This is more of a platform based company rather than a trading one. Agreed that the margins are low and will always be low because of the nature of the business but the ROCE will always be very high. I think it is 51% right now. The cash flow should also be very good unless it gets stuck in inventory. So valuation wise I would say it is cheap at a PE of 40 if you were to think of this as a pure platform based company.

Posts in category Value Pickr

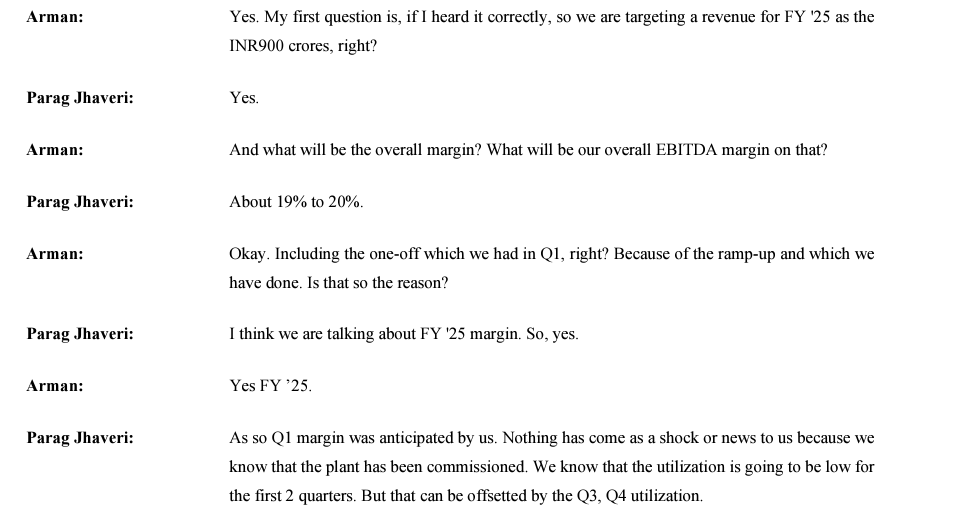

Yasho Industries (13-08-2024)

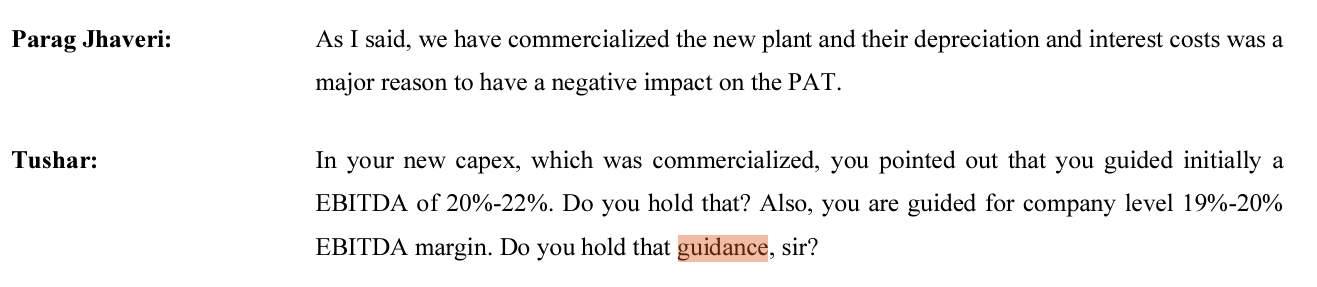

Maintains FY25 revenue and margin guidance despite weak 1QFY25

Maintains FY26 revenue guidance

Spandana Sphoorty Financial Limited – An Efficient Player (13-08-2024)

Currently, there is a lot of competition in the microfinance space, and everyone wants to take a piece of it. But what actually happens is willfull defaulting customers are easily shifting from one MF lender to another and defaulting on the lender whom they have borrowed in the past. I am staying in a village, it was really tough to get a loan before COVID by an illiterate villager, but after COVID, I see about two to three microfinance loan officers every week in my village asking villagers to avail loans from their companies. I think this is going to be a be a bubble. If they want to get protected from bubble then they have bring changes in the way they are giving loan.

Piccadily Agro Industries Ltd (13-08-2024)

Assuming some of these investors know the business plans of promoters!

Prevest Denpro Limited (13-08-2024)

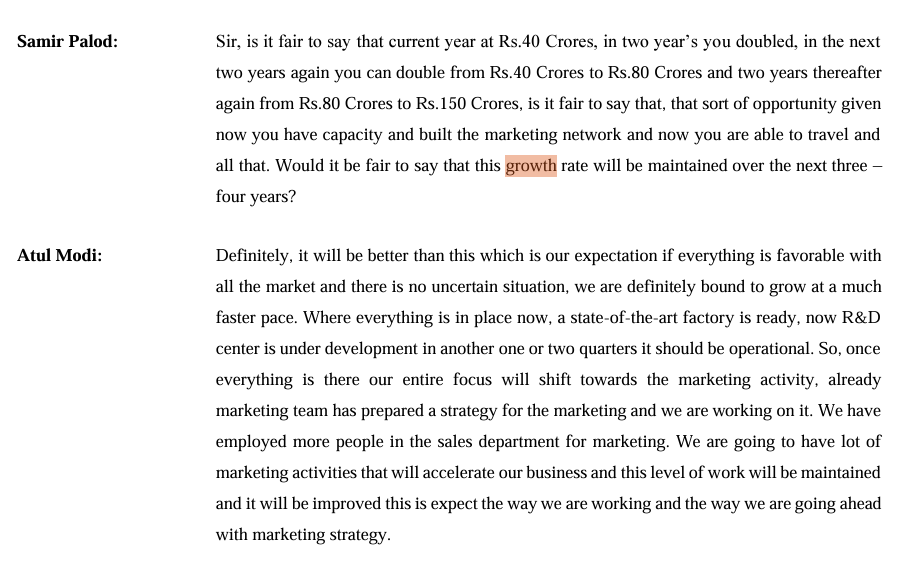

May 2022 – FY22 Year End Call

Atul Modi saying they can more than double FY22 revenue of Rs38 crores in 2 years and then double again to Rs150 crore. Two years later we are at Rs 56 crs

Company had mentioned they will maintain margins. Margins came down from 40% to 34% in 2 years

May 2023 – FY22 Year End Call

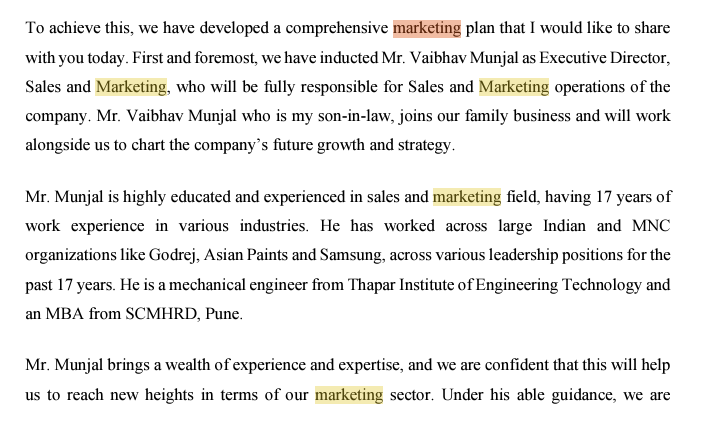

Heights of Nepotism. Making son in law ED, Sales and Marketing. What happens next? No sales growth in FY24.

The lack of growth continues in 1QFY25. Why cant such a tiny revenue base not be grown?

Piccadily Agro Industries Ltd (13-08-2024)

Hi Gaurav,

Rs 3000/ per bottle MRP includes excise duties and other levies , distributor margins , market spends and other overhead charges . you should always see sales net of excise duties . Also PAIL is a single brand company whatever other brands they have are in developmental stage. PAIL has one of the largest malt spirits plant in India and they sell large quantity of bulk malt spirits to other players .

Establishing a single malt in international and domestic markets requires deep pockets and investments and you are competing with Diageo’s Pernod’s . William Grants, LMVH brown Forman’s and Bacardi’s of the world who have products in all categories of alcohol i.e Scotch . American whiskies , vodka , Rum , Tequila Gins etc. Also PAIL management is also not quite transparent and belongs to political family infamous Manu Sharma.Indri as brand is doing well and is among leading single malt from India .

Shree Ganesh Remedies Limited (SGRL) – A pioneer in API intermediaries and Speciality chemicals? (13-08-2024)

Few highlights of first detailed presentation by the Company:

- Higher margin biz (Specialty chemicals) to contribute >60% in future (currently it seems 40%)

- In Specialty

fb8f6228-4032-48c5-bca4-11aa4e99ca06.pdf (4.4 MB)

chemicals:

a. Evolved from 20-50 tonnes/year to 80-100 tonnes/year, now

receiving inquiries for > 500 tonnes per year

b. At inflextion point, scaling up with global giants - 40 team of R&D: 20 PHDs

- Marquee client: BASF, Laurus, Aarti, Dipharma, Lonza, Cipla

- Land parcel available for future expansion

- Block 8 is operational since Q1 FY’25, to contribute meaningfully in Q3 FY’25

- Block 7 to be completed in 18 months (Dec’25): production of complex, niche specialty chemicals using automated plants, targeting low volume, high-profitability molecules

- They focus on products requiring 3-4 different chemistries rather than just 3-4 reaction steps reducing competition

- enter into product which fits their margin profile

- Sustainable EBIDTA: 24 to 28%; last two quarters higher EBIDTA due to RM pricing

Awfis Space Solutions: Flexing its Muscles in the Market (13-08-2024)

Awfis faces competition from several other players in the flexible workspace and co-working industry. Here are some of its primary competitors:

-

WeWork India: Part of the global WeWork brand, WeWork India offers premium co-working spaces across major cities in India.

-

Regus (by IWG): Regus provides serviced office spaces and co-working spaces, catering to businesses of all sizes. It has a significant presence in India.

-

91springboard: A popular co-working space provider with a focus on fostering startup communities, 91springboard operates in multiple cities across India.

-

Cowrks: Cowrks offers premium co-working spaces in several major Indian cities, targeting a mix of startups, SMEs, and large enterprises.

-

Smartworks: Smartworks focuses on providing enterprise-grade co-working spaces and managed offices, with a strong emphasis on technology and infrastructure.

-

Workafella: Operating primarily in South India, Workafella offers a range of co-working spaces and serviced offices.

-

InstaOffice: InstaOffice offers flexible office spaces and co-working solutions across multiple cities, with a focus on creating productive work environments.

-

GoodWorks Coworking: Based in Bangalore, GoodWorks offers co-working spaces with a focus on the tech community, particularly in the IT and startup sectors.

-

IndiQube: IndiQube provides customizable workspace solutions, catering to startups, SMEs, and large enterprises, with a significant presence in Bangalore and other cities.

-

BHIVE: BHIVE is a co-working space provider based in Bangalore, focusing on creating a vibrant community for startups and entrepreneurs.

These competitors vary in their focus, ranging from startups and SMEs to larger enterprises, and they offer different types of workspace solutions, from traditional co-working spaces to managed offices.

DCB Bank – Steady performer (13-08-2024)

You are correct, sir. I also see potential here, but I want to understand more about how this bank operates. My concern is that, based on my assessment, they seem less aggressive. How will growth come in the future if they maintain this approach?

Panasonic Energy India Company Ltd (13-08-2024)

Exciting set of Q1 results.

Points that reaffirm/further the thesis:

- Revenue up 7% YoY adjusting for the B2B order.

From Eveready’s call according to Neilsen:

The segment of carbon-free

batteries, which still constitutes nearly 90% of the battery market by value, remained

muted during the quarter, primarily due to weak rural demand, and our performance

was in line with the market.

This implies yet another quarter of market share gains for Panasonic. During 4Q24, they had outlined ambitions to increase market share by 2 percentage points every year. They seem to be exceeding their own expectations last year and this year till date.

- Gross margins up sharply.

Gross margins up approx 500bps for the industry. Not sure what part of the remaining increase can be attributed to the lower base from B2B customers and what part to increased realisation over and above the industry. - EBITDA margins up to 8.5% vs 4.8% in 1Q24.

Trending closer to Eveready’s margins as per thesis. - Continue the renewed focus on shareholder value

Dividend resumed, at 8.85 per share vs 7.5 per share in FY22

Employee costs have increased by around 20% YoY. Looks like the restructuring phase is over and they have resumed our growth phase. Given the widely anticipated rural market recovery in the upcoming quarters driven by strong rains and hopes for populist policies in our country in the coming years, I’m excited to see the growth they’ll be able to provide given that they’ve done strong numbers in such a weak environment in the recent quarters.

Minor reflections/rant(not analysis):

I continue to be confused by the strong performance by Eveready’s stock price despite continued muted performance and the valuation discrepancy with Panasonic.

The market seems not to appreciate that even in developed markets, revenues continue to grow single digits(according to Eveready’s claims in the latest concalls) and that batteries are proxy plays to several attractive bets on skyrocketing discretionary spends when percapita income grows beyond $2000.

eg. FirstCry listed at a very strong premium to the IPO price and saw good demand on listing. Given that toys are a great percapita play cited above, why does the market not seem to reward a strong brand like Panasonic with valuations similar to or better than a company like Eveready which has not only struggled to grow in batteries but also scale profitably in other categories such as lighting and flashlights.

FYI, only Duracell and Panasonic have their batteries being sold on FirstCry.