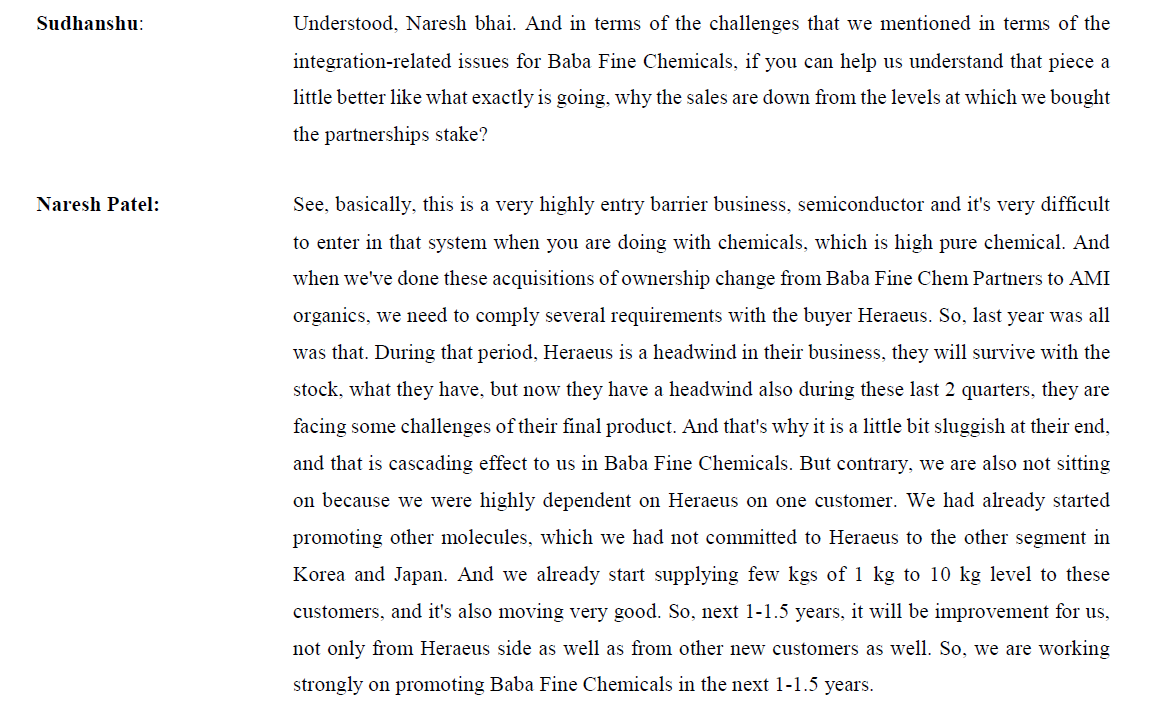

So the acquisition of Baba Fine Chem seems to have gone haywire. Looks like they had only one (major) customer Heraeus who is facing challenges in its final product. Baba had revenue of Rs.47 crore in FY23 and Ami paid 4X EBIDTA (Rs.68 crores) for a 55 % stake. Last year, the management said Baba will grow 3 to 4 X in a year. But now it is making just Rs.5 crores per quarter in revenues. Quite a coincidence that Heraeus started facing challenges just when Ami took over one of their suppliers.

Ami is now trying to develop other products and tap other customers, but until they get anything concrete, this acquisition will have to be deeply discounted. The good thing – hopefully – is that at least the technology they got access to is still useful and relevant.

Som Distilleries and Breweries (27-08-2024)

I think it is not possible since the promoters are not majority shareholder of the company in the first place. It is 35% something so I don’t think this is true. Moreover the volumes have dried up big time but on positive note the delivery percentage has increased significantly from the monthly and weekly average. So lets hope for the best…

Ranvir’s Portfolio (27-08-2024)

One has to compare the total organised existing capacity and then add all the capex announced by the major players

My guess is ( because I don’t remember the exact numbers ), it won’t be more than 7-9 pc of capacity addition / yr – going fwd. But the demand growth is generally > 10 pc

Supply – Demand demand dynamics look favourable for hotel sector for the medium term ( next 2-3 yrs ). I think u can easily get this data. If u can post this here, it ll be of great help

Can anyone share views on Paramount Communication Limited? (27-08-2024)

Can anyone share views on Paramount Communication Limited?

Ranvir’s Portfolio (27-08-2024)

Nothing except reading about the Industry, reading concalls, listening to management interviews, taking help from some YouTube podcasts

That’s about it. This is generally enough