May I know how this is similar to ITC? Are you referencing the ITC hotels demerger? My understanding is that hotels business will list separately in some time.

Posts tagged Value Pickr

Bajaj Finance Limited (25-08-2024)

(post deleted by author)

Deepak Fertilizers and Petrochemicals (25-08-2024)

Business:

- Revenue contribution: 40% Fertiliser; 40% Mining chemical (TAN); 20% Industrial chemical (Nitric acid & IPA)

- Profit contribution: 80-90% from mining and industrial chemicals (vs revenue contribution of 60%)

- Change in favorable product mix: Moving from fertiliser to mining and industrial chemicals (down from 80 to 45% now)- Agri cyclicality reducing

- Raw materials: Nitric acid (75% of capacity would be utilised internally) and amonia for TAN and fertiliser

- Ammonia is made from hydrogen (compressed from air) and nitrogen (gas)

- Entered into long term contract from Equinor for stable natural gas price (to start in 2026)

- Only manufacturer of TAN in India; serves 40% of domestic demand (rest is imported from Russia)

- 2200 cr capex in TAN would enable to serve 60% of domestic demand and make it 3rd largest TAN producer in world (expected to go live in H2 FY’26)

- 65% demand of TAN comes from Coal mining (Govt’s focus)

- Russia dumped 50% of their supply to India in FY’24 (much lower than FY’23) due to muted demand in Peru and Brazil- this is normalizing

- No supply addition of TAN in 5 years

Market share:

45%- Nitric Acid (South Korea is largest exporter; China was but imposed export ban)

35%- IPA

Fundamental triggers:

-

Amonia prices going up

-

TAN spreads increasing

-

Import duty increasing

-

Capex of 2000 cr in nitric acid (60% capacity already booked for 20 years)

-

Volatility in margin going down due to backward integration

-

In TAN business, moving into forward integrating explosive chemicals: Like Solar industries; in nitric acid also moving towards speciality nitric acid (solar and steel grid- high purity is required)

-

Margins becoming 18-20%

-

With expanded capacity, can serve 60% of India’s domestic demand

Multiple things at play:

Govt focus on mining (tailwind)-> Beneficiary is Deepak as only player of TAN in India (used in coal mining as explosive) → Supply side constraint: imports are made tougher due to higher import duty on TAN in budget (plus Russia banning its export); Change in product mix (favorable); backward integration

During FY25, they can do 950 to 1000 crore PAT if commodity prices remain stable; trading at a 12-13x PE ratio.

Monitorable:

- Margins in the range of 18-20%

- Check commodity prices (investor presentation)

- Competitive intensity: Coal India (key customer) and Chambal is expected to enter into TAN

- Debt level

- Monitor backward integration of ammonia

Credit:

SOIC IAS

Bastion Research https://youtu.be/gj0eUjrL46Q?si=tfk9Mac4SFfku6gB

Ammonium nitrate prices set to rise as India cuts imports from Russia – BusinessToday

Deepak Fertilizers and Petrochemicals (25-08-2024)

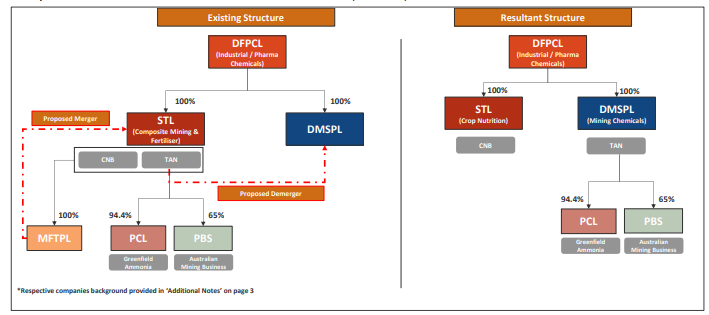

Company is demerging business from DFPCL to DMSPL which is wholly owned subsidiary, hence no need for separate listing. This is similar to ITC demerger.

MAS Financial Services – High RoEs, Decent Growth (25-08-2024)

Thanks for detailed reply.

But what I pointed is completely different,

NBFC business is not easy that is not the point…!, bandhan Bank and SKS are completely different story from each other as well as from MAS also.

Mr.Kamlesh born in a town 25km from my town, I have seen them growing from 2 cr to 10k crs.

What strenth they have is pure pure lower penetration of banks and NBFCs.

That’s why they have grown, they have taken 27% on mortgage loans, does it possible in upcoming days.

Now they r focusing on home loans!!!

Can anyone tells me what they will achieve ?

They accepted now there is no room for growth, and to run the show and to protect their AUM they r riding on HL and ML.

Ranvir’s Portfolio (25-08-2024)

Sir,

Please guide us on how can one understand an industry or sector well.

Where any sector which is new to you and you want to build some edge how will you make it happen?!

Pyramid Technoplast – Chota Time technolpast (25-08-2024)

- Total income for Q1 FY25 was INR 133.6 crores

- Overall volume increased by 14% year-on-year

- Gross margin was 25.2%, EBITDA margin was 9.3%

- Targeting revenue of INR 600 crores for FY25

- Aiming for EBITDA margin of 9-10% for FY25

- Long-term goal of INR 900-1000 crores revenue by FY27 with 11-12% EBITDA margin

- Revenue mix: 52% Polymer, 36% IBC, 12% Metal Drum

- IBC plant (Unit 7) operating at 50% capacity

- Metal Drum capacity being fully utilized

- Expecting 20% growth in IBC volumes over next 2 years

- Aiming to increase Metal Drum market share as capacity expands

- Expanding Metal Drum capacity from 30,000 to 50,000 per month, targeting 70,000 by Sept 2024

- Setting up new recycling plant (Unit 9) for backward integration

- Expanding IBC and Polymer Drum capacity in Maharashtra (Unit 8)

- Raw material prices have stabilized

- Export demand impacted by increased freight costs but now recovering

- Chemical industry growth driving demand

- Increased competition with new players entering market

- New IBC line in Maharashtra to add 144,000 units annual capacity

- Metal Drum capacity doubling from 10,000 to 20,000 tons per year

- Polymer Drum capacity increasing from 19,000 to 25,000 MTPA

- Export demand recovering after being impacted by high freight costs

- Targeting INR 600 crores revenue for FY25 with 9-10% EBITDA margin

- Long-term goal of INR 900-1000 crores by FY27 with 11-12% margin

- Capex of INR 45-55 crores per year planned for FY25 and FY26

- To be funded through internal accruals and cash balance

- Opportunities in recycling and backward integration

- Risk of overcapacity and margin pressure with new competitors entering

Smallcap momentum portfolio (25-08-2024)

@visuarchie Sir, please help sharing the spreadsheet. Hope it can be downloaded and edited. Thank you.

Ion Exchange (India) Limited (25-08-2024)

- Consolidated operating income up 18% YoY to INR 5,676 million

- EBITDA grew 31% YoY to INR 641 million (11.29% margin)

- Net profit increased 35% YoY to INR 448 million (7.89% margin)

- Engineering division: Revenue +13% YoY, EBIT +26% YoY

- Chemical segment: Revenue +36% YoY, EBIT +36% YoY

- Consumer division: Revenue +9% YoY, Loss of INR 34 million

- Chemical plants operating at 65-70% capacity utilization

- Capacity expansion in chemical segment

- Focus on penetrating international markets for chemicals

- Consumer segment prioritizing scale over immediate profitability

- Roha chemical plant investment of INR 400 crores

- INR 125 crores allocated for new technology in Roha plant

- Engineering segment: 15-20% topline growth expected for FY25

- Chemical segment: 15% growth guidance maintained

- Engineering order book at INR 3,394 crores

- UP project residual value: INR 813 crores, significant execution expected in H2 FY25

- Roha plant expected to reach optimal capacity utilization in 3-4 years

- Asset turnover of over 2 times expected on INR 275 crores investment

- Positive government policies creating opportunities in water treatment sector

- Some legacy projects impacting engineering margins, expected to improve by Q4

- Chemical segment performing well with robust margins

- Engineering segment expecting improved execution in coming quarters

- Management change planned from October 2024

- Focus on international opportunities, especially in Middle East, Africa and Southeast Asia

Microcap momentum portfolio (25-08-2024)

Hi @araman, I have quite good experience and expertise in Google sheets. We can connect and work on this together if you are willing.

@9916673623 I use kite historical API. And have developed few algorithms too. Let me know if I can also join you and help in whatever way possible.

In case the Google sheet method works then we can try and create historical investments and weekly and CAGR for everyone’s benefit. If Google sheet can’t be used we can perfect the entire process in python along with historical investments and returns.