“Deposit growth isn’t slow because people are buying stocks and financial derivatives. That’s rubbish. It’s slow because the RBI wants it to be slow.”

Posts tagged Value Pickr

SWAN ENERGY LIMITED (SEL): The company focussing on sectors with strong tailwinds (20-08-2024)

The remaining stake in Triumph offshore pvt ltd(remaining 49%), was acquired from IFFCO by swan energy in june 2024 for 440 cr.

now TOPL is 100% subsidary.

Hitesh portfolio (20-08-2024)

Sir, is there any reason why you use GMMA instead of individual MAs? Do they provide any additional insight?

Indiamart Intermesh – Indian Alibaba? (20-08-2024)

Does anyone have any recent data on Trade India( What are their revenue, profits, and stuff )?

Rei agro price shown 95 INR (20-08-2024)

Hi Guys, I am just wondering how come ICICI Direct is showing REI Agro price as 95 INR though this stock is not traded since 2017 and is in liquidation. Even one user had posted on Moneycontrol that he is also seeing same price on HDFC securities. I was invested in this stock and in portfolio it started showing 95 rs however if you search the stock price it shows 0.24 rs

Companies with 20%+ growth guidance for next few years (20-08-2024)

I do not have any evidence of CG issue. However, generally I do not prefer companies with multiple subsidiaries in its structure.

Disclosure; My views are only for academic discussion and not recommendation to buy or not to buy or sell or hold.

HDFC Bank- we understand your world (20-08-2024)

That’s already factored in stock price to book. Book value per share will go down with equity dilution. So current multiple of 2.7 times is after reduced book value.

RBI ruling regarding CDR applies to all the banks so yes it’s an argument to use if one is bearish on the entire banking sector but it doesn’t exclusively impact HDFC only.

With interest rate cuts banks will again go back to raising capital from the market. Big picture is that if we are bullish on Indian economy, banks need to participate in that growth. As investor we can’t lose breath over all micro-developments.

Natco Pharma: Focusing On Complex Products (20-08-2024)

Mr.market doesn’t like uncertainty in earnings. In the case of Natco Pharma it is clearly visible that earnings will definitely fall after 5-6 quarters from now and after that it will take some time to recover back to its growth trajectory. But current liquidity in the market can drive any share up and up and can give company any valuation. Natco Pharma is primarily focused on Para IV and not on the innovation of a new drug. If natco pharma with its high cash balance spends properly on R&D and innovates a new drug then we can see sustainable growth in earnings and higher valuation for the company similar to innovators. But i thing the company is not in the mood of innovation rather copying a drug and doing a para IV filing or inorganic expansion.

Disclaimer: Invested in the company

HDFC Bank- we understand your world (20-08-2024)

Stock price increase doesn’t have to come from just rerating. Earning growth is also an important factor and so far bank earnings haven’t slowed down.

Moreover, multiple rating has got nothing to do with asset mispricing. Mispricing is when market is not rewarding earning growths for a stock at the average sector valuation. Valuation rerating and derating are more driven by sector dynamics and collective wisdom, of the market participants, about the future of a sector.

Every sector goes through cyclicity in valuation ratings. Take IT sector in 2022 and 2023. All the stocks got badly derated and we saw the arguments from naysayers telling that IT story is done (with typical threadbare analysis of their valuations, business prospects etc). All IT stocks got beaten which doesn’t mean that market was mispricing them for 2 years. It’s just that market was pricing them at their earning growth on depressed sector valuation.

Market changed its mood about IT sector in 2024 and started rerating the sector even though earnings still haven’t started to come through. I can provide similar data points for the other sectors.

Coming to financial sector, all the private players (Kotak, Axis, Bajaj Fin, Indusind) have seen their multiples getting derated due to various external factors well summarized in this thread.

So when the rating cycle for banking industry turns and HDFC bank doesn’t benefit then it will make sense to analyze all the things wrong with the bank and pricing aspects. Before that making any predictions about stock prices is futile.

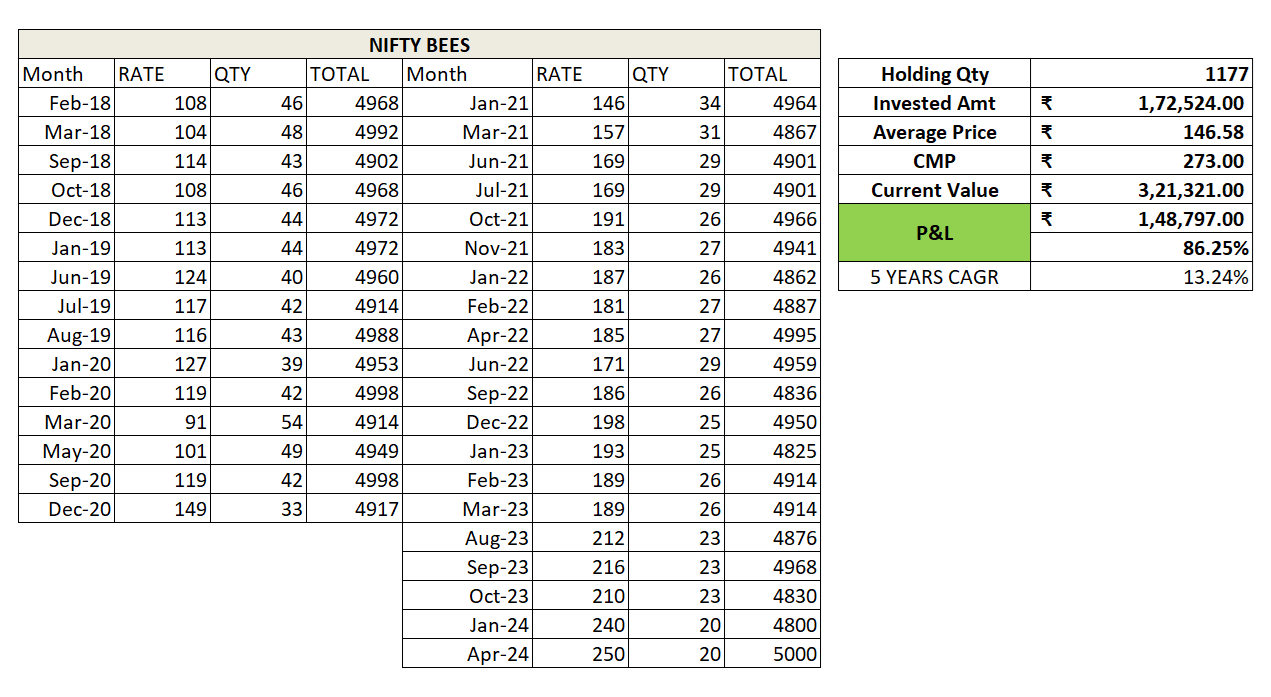

Stock SIP boring yet powerful (20-08-2024)

Nifty Bess Jan-18 to Aug-24

SIP Amount : 5K