Posts tagged Value Pickr

Nath Bio-Genes ….. Seeds player (18-08-2024)

Why did management not publish any presentation after the Q1 25 result or make any

concall?

Modison metals (18-08-2024)

Q1 2025 results are out and do not meet the market’s expectations. No wonder this company is the market leader in HV/LV switchgear contacts and has been doing business for more than 60 years but has not developed a moat in business. Their business prospects are up/down due to commodity price fluctuations.

this quarter’s gross profit margin is less than 1%

Silver hedging loss 3.75 cr and profit 1.14 cr.

Invested and sold 50% holding after Q1 25 result.

Caplin Point Laboratories (18-08-2024)

Another sucessful completion of inspection at Caplin

ANVISA- Brazil conducted an inspection of Caplin Steriles’ injectable and ophthalmic manufacturing facility located at Gummidipoondi. The inspection was conducted between August 12th and 16th, 2024 and concluded with zero observations

This will help Caplin to get into Brazilian markets and eventually to Chile and Peru. Thier business model is based on opening of warehouses in the country they enter and establish distribution, this sucessful inspection means that they will be able to cater the brazilain markets with more products of better quality and when their products portfolio reaches 30+ they can open a warehouse in Brazil ( with fewer products warehouse in not economically viable according to the management )

Quarterly results also robust and management commentary also encouraging

Disc : Not a buy/sell recommendation. Not Sebi registered.( Invested )

Vaibhav Global ~ Vertically integrated value e-tailer of Jewellery and Lifestyle Products (18-08-2024)

Consumer sentiment and GDP growth (in US at least) has actually been robust going by news reports so why is VGL unable to capitalise on that sentiment? If mgmt couldn’t deliver results in such a robust macro economic scenario where GDP grew despite all time high rates, how will the mgmt deliver results when Fed starts cutting rates or a recession hits US ? Price might be right to enter at this point but can’t trust the mgmt which doesn’t deliver results in good times too! That might be indicative of a flawed business model.

Indiabulls Housing – A compounder from here? (18-08-2024)

The company has Rs 37,380 Cr of legacy loans (housing + developer finance) on their balance sheet as of June 2024 as per their Q1 earnings update. The market seems to be saying that all of this book will likely go bad (maybe that’s why they haven’t been able to unload it yet in the first place) and given their track record of 70% recovery from bad loans, the hit will be to the tune of Rs 11,000 Cr. Hence, discounting the same from their current net worth of Rs 20,000 Cr gives you Rs 9000 odd Cr of market cap.

However,

a) the company already has imputed provisions of Rs 6000 odd Cr from the written off pool which the market is not accounting for, and

b) not all or even a majority of the legacy book is likely to go bad (my opinion)

Nevertheless,

The management seems to be indicating that a substantial portion of the legacy book is likely to be unwound after requiring some provisioning and that’s why there is no talk of write-back of provisions from the expected recoveries (and all the jargon around “tactical” actions to reduce the legacy book which is nothing but another way of saying that we will require to provide for some part of the outstanding legacy loan book before either offloading it or running it down over the normal course of loan repayment)

Lastly,

All of this ultra cautious approach could also be a ploy by the management to keep the share price depressed till 30-Sep-2024 when the optional put option will be exercised by the FCCB holders. If the share price were to rise before that, the FCCB holders could simply exercise the conversion option and add 5 Cr shares to the already large number of diluted shares after the Rights Issue. The FCCB conversion price is somewhere in the handle of 200 Rs per share but am not sure.

The management is also working on another ESOP plan which was approved by the board in Feb 2024 but implementation was deferred till after all the name change and KRAs for performance evaluation (the eight metrics they started reporting on since Q1)

were implemented. Lower the stock price, lower the strike price for their ESOPs since ESOPs are awarded at the market price of the day to avoid P&L hit.

My take on business performance going forward –

The increase in profitability will be gradual but steady over the course of next 8 quarters. The management will ensure that there are no surprises on the positive or negative side going forward. Not sure about the figure of 4000 Cr p.a. as I still don’t understand how the ROE of 18% will be achieved without substantial leverage. If the 18% ROE is after accounting for provision write-back sometime after 2027, then it is not sustainable.

At some point well within the next two years, the market will get enthused by the steadily rising asset light AUM and earnings as well as reducing legacy book and assign a higher book multiple to the share.

Disc: Invested with a large holding

Sky Industries Ltd – Footwear,Automobile manufacturer Major customers (18-08-2024)

sky industries is merging their two manufacturing facilities and shifting to another location, credit rating has been upgraded. Any views or update on this by any friend.

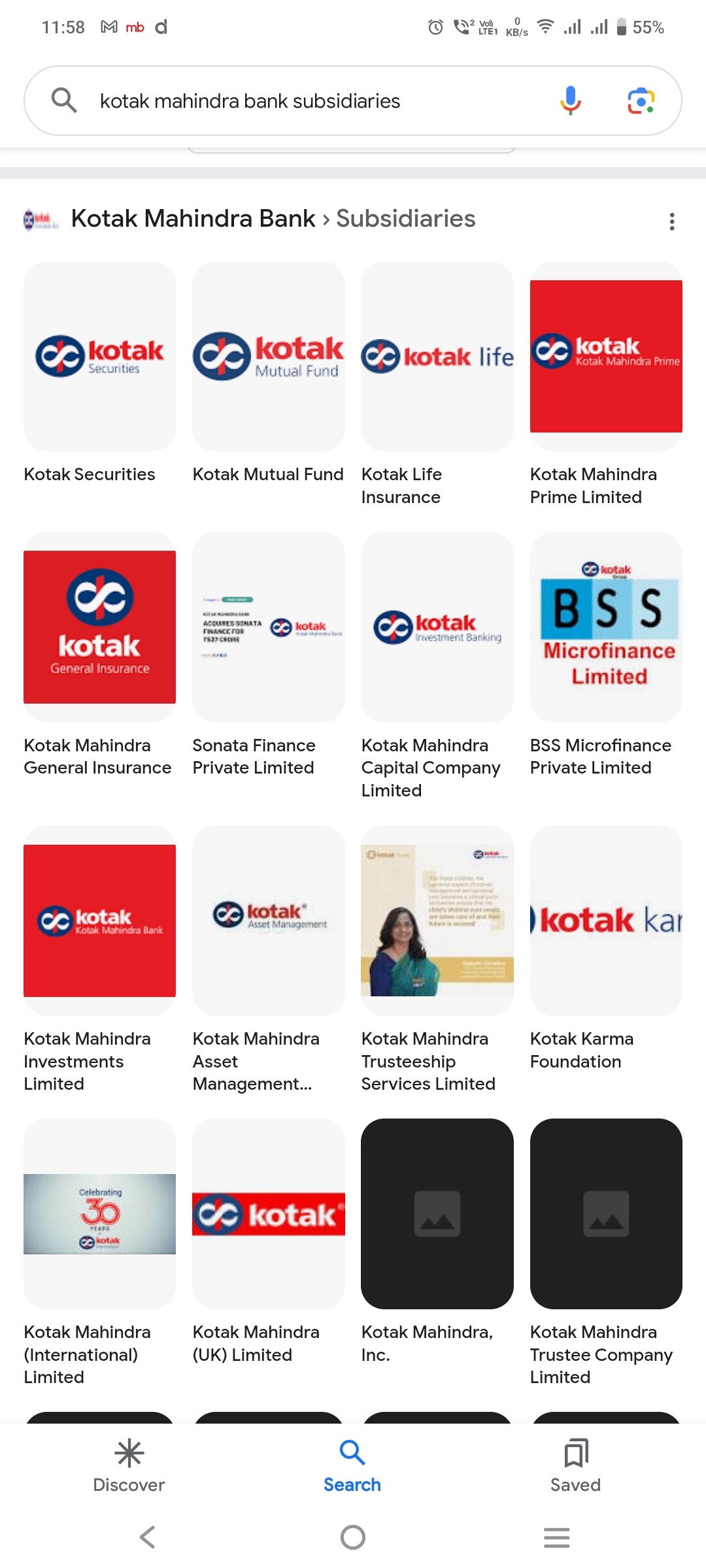

Kotak Mahindra Bank – Low Cost Liability Banking Franchise (18-08-2024)

Unlike other major banks, Kotak Mahindra Bank has unlisted major subsidiaries. Ideally kmb should get better p/b value compared to all other big banks.

Borosil Limited (18-08-2024)

Here’s a summary of the key points from latest Investor Presentation:

Financial Performance for Q1 FY25 (Quarter ended June 30, 2024):

- Net Sales: ₹216.8 crores, up 23.2% year-over-year (YoY)

- EBITDA: ₹36.7 crores, up 74.9% YoY

- EBITDA margin: 16.0%, improved from 13.6% in Q1 FY24

- Profit Before Tax (PBT): ₹12.9 crores, up 80.4% YoY

- Profit After Tax (PAT): ₹9.3 crores, up 87.6% YoY

- Net Debt: Reduced to ₹57.8 crores from ₹94.5 crores in the previous year

Segment-wise Performance:

- Glassware: ₹55.7 crores, up 42.2% YoY

- Non-Glassware: ₹85.1 crores, up 20.3% YoY

- Opalware: ₹76.1 crores, up 15.0% YoY

Other Key Insights from the commentary/slides:

-

Strong overall growth: The company has shown robust growth across all segments, with total consumer ware sales increasing by 23.2%.

-

Improved profitability: Significant improvement in EBITDA and PAT, indicating better operational efficiency and cost management.

-

Debt reduction: The company has reduced its net debt, strengthening its financial position.

-

Diversified product portfolio: Borosil has successfully expanded from being primarily a glassware company to offering a wide range of consumer products including non-glassware and opalware.

-

Market position: Borosil is positioned as one of the leading brands in glass microwavables and claims to be the largest opalware player in India.

-

Future growth strategies: The company aims to achieve a revenue CAGR of 15-20%, improve EBITDA margins, and optimize capital employed through various initiatives including increasing penetration of glass storage and opalware, introducing innovative products, and accelerating e-commerce growth.

-

ESG focus: Borosil has outlined strategic ESG priorities, including aims to achieve carbon-neutral operations, create a positive water balance, and focus on waste management opportunities.

Disclaimer: Holding part of tail end of LT PF. No recos., No transaction in last 30 days.