FY24 annual report is now published. Mangalam Brands reported revenues of Rs. 160 crore in FY24, up from Rs. 100 crore in FY23. The company targets Rs. 500 crore revenues over the next 3-4 years as per management commentary. That should see the transformation from B2B operations to a mostly brand driven business that is less susceptible to margin volatility…

Posts tagged Value Pickr

Aptus Value Housing : Is valuation justified or just another HFC? (21-08-2024)

That’s obvious and I’m not trying to understand how dividend payment helps ROE of a company.

My point was that dividend payment should the last option for the companies when they don’t have any use for the capital. So it’s fine for a company, generating loads of operating cash flows, to give dividends for lack of better opportunity for that capital.

For financial companies, capital is the key raw material and continuous supply of it is key to their operations. So if Aptus is raising capital from the market, market would expect them to put that to work and generate interest income and not pay dividend to boost ROE. If they didn’t have opportunity for that capital then why raise it in the first place and expand their balance sheet?

And the most importantly, improve ROE to what end? Such inorganic tactics to improve ROE are not lost on the market and won’t benefit stock prices if company is not delivering on core operating metrics.

Kamat Hotels (India) Ltd- A Possible Turnaround Story! (21-08-2024)

Few clarifications from my end:

-

Why only NCD redemption cost is there in Q1FY25. What about the interest cost of debt from Axis bank, it should be spread out over the whole year?

-

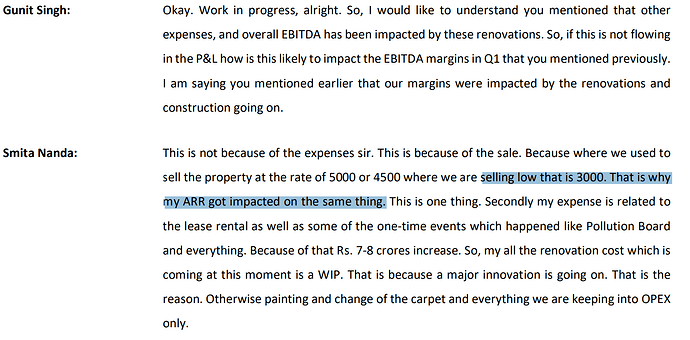

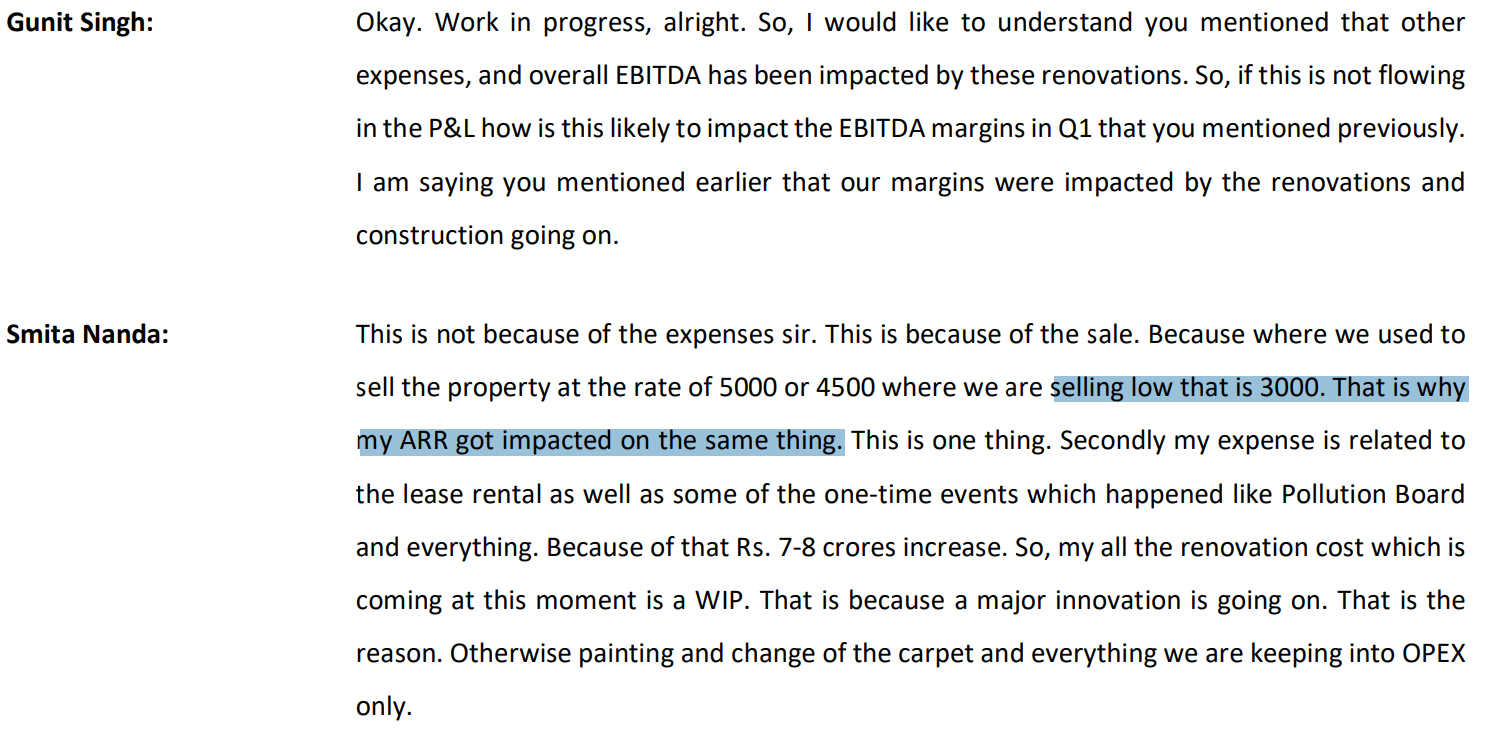

They had posted 91 Cr EBITDA in FY24. 140 Cr is ~54% jump which is not possible without adding a lot of keys. Also, they have shown 0 key progress from Q4FY24 to Q1FY25. They haven’t mentioned any other keys in pipeline other than the ones being shown from last 1 year.

-

ARR halving was mentioned during the concall by CFO

-

I think FY26, it’s possible but guidance is for FY25. Or is it a typo from your end?

Nitta Gelatin India Ltd | (21-08-2024)

From Crisil rating update report released yesterday link

“The group plans to incur a capital expenditure (capex) of ~Rs 250 crore over fiscals 2025 and 2026 to expand capacity in its gelatin and collagen peptide unit. It has announced withdrawal of its proposed rights issue of Rs 40 crore to fund the above capex and plans to finance the proposed investment through a mix of internal accrual and external borrowings. Though this could be partly debt-funded, financial risk profile is projected to remain comfortable on the back of expected annual cash accrual of over Rs 50 crore and adequate liquid surplus, which stood at Rs 76 crore as of March 31, 2024.”

Websol energy system ltd (21-08-2024)

Dear friends,

Premier energies IPO opens for subscription from 27th Aug 2024. Market will decide the valuation of pure play Solar cell and module manufacturer’s. Premier energies has 2 GW Cell & 4 GW module capacity with an order book of close to 6000 Crs. Though, it has presence in other verticals like EPC, IPP & O&M, the order book is negligible.

Waaree energies is valued at Mcap/sales of 8x in unlisted zone (FY23 sales).

Let us hope that listed competitor Websol energy gets benefited with the same valuation of 8x to FY25 sales from market as it has better margins than others as of now. Fingers crossed. Please share your views.

https://www.moneycontrol.com/news/business/ipo/solar-module-premier-energies-ipo-12803094.html

Kovai Medical Center and Hospital – Health and Wealth (21-08-2024)

Did they give any timeline for getting to 2000 Cr revenue. Also, any comments on the operating margin from management side?

Is the entire 300 Cr capex going to be utilized from internal accruals or debt or equity raise?

Varun beverages fast growth duopoly business (21-08-2024)

As per last updates PPT for VBL, seems Indian market is expanding.

Aptus Value Housing : Is valuation justified or just another HFC? (21-08-2024)

Another way to look at it:

Paying Dividend is another way of bumping up the RoE nos with a few bps. So, the payout made from the Reserves decreases the Overall Book Value/Networth of the company which in turn increases the RoE %.

This logic makes sense for a company clocking decent growth (though less than its potential) but still managing to stick around a 17-18% RoE numbers. Cause when a company grows at 25-30% and they fail to show the similar kind of growth in subsequent years, its RoE decreases.

So, paying dividend is an easy way to keep the Networth under check and maintain a consistent RoE.

Unemployed investors portfolio (21-08-2024)

Bought infollion research

Tasty Bites: A proxy play to India’s QSR industry (21-08-2024)

Well, the stock price went from 17.5k in August 2023, to 14k now, while going as low as 9.5k in the middle. Glad I had exited in August 2023 itself.

PE expansion because of earnings contraction is not a good thing imo.