Yes. I had 5 RE, but applied for 100. Let’s see what happens

Posts tagged Value Pickr

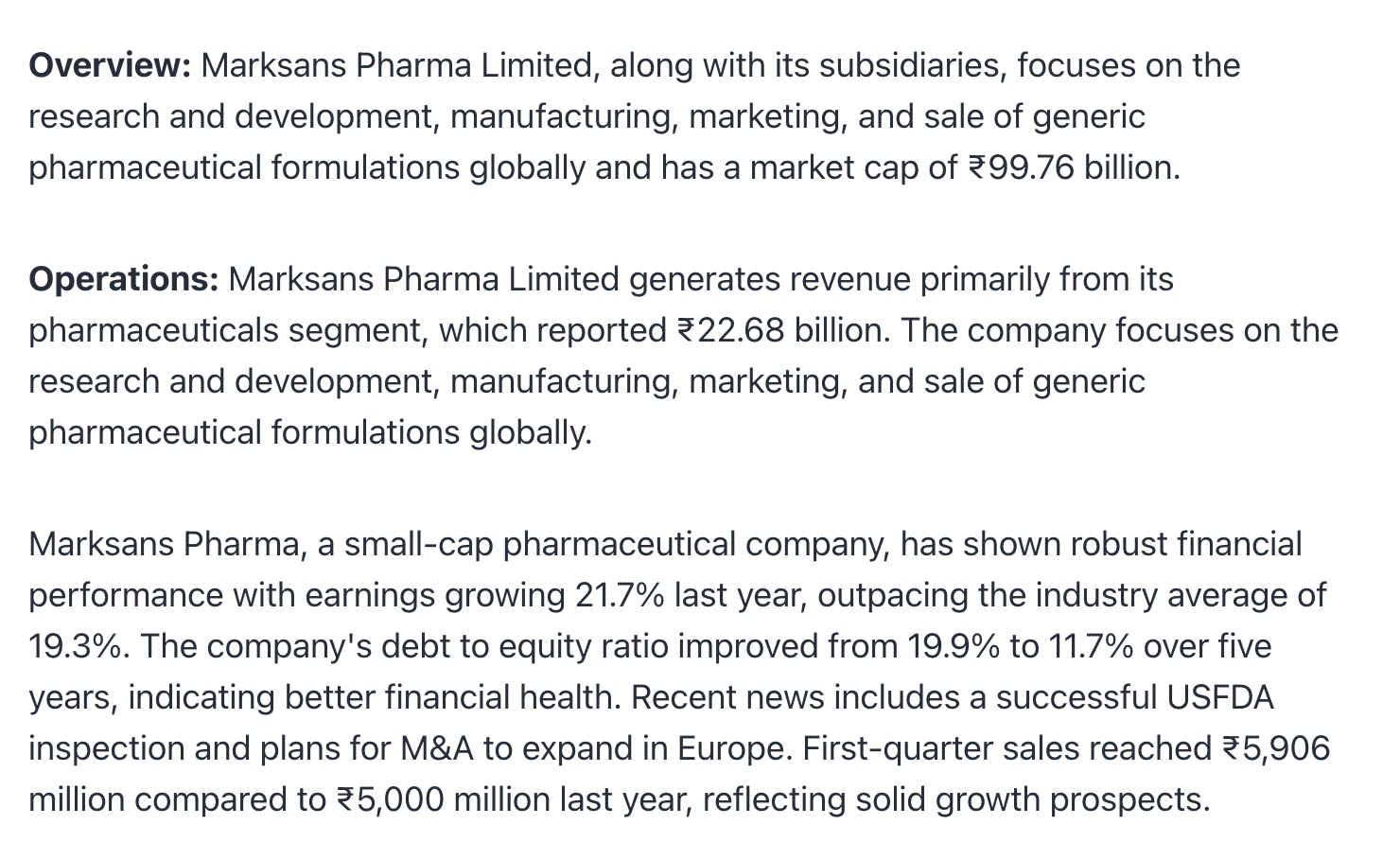

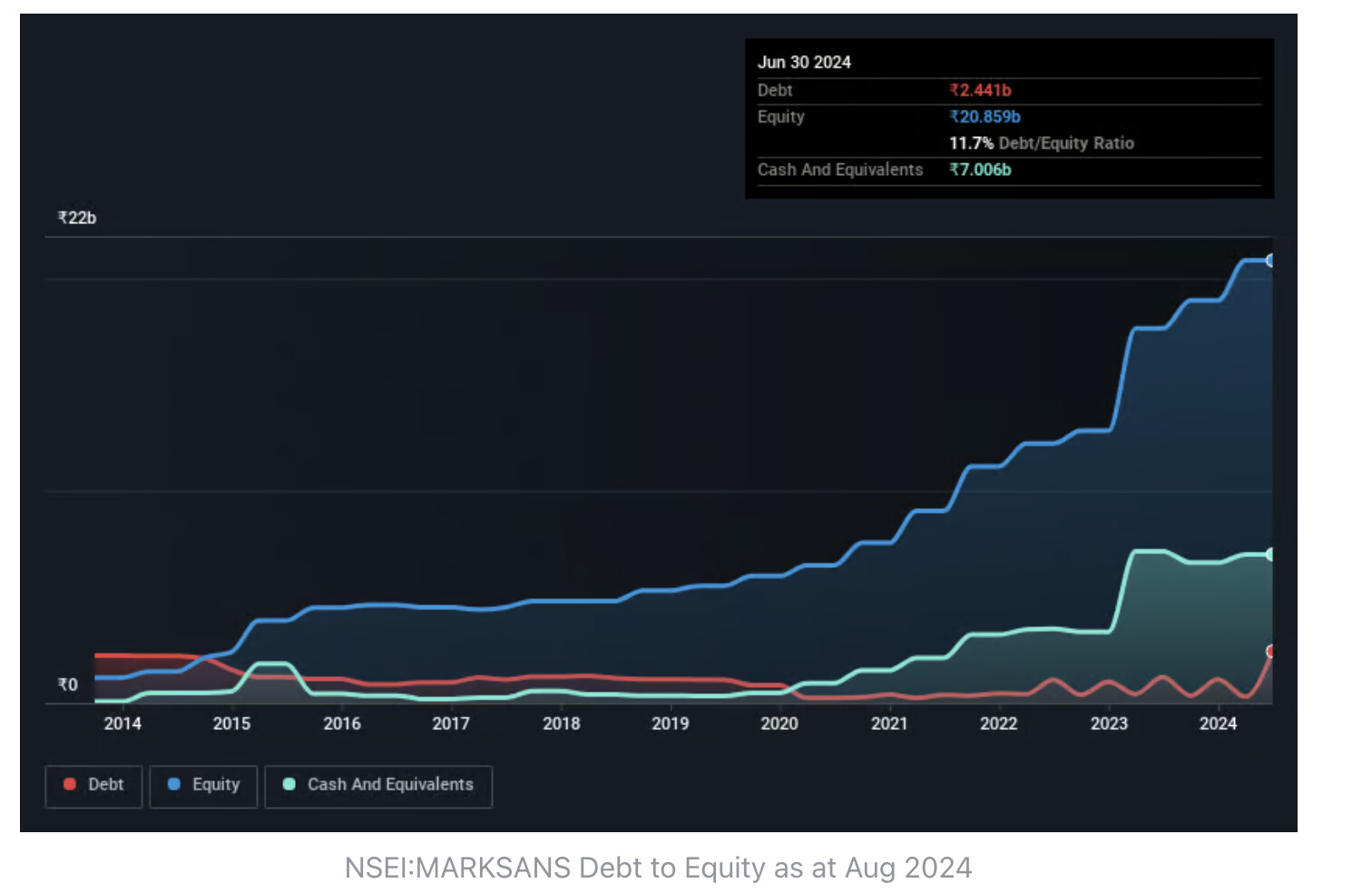

Marksans Pharma- Can it be the next Pharma Biggie? (24-08-2024)

Article:

chart:

PGINVIT impairment of investments in subsidiaries and book value (24-08-2024)

Hi … Anyone who invests in REITS/INVITS can join our telegram group:

https://t.me/+LIxYzAt5brUzMWI1

We will be discussing daily news and announcements around REITS/INVITS

Shakti Pumps – solar shakti (power)! (24-08-2024)

In what would expand the coverage of solar energy in rural areas, the Union ministry of new and renewable energy (MNRE) has raised allocation target for Rajasthan under component A and C of Pradhan Mantri Kisan Urja Suraksha Evam Utthan Mahabhiyan (PM-KUSUM).

Chief minister Bhajan Lal Sharma had written a letter to MNRE minister Prahlad Joshi requesting an increase from the current target to 550 MW under the two Kusum schemes.

As per MNRE’s new order, Rajasthan Renewable Energy Corporation Ltd has been allocated an additional target of 1,000MW, taking the total to 1,550MW. The Centre provides subsidies under the schemes. MNRE has issued an additional allocation of 1 lakh agricultural pumps to be solarised. This allocation is in addition to the 2 lakh pumps previously issued.

Source Link

~ ~ ~ ~

Rajasthan has been one of the states in which Shakti Pumps is a leader in implementing the solar pumps.

Smallcap momentum portfolio (24-08-2024)

@visuarchie

Sir, Hope doing good. Just to let you know that i have started with NSE 500 universe 4 weeks ago and so far its going on good. I felt the draw down was fairly ok (max -4% and currently -0.5%) despite the index has corrected decently.

At present i’m holding top 20 stocks with WRH as 1.5X (retain until rank 30). In the last 4 weeks one thing i observed was, there are few candidates which keep on going out of 30 rank and coming back within top 20 either next or next to next week (so far exited 10 stocks and 2 of them has come back to the top list).

So wondering does 1.5X WRH is too narrow for 500 universe? (i.e. 6% of the universe). Is there any thumb rule or best practice which we can follow? Thought to get your views/thoughts too here pls.

Cheers!!!

Is China investible? (24-08-2024)

Aye aye, Captain ! two cents from a new recruit:

“They say the economic outlook is still weak…” Based on what I read in the weekly Platts report on polymer prices (attached below, from ongoing week, for your viewing pleasure).

There there is also a link which has been discussed on VP >Welcome to the end of the biggest commodity boom – The Economic Times. It’s talking about a commodity oversupply until 2028.

So, maybe I’m still not getting clear direction about the whole China thing, especially since I’ve just started out in this investing game and never tried things with even domestic focused funds .

But who knows? Maybe Turkey’s central bank-based funds might just do better in the short term—if such funds exist! A rookie taking a shot in the dark here.

ITC: “Will”(s) “Gold Flake” assist “Ashirwad” to win “Bingo!”? (24-08-2024)

however unlike in the past, ITC’s FMCG business is showing a lot of traction. Demerger of the hotels business will also unlock value.

ITC is like a fixed deposit for me. My purchase at Rs 190 levels a few years ago is giving me a dividend of nearly 8 per cent which is growing at around 10-12 per cent annually. The demerged hotel biz, other businesses which may get demerged in future and the expanded valuations are all icing on the cake for me.

Samhi Hotels – Turnaround with Tailwinds (24-08-2024)

Hi…

Thanks for the Concall summary. That was helpful

Did they give any guidance on debt reduction roadmap or at what levels are they comfortable with their DEBT/EBITDA or Debt / Equity levels etc

Thanks

Tata Motors – DVR (24-08-2024)

Pls correct if my understand is wrong:

If we go for conversion; the holding period of the shares will start afresh i.e 1st Sept, irrespective of when you bought the DVR. so for someone looking to sell within the next 1 year, better to sell DVR now and pay only LTCG

However since the cost price shall also be determined as the closing price of Tata Motors on 30th August, better to go for the conversion and bring down the profit and hence tax…

Ranvir’s Portfolio (24-08-2024)

Innova Captab –

Q2 FY 25 concall and results highlights –

Revenues – 294 vs 233 cr

EBITDA – 44 vs 32 cr, up 36 pc ( margins @ 16 vs 14 pc )

PAT – 29 vs 17 cr, up 67 pc

Breakup of sales in Q1 FY 25 vs Q1 FY 24 –

CMO – 57 vs 71 pc

Domestic branded sales – 17 vs 18 pc

International branded sales – 11 vs 11 pc

Sharon Bio’s sales – 15 pc vs NIL

14 out of top 15 domestic Pharma companies are company’s clients

Company’s manufacturing units –

02 @ Baddi – can make – tablets, capsules, ointments, syrups, dry powder injections, liquid orals. Capacity utilisation @ 50 pc

01 @ Dehradun – tablets, capsules

01 @ Taloja – APIs

Both Dehradun and Taloja units are acquired units of Sharon Bio. Capacity utilisation at both these units is around 60 pc

New Greenfield unit coming up at Jammu – Multiple products. Likely to go live in Q2 FY 25. Full capacities to ramp up over a period of 2-3 yrs. Its a formulations plant mainly focussed on – Cephalosporins, Penicillin, Carbapenems product families. To make dosage forms like – tablets, capsules, dry powder injectables, dry syrup and respiratory respuels

Jammu facility has a peak revenue potential of > 1500 cr / yr. Likely to be achieved within 5 yrs. Expect to do > 300 cr sales from this plant in FY 26. Should be able to ramp up sales to 900 cr from this plant by FY 28

Company has 01 R&D center at Baddi. Setting up another one @ Panchkula

API prices continue to be soft – both for acute and chronic APIs. At present, company is procuring 70-80 pc of its API requirements from domestic sources. As PLI schemes for the API sector show full effects, company’s domestic sourcing may even go higher going fwd

Company’s margins in domestic + international branded business are > CMO business. However, company has no plans to dramatically change its business mix. They aim to keep growing all their businesses at healthy rates

As the Jammu plant ramps up, company expects to double its revenues and profits in next 3 yrs

Company’s domestic branded formulations are sold under the brand umbrella – ” Univentis Medicare “

As the GoI keeps imposing / being strict on implementation of GMP guidelines iro various Pharma manufacturing units, the organised + compliant players stand to benefit. Its a natural tailwind for the company

In FY 26, if Jammu plant clocks 300 cr sales and company’s base business grows by early teens ( say 13 – 15 pc )- as guided by the management, the total business may grow by > 35 pc !!!

For FY 25, growth should be > 15 pc with similar margins as last FY

Disc: holding, biased, not SEBI registered, not a buy/sell recommendation