@araman JYOTICNC is in top-15 list

OPTIEMUS is in top-27 position in my list

Posts tagged Value Pickr

Microcap momentum portfolio (25-08-2024)

Microcap momentum portfolio (25-08-2024)

@visuarchie i am not focusing on correcting yahoo finance data. right now when ever i am getting time i am trying work on below points.

- Back testing automation.

- creating top 25 stocks automatically (compare last week and creating new 25 stocks list)

- Return calculation.

- How to keep code in open source.

Note @ my code o/p mostly matching with u r publishing list.

MOLD TEK PACKAGING—dividend plus growth (25-08-2024)

Good question, I wonder if someone has asked this question in the concall before.

Would love to hear from folks if any inputs.

Microcap momentum portfolio (25-08-2024)

@araman i am trying to use yahoo finance library . Data is not accurate. other than that most of things are OK. if you are able to do using Google sheet , that excellent.

Hindustan Foods (25-08-2024)

Following is the phrase taken from the website that you have attached in your post. They starting their own brand is something that I am unaware about. As far as I know, they started a facility in health care segment. Please go through that phrase below:

“HFL Healthcare and Wellness Pvt.Ltd. is a 100% subsidiary of Hindustan Foods Ltd (HFL), which is listed on both BSE & NSE. HFL is part of the Vanity Case Group Of Companies that operates 34 plants across 16 different locations in India, manufacturing multiple categories of products for the FMCG, Healthcare & Wellness sectors.

The mission of HFL Healthcare and Wellness Pvt.Ltd. is to become a leader in the contract manufacturing space and a preferred business partner for Medicated/Non-Medicated Foot Care, OTC and Personal Care products.”

You will see that it is clearly written what their goal is. Please share the source where you read about they starting their own brands.

Microcap momentum portfolio (25-08-2024)

@visuarchie Except one, I was able to match all other names in your list with the sheet I was working on. Can you please check if JYOTICNC should be really ranked so high.

In the sheet I was working on, it was ranked 47 while looking at a lag of 12 months and 153 while looking at a lag of 6 months.

My sheet asked me to go with OPTIEMUS

Not suggesting that your list is incorrect. You have been at it much longer and its quite possible I am making some silly mistake

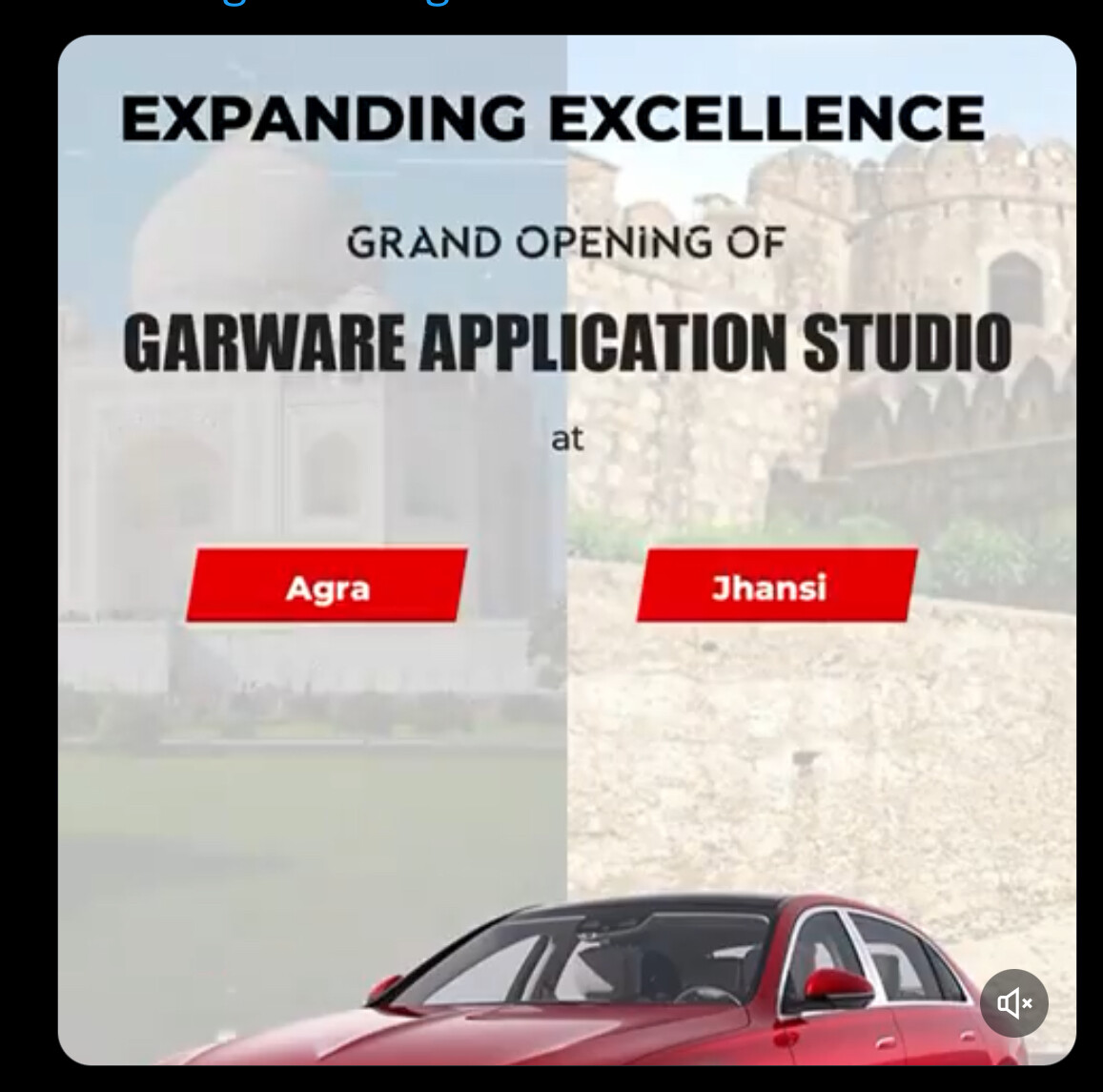

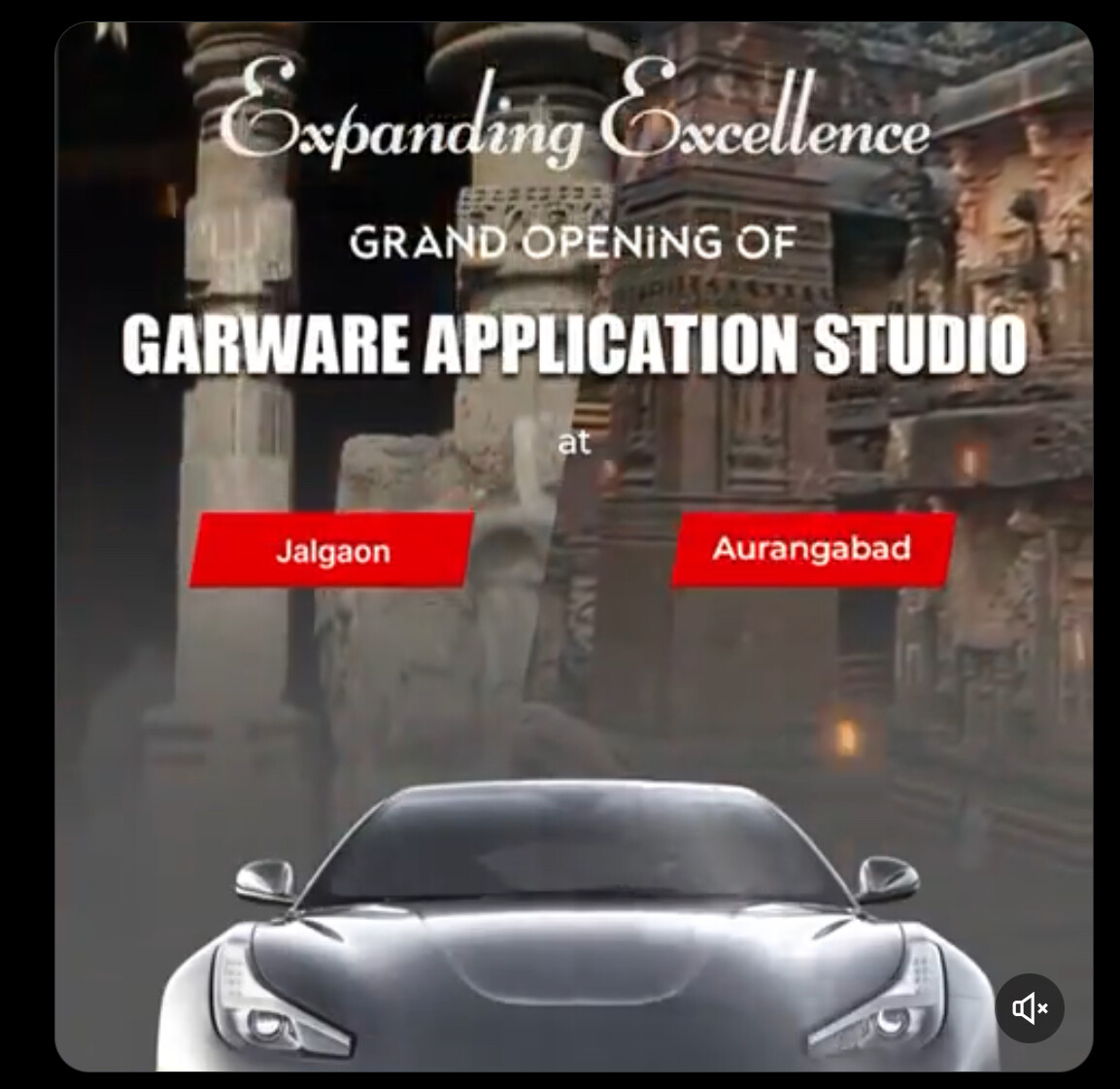

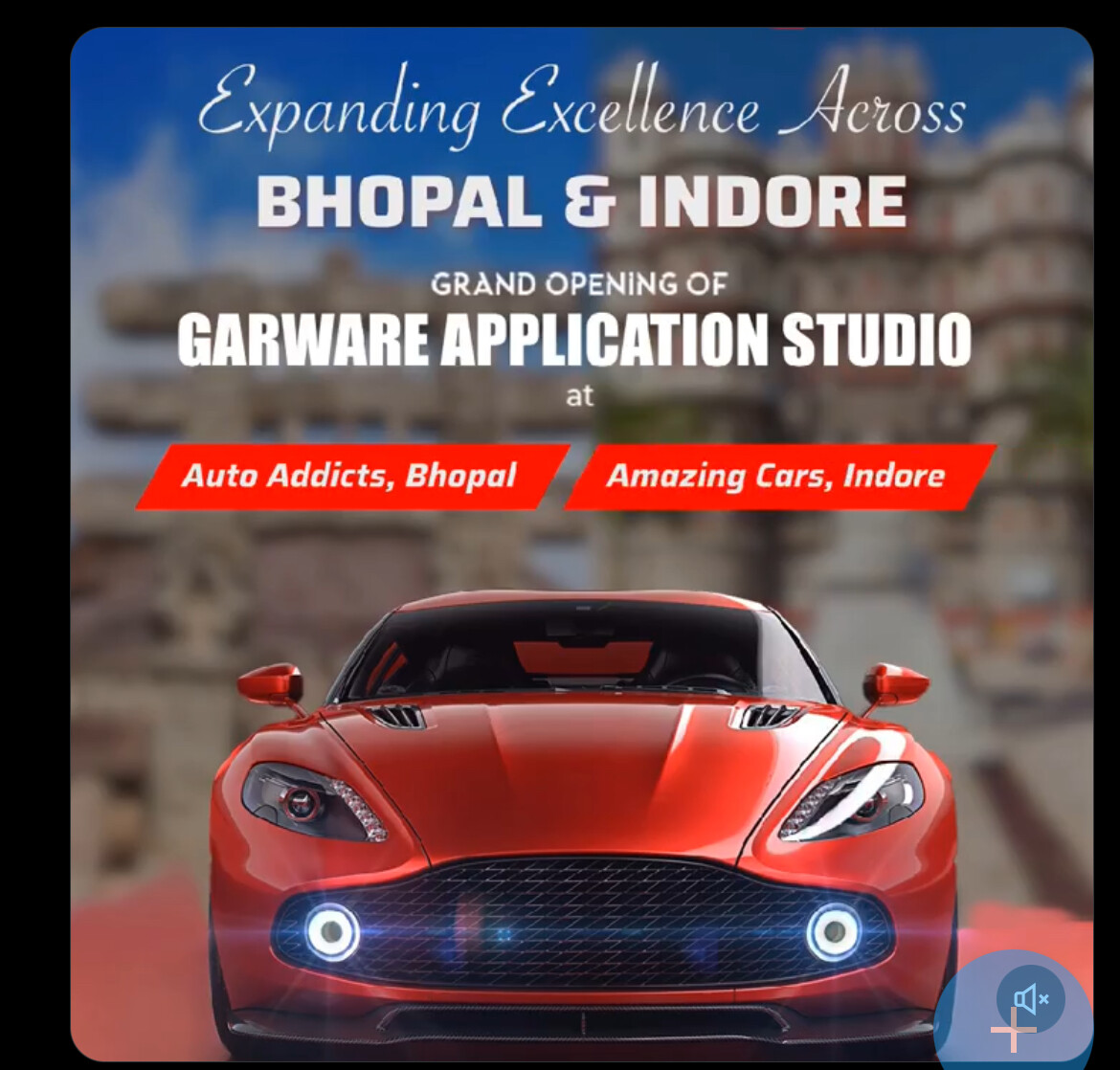

Garware Hi-tech films (Earlier Garware polyester) (25-08-2024)

This quarter they are to adding Garware application studio aggressively

delhi

agra and jhansi

jalgaon and aurangabad

faridabad

bhopal and indore

pune

disc – invested not buy/sell recommendation

Microcap momentum portfolio (25-08-2024)

Very happy to see people willing to collaborate on developing this further. Power of community sharing.

Microcap momentum portfolio (25-08-2024)

NSE data comes in multiple categories, EQ, BE etc. It is quite possible for the dates that you are referring to, the stock has gone to BE category.

When you want to check the data on NSE, click to show all categories and then it should be fine.

Senco Gold: Upcoming gold story! (25-08-2024)

Senco Gold –

Q1 FY 25 concall and results highlights –

Current breakdown of number of showrooms –

Company operated – 97

Franchise showrooms – 68

Total – 165 ( spread across 109 towns and cities and 01 in Dubai )

Added a total of 06 new stores in Q1

Q1 financial outcomes –

Revenues – 1403 vs 1305 cr, 7.5 pc

EBITDA – 108 vs 67 cr, up 62 pc

PAT – 51 vs 27 cr, up 85 pc

Same Store sales growth @ 4 pc

Avg Ticket value @ Rs 73.9k vs Rs 63.7k for FY 24

Q1 Stud ratio @ 9.9 pc vs 11 pc for FY 24

( diamond sales were down by 3-4 pc in Q1 – due rising gold prices )

**Sale of recycled gold stood at 35 pc of total sales ( ie customers exchanging old gold ornaments for new ones ) **

Have launched lab grown diamonds under the Sennes brand

Aim to add about 12-14 more stores in FY 25

Aim to add about 12-14 more stores in FY 25

About 95 pc of company’s gold stocks are hedged. Due to the sharp duty cut on Gold imports announced by the GoI ( recently ), there will be an adverse financial impact of about 50 cr for the company for the remaining 9Ms this FY. However, the duty cuts have also stimulated the demand for gold and gold jewellery which should help the company offset this impact

Aim to grow topline by 18-20 pc for FY 25 vs FY 24

Depreciation charges in Q1 are 18 vs 12 cr ( up 50 pc YoY ) – mainly because of aggressive store opening in FY 24

Confident of touching a stud ratio of 12 pc for full FY 25

Growth in Q2 ( as on the date of Concall ) has been a whopping 25 pc ( triggered by duty cuts ). Hence the confidence to guide for a 18-20 pc topline growth for full FY ( with same store growth guidance @ 11-13 pc )

Also seeing healthy growth in Franchise stores in Tier -2,3 towns – probably an indication of improvement in rural economy and normal monsoons

Elevated levels of other expenses in Q1 are unlikely to continue wef Q2. The same were elevated as the company was spending a lot on brand promotion / marketing etc as the Mkt was showing weakness wef late May / Jun

Company is confident of making up for a large part ( if not for the full part ) of inventory losses of around 50 cr in the next 3 Qtrs – due increased sales, lesser discounting etc

To be on safer side, company is guiding for 15-18 pc bottomline growth for FY 25

Disc: holding, biased, not SEBI registered, not a buy sell/recommendation