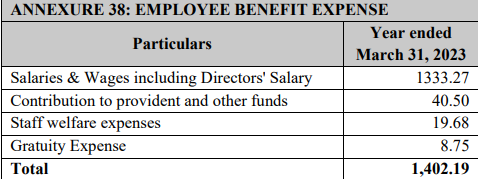

For the salary part, there is one more issue. i found a 5cr discrepancy in the employee expense amount for FY23 mentioned in the DRHP and the audited financial reports for fy24.

DRHP

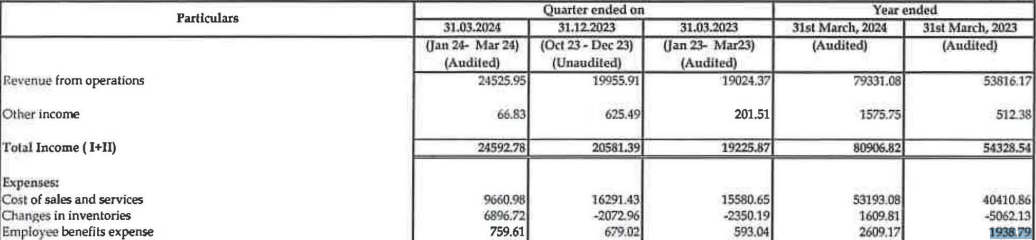

FY24 audited financial report

Can somebody explain this?

For the salary part, there is one more issue. i found a 5cr discrepancy in the employee expense amount for FY23 mentioned in the DRHP and the audited financial reports for fy24.

DRHP

FY24 audited financial report

Can somebody explain this?

Any update on ethanol plant commission?

In Jun’24 results, no sign of ethonol numbers.

@visuarchie , hello sir,

I normally use momentum indicator as Average of sharpe returns of 3months, 6 months and 12 months on the small cap and microcap universe.

Instead of using average of these three time periods ,

If for ranking I use only 3 months sharpe returns or just 1 month sharpe returns, what difference it will make? And which one is more desirable from returns point of view?

I believe it’s partial profit booking rather full exit …

True. I didn’t want to edit it after making the post. The earnings crashed by close to 30% from Oct 20 to Oct 22; stock price crashed by close to 40% during the same period. ( I am referring to the values 18.96 and 13.87 for EPS during the periods and 166 & 103 for stock price )

P/E came down but not substantially as I stated before. So you can basically call it as a stock trading below its own ten year median P/E during both the periods.

The change was in P/B. In Q2 and Q3 of 2022-23 it traded at a low P/B value and at times going below 1.

When the video was shared the assumption was that the high P/B was justified because there are entry barriers in this business. Even while agreeing that gold focused players are here for the long term and not everyone can scale this up , it is also true that many are opportunistically getting into this business affecting the margins and business growth at least for a short period.

So for such a business which goes through these cycles P/B alone could be a good reference. When it is trading at high P/B chances are that the market is reflecting the high ROEs and RoAs . But the high returns are attracting many opportunistic players into the business . When it is trading at low P/B those opportunistic players have already got in bringing down the returns . Now the returns are no longer attractive so that only focused long term players continue. The cycle repeats as non gold NBFCs/ banks etc get out of it.

So what about the low P/E? Where does it fit in? I think the easiest way to think about this is that the ratio of P/B and P/E , which is RoE , should go through a cycle if you believe that the business shows a cyclic nature – even if they are short cycles. If you believe that there are strong entry barriers then the returns or the ratio of P/B to P/E should improve or remain stable.

I am thinking this afresh so please don’t mind any contradictions with the previous post. Also I am thinking as I am writing this so the arguments may have holes. I am trying to think about what he was referring to a low P/E and high P/B scenarios. Let’s think about the truck business which had a book value of 2000 Rs and providing a return of 500 Rs. If it is trading at 2000 Rs then the return is 25% which is high. So for the sake of simplicity let’s assume that the market is pricing it at 4000 Rs and the earnings yield if you buy the stock now is only 12.5% . The P/E is 8 now. If the owner deploys another 2000 rs that gives zero returns then the P/E is still at 8 but price to book has become an attractive 1 now. So the essence of his message, I believe , was that you shouldn’t be looking at the high P/B negatively. You shouldn’t if you believe that entry barriers are strong. But if they are not strong then many players will enter this business bringing down the returns and the stock price would react to that.

Now something else.

Right now the projections on gold loan portfolio seems positive. But my question is how do you see the non gold loan portfolio. If I remember right only about 50% AUM is gold loan now. How good you think are their non gold loan portfolio? It is not the secured kind as referred in the video. In fact when we say that non gold NBFCs and banks may not do well since they are not focused , the same should also be true for gold focused players entering into other business. Will they lose the advantage they had on as a gold focused player or the present stock price take care all of that?

Absolutely agree that these are not ideal and caps the multiple BCL can command.

Regarding low cash flows, I agree that it has been on lower side but I did a comparison some time back with its PAT, the numbers were OK i.e. no red flags (Cumulative PAT of last 5/10 yrs not >>> Cumulative CFO) which would indicate Financial shenanigans. With the nature of business changing from low margin Edible Oil to mid-teens Distillery, we should expect higher cash flow. The same has been mentioned by Management (Mr. Mittal).

Product price is controlled by Govt, agree, but same Govt assures the uptake of its product, so we are assured of ~100% capacity utilization. Moreover, EBP is one of its pet projects and so many Ministeries keep harping about it, be it Petroleum, Transport or Farm. Right now, India has a deficit of Ethanol (if it has to reach 20%). Surplus Ethanol is few years later and do note that BCL’s manufacturing capacities are fungible between Ethanol and ENA. With the demographics of India and rising affluence, alcohol demand is only going to go up. I am not even considering Ethanol for Diesel.

I 100% agree that for BCL market cap to go up, earnings need to increase and like you said, FCI rice availability is the (only) hope in near term. Based on what I understood from the answer to my question to Mr. Mittal during Q&A, BCL doesn’t intend to use FCI rice even if it’s available. The benefit BCL will have in such a scenario (FCI rice is made available) is that since many Ethanol producers will shift to FCI rice, it will ease demand of Maize, thus reducing its price.

Disc: Invested so maybe biased

Hi @rambaranwal, thanks for all the interesting insights. Just went through a couple of articles and found this

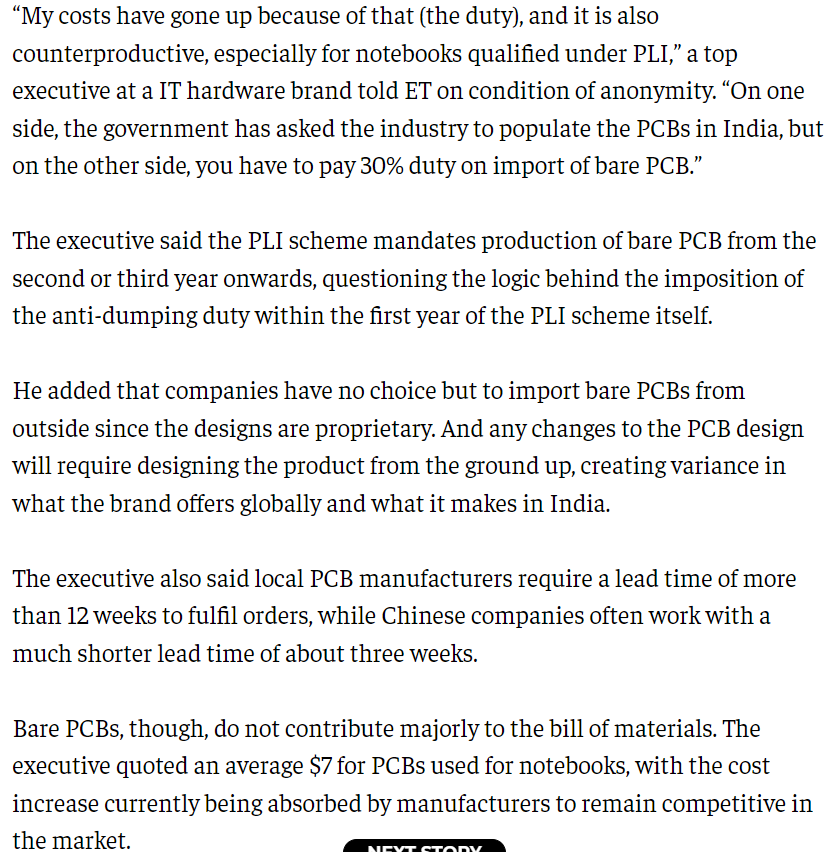

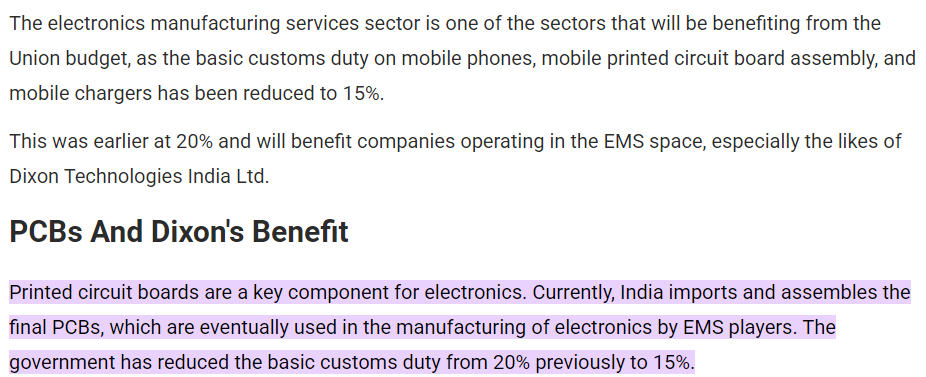

1. Do you think there is a risk of the government reducing the import duty on Bare PCBs due to the above mentioned reasons (plz refer the image)?

2. Also plz refer to the below image as well. It says that the govt has reduced the import duty to 15%. Am I misunderstanding something? I’m confused at one place it says the duty has been raised on Bare PCBs at another it says it has been reduced (and both are very recent news) would really appreciate some clarity

I agree! However, In the stock like this, market usually don’t react on the information, news or narratives they want it to be reflected in the numbers first that too consistently for few quarters because of the past experience that it isn’t one off but rather it’s a long term trend. That’s what i believe so technically once it starts reflecting in numbers the market will start aggressively adding it or atleast start taking interest. Regarding the downside, I’m not that smart but from the little I know 130-140 is a strong long support if markets falls down significantly however in small corrections it should respect 140-150 based on technicals

Except for the first point, rest is already know to market. Still not able to understand why the price is still down. Also, if market falls, won’t there by risk of further downside?