Caspia Pro might only add to Q4 revenues.

Caspia Pro might only add to Q4 revenues.

Danish Power Ltd:

About the company:

Danish Power is an ISO 9001:2015, ISO 14001:2015, and ISO 45001:2018 certified manufacturer specializing in various types of transformers and electrical control systems. Their product range includes inverter duty transformers for renewable energy projects like solar and wind farms, as well as power and distribution transformers. Additionally, they provide control relay panels and substation automation services.

Product portfolio:

Key products include inverter duty transformers (up to 20 MVA), distribution transformers (up to 5 MVA), and power transformers (up to 63 MVA).

Cold Rolled Grain Oriented (CRGO) Electrical Steel, Copper Wire, Copper Strip, Copper sheet and Aluminium Wire, Strip, Sheet, Mild Steel, Transformer Oil and Relays these are the raw materials required by the company and procures them either through imports or local suppliers.

Manufacturing facility

Manufacturing facility located at Mahindra World City in Jaipur. And company owns a vacant land in here which will used for expansion plans

Danish Power has received the all India First Licence for Outdoor/Indoor type liquid immersed Distribution Transformers up to and including 2500 KVA, 33KV- Part 3 Natural / Synthetic organic ester liquid immersed as per: IS 1180: Part 3: 2021.

Value chain analysis

Clientele:

Their transformers are designed to ensure efficient power transmission and distribution across several industries, with notable clients like Tata Power, ABB India, and Torrent Power, Waaree Renewable, Jakson Green Private Limited.

Over the years, company has established a diversified client base across different customers in the power industry like renewable power EPC projects like solar power plant, wind power farms, other power generation plants, power transmission, electricity sub-stations, power utilities etc. like Tata Power Solar System Ltd, Waaree Renewable Technologies.

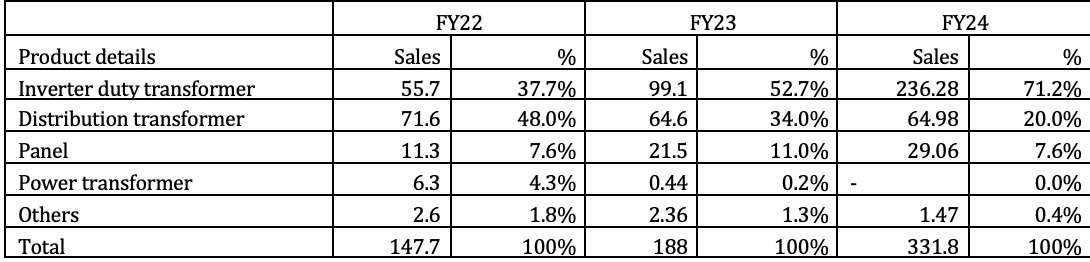

Revenue Mix:

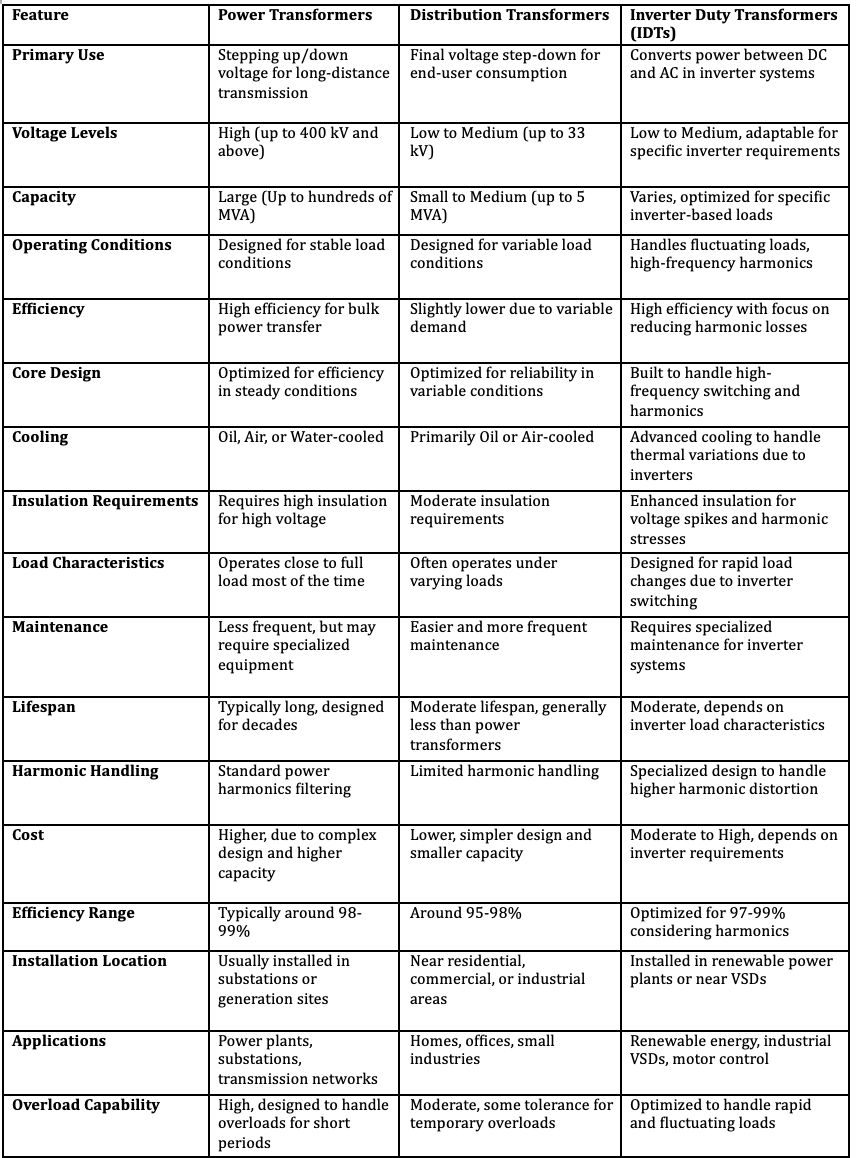

Difference between Power distribution and Inverter duty transformer

Industry overview

• From April 2020 to September 2023, the renewable energy sector in India attracted US$ 6.1 billion in FDI equity investment.

• India has received a cumulative amount of US$ 3.8 billion in foreign direct investment (FDI) in the solar energy sector over the past three fiscal years and the ongoing fiscal year until September 2023.

• India ranked fourth in the list of countries to make significant investments in renewable energy by allotting US$ 77.7 billion between 2015 and 2022

• In the Budget for 2024, the government’s 14 power sector initiatives have been allocated funds that are 50% higher. Increased funds have been allocated to green hydrogen, solar power, and green energy corridors in line with the renewable energy target for 2030.

• In order to meet India’s 500 GW renewable energy target and tackle the annual issue of coal demand supply mismatch, the Ministry of Power has identified 81 thermal units which will replace coal with renewable energy generation by 2026.

CEA: Distribution System Plan 2030

Projected Installed Capacity by March 2030:

• Expected total installed capacity: 786 GW.

• Compared to March 2022: Increase from 400 GW to 786 GW.

• Renewable capacity percentage: Envisaged to be around 62.6% of total installed capacity.

Current Power Sub-Station Statistics (as of March 31, 2022):

• Total number of power sub-stations: 39,965.

• Total installed capacity: 4,82,810 MVA.

Planned Sub-Station Expansion (2022-23 to 2029-30):

• Planned addition of sub-stations: 12,192.

• Total power substation capacity addition: Approximately 1,41,522 MVA.

Projected Cumulative Sub-Station Capacity by 2029-30:

• Cumulative sub-station capacity by 2029-30: Around 6,24,332 MVA.

• Increase compared to March 31, 2022: 29.31%.

National Electricity plan:

The budget outlay for the National Electricity Plan (NEP) for 2023–2032 is ₹9.15 lakh crore.

Planning for Future Demand: The NEP outlines strategies to meet the country’s projected electricity demand over the next 5-15 years, ensuring energy needs align with economic growth.

Renewable Energy Focus: It emphasizes increasing the share of renewables like solar, wind, and biomass to reduce carbon emissions and move towards cleaner energy.

Infrastructure Development: The plan includes proposals for expanding and upgrading the transmission and distribution networks to support reliable power supply and reduce losses.

Energy Efficiency and Security: NEP aims to enhance energy security by reducing dependency on imported fuels and encourages energy efficiency across sectors.

Grid Modernization: Focus on modernizing the power grid with smart technology and digital solutions, including battery storage systems, to handle renewable energy’s variability.

Support for Universal Access: Prioritizes providing electricity access to all households, particularly in rural areas, contributing to socio-economic development.

Five-Year Update Cycle: The NEP is updated every five years to reflect technological advancements, policy changes, and shifting energy demands, keeping it relevant to current needs.

Growth in Transformer Allied products

Transformer Oil market 2028 $3 Billion 5.90%

Oil immersed transformer market 2028 $28.2 Billion 6%

Transformer monitoring market 2028 $3.7 Billion 9.10%

CRGO steel market 2032 $20 Billion 5.90%

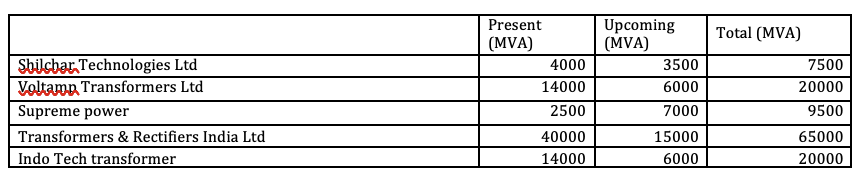

Peers capex plans

Growth Triggers

• Diversified Product Base

Key Risks

• Reduction in Govt spending in capex could result in lag in revenue recognition.

• Delay in Company’s capex plans could affect the guidance given by the company.

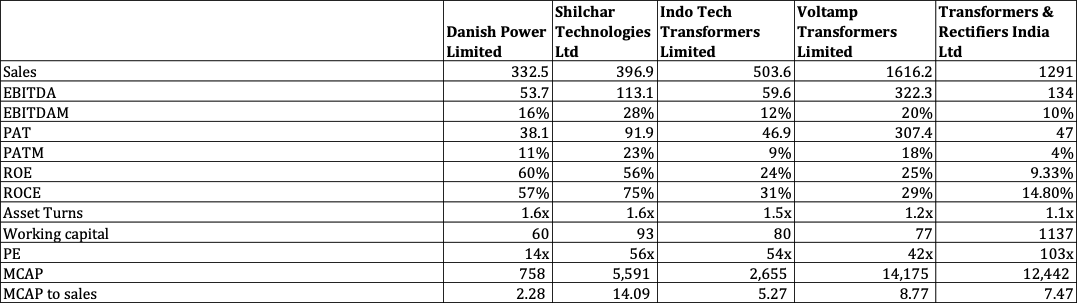

Peer comparison

Assuming Shilchar realization per MVA is 10Lakhs and capacity fully utilized at 7500MVA.

Here Danish power is compared with Shilchar Technologies is because of their similarity in product profile.

Conclusion

Danish Power Ltd. is an attractive investment opportunity in the growing renewable energy and transformer manufacturing sectors in India, especially with the government’s goal of achieving 500 GW of renewable energy by 2030. The company boasts a diverse product portfolio, including inverter duty transformers essential for solar and wind projects, and is expanding its capacity from 4,681 MVA to 11,000 MVA to meet increasing demand. Danish Power is well-positioned for sustained growth with a solid financial performance, established relationships with key clients like Tata Power and ABB India, and a favorable forward price-to-earnings ratio compared to peers. Despite potential risks related to government spending and capital expenditure delays, its proactive strategies and experienced management make it a compelling choice for investors looking to benefit from India’s renewable energy boom.

Disclosure: Invested since IPO levels and Biased

@Cshar – when you say large position – how much in terms of % of portfolio ?

SG Mart Concall Notes:

Volume:

Service Centers:

Steel Prices:

Margin Guidance:

Business Segment Sales:

Disc: Invested

An analyst, Vivek Patel, asked a question regarding the risks involved in the business.

Another question asked by Alisha Mahawla

Management said they purchase in bulk, so they get a discount and maintain inventory days of 10 days. They mentioned that the volatile steel price won’t affect the margin. I think management is too optimistic about the business. If they can’t pass the increased cost to the customer, that won’t benefit the business.

Disc: Invested

Below is a write up I wrote on the holding period in Small & Microcap Space:

“In 1988, Warren Buffet famously said, ‘Our favorite holding period is forever.’ This quote has become a tagline for many investors, including me. But on thinking and evaluating this quote, I find it to be misleading.

Many investors, including myself, when reading Buffett’s shareholder letters for the first time, took this quote literally. However, Mr. Buffet’s real intention was to convey the message that he intends to buy stocks he can hold forever. So, in 2016, after he got sick of people misinterpreting his statement, he said, ‘Sometimes the comments of shareholders or media imply that we will own certain stocks “forever.” It is true that we own some stocks that I have no intention of selling for as far as the eye can see (and we’re talking 20/20 vision). But we have made no commitment that Berkshire will hold any of its marketable securities forever.’

This makes one thing clear: in investing and in life, a person’s intention matters the most. Here’s the difference between trading and investing:

In Trading: A person’s intention is to sell the stock, while,

In Investing: a person’s intention with every purchase is to hold it.

His intention was to hold his stocks forever, but as the business or macro situation changed, he sold them, though he made good money on them (that’s a different topic). This proves what we know to be true, but don’t like to admit: all stocks have different shelf lives.

Shelf life refers to the amount of time until a commodity or food is consumable without being unfit for consumption. For example, vegetables have a shelf life of 2 to 3 days, fruits 5 to 7 days, milk 1 to 2 days, and pickles 1 to 1.5 years.

Just like food, every stock or investment in your portfolio has a shelf life. The difference between food and stocks is that we know the shelf life of food, but with stocks, we don’t know the shelf life when we buy them. There’s no one-size-fits-all approach to estimate it as all businesses evolve differently. Some are gradual compounders, and some are momentum sprinters. This also differs from investor to investor.

Now, if I ask you to define your stock holding framework, many of us would define it with an exception rather than a norm, like: ‘I do deep research and understand different businesses and industries and identify a handful of wonderful businesses that I buy and hold forever.’ Isn’t it funny? Like Mr. Buffet, maybe only 2 out of 50 businesses you analyze would be worthy of owning for 10+ years. They are exceptions, not the norm, as not every business is in the buy-and-hold category.

We love to define our investing strategy as finding those 2 wonderful businesses, but in reality, our investing strategy depends on how we deal with the remaining 48. We can still make a lot of money on those 48 because what I realise is that finding those 2 business is also a matter in which luck plays a significant role and apart form finding those 2 business it also becomes equally important to get allocation and execution right.

But here’s the dilemma no one in the market likes to talk about: the skill of selling. It’s an admission that either your thesis is wrong or that ‘you don’t hold stocks forever.’ Admitting you are wrong means you are not perfect, and no one wants to admit that they are not perfect – though none of us are.

My intention with every purchase is to hold the stock for 5+ years, but less than 5% of the stocks meet that criteria of a wonderful business. Thinking on this line, I did an assessment of my own portfolio, and the results were quite surprising. Over the last 5-6 years, I invested in 40-50 companies and held only 3 stocks for more than 5 years. My average holding period across my stocks was 2.5 to 3 years, as I invest primarily in small and microcap companies. The natural shelf life of such companies is shorter than that of mid and large-cap businesses.

I’ve observed that in Indian Markets, for a small and microcap business, that shelf life is 4 to 10 quarters. In this part of the market, it also becomes equally important to evaluate management as small-cap investing is mainly surrounded by evaluating whether management is lucky or skillful and how long it will last.

And also, most small and microcap investors, including me, try to fit too hard into the camp of ‘buy and hold forever,’ but the shelf life of most small-cap companies is 2.5 to 3 years. I’m trying to be more aware of this issue and figuring out ways to avoid it, but I still haven’t got a proven way.”

This is my way of thinking and this may apply to only me but, I am just trying to share my thoughts and as a learner we should always endevor to develop our own thinking and though process as in life and investing borrowed skill and conviction are harmful.

In past few days or say weeks got little busy in some family event due to which I couldn’t update my blog but hereon I’ll try to share my thesis as often as possible and update it as well.

Time Technoplast is a company which I invested with when the current leader Mr. Bharat ji Vageria came in had visited there facility back when Anil Ji was heading the company and looking at the corporate history of the company, it was always a technocrat company bringing in newer technology in IBC and Chemical Packaging space but took a hit in terms of poor capital allocation & management not walking the talk, but with coming up of new leadership this problem started to get resolved and focus of new Mgmt started shifting from low margin established product range to better Margin Value Added Product Segment, easing out of corporate structure, selling of non-core assets in form of land parcel at Karnataka on which earlier mgmt planned to do real estate business.

One Mental Model I use is

Great Business – High/Better Margins & High/Better Turnover

Good Business – Better Margins & Low Turnover

Okayish Business – Medium Margins & Better Turnover

Gruesome Business – Low Margin & Low Turnover

So when Management shift from Okayish Business to Good Business Markets starts to appreciate the fact… as value creation starts to get better.

Below I have shared my thesis in the form of small write up

Time Technoplast Limited Report.pdf (1.1 MB)

On 16.04.2024 in blog of Time Technoplast I wrote

Time Technoplast is a medium term bet and the internal business is cyclical in nature but right now the company is in sweet spot because

Hello, I would like to join the WA group, have sent the request.

Vikas ji!

Since I’m a bit of an “action hero” in the market (read: click-happy ![]() ), I’m always itching to buy something… usually one stock at a time, then more if it drops. And in this bull market, if it doesn’t rise, well, nana-mota position gets the chop!

), I’m always itching to buy something… usually one stock at a time, then more if it drops. And in this bull market, if it doesn’t rise, well, nana-mota position gets the chop!

For me:

Have you or anyone from “Finance Samaj” here have checked out this RAC story yet?

Untill you have concentrated bet, you wouldn’t be able to make it meaningful, there are risk associated with large bet hence valuation comes in picture, mostly turnaround, forgotten by markets or stocks sitting at cusp of growth triggers. You need some luck as well. Higest the safety of margin, higher the chances or capital protection if events not unfold as you thought.

I have done it repeatedly in last 7-8 years with 80% success rate. Its an art which requires lot of courage and patience, holding a rising large position is more problematic. I have done it with Vodafone Idea, Tata Motors, Shoppers stop, ABFRL, Latest Kalyan Jewellers, Started with 25K stocks in Nov 22 at 115, diluted 2K at 300, diluted 5K around 500, diluted 4K around 650, diluted 11K between 700- 750 as its too expensive for me now, holding 3K, will sell it again as Istock is discounting 2 year forward earnings and competition is heating up after entry of PN Gadgil, Novel Jewels, PC Jewel, Senco and other small IPO’s. This sector is avoid for me know.

Built up a large position in SAMHI hotels which is trading at 10 EV/EBIDTA own 90% of real state, discounted around 50% with marque brands like Merroit, IHG, Hyatt. Can’t lose much from here.