Posts in category Value Pickr

Piccadily Agro Industries Ltd (13-08-2024)

(post deleted by author)

Piccadily Agro Industries Ltd (13-08-2024)

It is very difficult to find out what is happening in the company.

Investors have no idea how many casks company have? How many of them are maturing this year? How long is the maturation period – Is it 3 years or 5 years or 7 years?

Also, how much malt is for captive use and how much is company selling? Is company selling matured malt or fresh malt? If it is matured malt, how is it matured?

I have realised the 30k litre/day capacity management was talking about in the interview was malt capacity and similarly 60k litre/day capacity in fy26 is also malt capacity.

No one has an idea about the Indri whiskey or other whiskey capacity. The company is a total back box, no one can see inside.

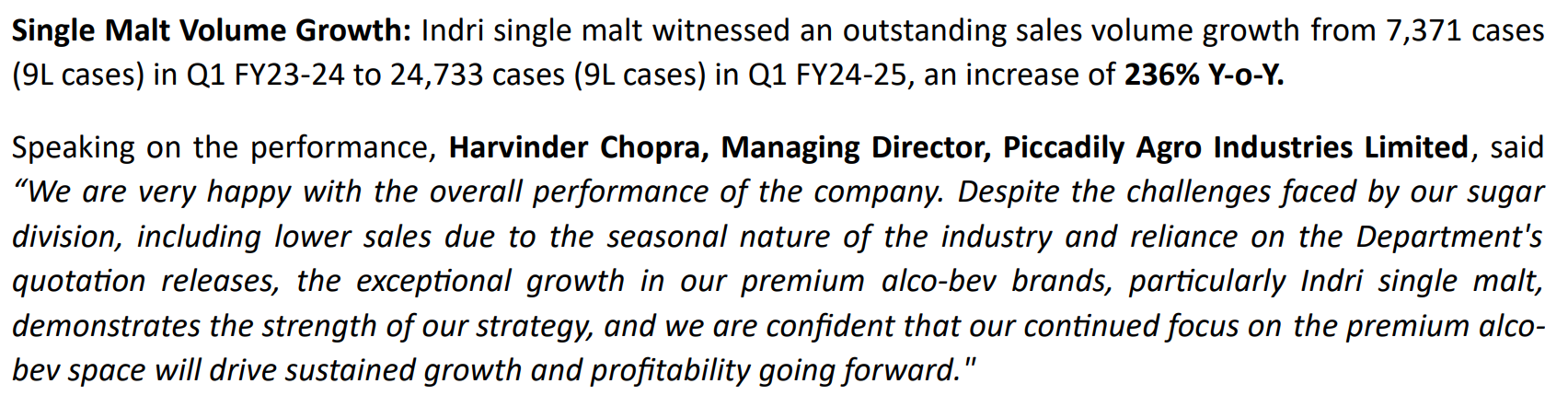

Now the distillery revenue has increased from 106cr to 119cr an increase of 12% but Indri whiskey sale has gone from 7,371 cases to 24,733 cases. Assuming Rs. 3000/bottle price revenue from Indri last year was 27cr whereas this year it is 89cr.

so, what happened to the sale of other brands – Golden wings, Whistler Whiskey, Kamet Single malt, Camikara rum & Royal highland.

Kamat Hotels (India) Ltd- A Possible Turnaround Story! (13-08-2024)

I have been tracking this company for past 2-3 quarters. After every quarter, I see people on the forum discussing the promises the management has not kept. And I get the feeling that the management breaks more promises than they keep.

Market has many other opportunities. In such a scenario, it is better to deploy your hard earned money in a company where you can trust the management’s guidance than go bottom fishing.

Cheap stocks are cheap for a reason, especially in these bull markets

Zuari Industries (13-08-2024)

Please read forum guidelines properly before initiating a thread.

https://forum.valuepickr.com/faq

To nurture a vibrant community ValuePickr does not restrict anyone from starting a thread on a stock of his/her choice. Only Caveat is if you are going to introduce a discussion on a stock, we expect you to do your homework and start the thread with some basic info-set, and 1st level analysis such as growth drivers, a few positives & negatives, immediate triggers if any, and enumerate some RISKS. Nothing very heavy is required, but enough to set the tone for 2nd level of discussions.

Thread initiators are usually alerted to edit their post, and make necessary changes before thread is opened up again. So you/colleague and look to edit the post in order to meet prescribed guidelines. We have the responsibility – especially the thread initiator (assumption is he/she is a savvy investor) – to cater to bringing everyone on same page – quickly – if you know what we mean.

Kamat Hotels (India) Ltd- A Possible Turnaround Story! (13-08-2024)

No, didn’t specify anything

This is possible but will be skewed towards the year end.

They could have easily postponed it.

Insecticides India A stock with good Opportunity size (13-08-2024)

Insecticides India –

Q1 FY 25 results and concall highlights –

Revenues – 657 vs 640 cr, up 3 pc ( volume growth was 15 pc, lower topline growth is due to fall in RM and end product prices )

Gross Margins @ 27 vs 21 pc YoY ( pure generic products have a GM of around 15 pc )

EBITDA – 72 vs 46 cr, up 57 pc ( margins @ 11 vs 7 pc – massive improvement YoY )

PAT – 49 vs 29 cr, up 68 pc

Product wise sales breakup –

Insecticides – 33 pc

Herbicides – 61 pc ( doing very well vs LY )

Fungicides – 4 pc

PGRs – 2 pc

Channel wise sales breakup –

B2C – 71 pc ( vs 66 pc LY – good improvement )

B2B – 26 pc

Exports – 3 pc

In B2C category, 60 pc of sales in Q1 FY 25 came from premium products vs 57 pc LY vs 51 pc in FY 23 ( company calls them Maharatna and Focus Maharatna products ). These r higher margin products vs pure generics. At the company level, they contributed to 42 pc of sales. Gross margins in these products are > 40 pc vs around 15 pc for pure vanilla generics

The monsoon distribution has been good this season + the reservoir levels are healthy. This makes the Industry outlook positive

Company is working with Nissan Chemicals on half a dozen products ( these tech – transferred products obviously have higher margins )

Products launched after 2020 are already contributing to > 500 cr on the topline ( this is a very encouraging sign )

Q2 looks promising across India. Should exit the FY25 with double digit EBITDA margins

For most of the new products that the company is launching, AIs ( or technicals ) for them are made In-House

At present, company has 11 Focus Maharana products. These r high growth, high margin products ( mostly with Pan India presence ). Aim is to keep graduating more products from Maharatna to Focus Maharatna category. Maharatna products are currently smaller with regional presence

Pricing pressures continue to remain in B2B and Exports mkt. Reversal of this scenario may take some more time

Will be launching 04-05 new products this FY. All these will be differentiated products in the Maharatna category

Company is guiding for volume growth of > 15 pc with a value growth of around 10 pc for FY 25 ( due price corrections in finished products ). Should be able to do an EBITDA of around 220 cr for FY 25

Company’s new Technicals facility at Dahej is expected to start production in 1-2 months time ( awaiting Govt approval ). Company has spent around 150 cr on this plant. This plant has a revenue potential of around 250 cr ( realisable from next FY ). However, if the company chooses to use this plant for captive consumption to lower the costs of its formulations, this revenue potential may come down but the company level margins may increase

Company intends to keep improving the contribution of Maharatna + Focus Maharatna products in its overall revenue pie for the foreseeable future. Hence, there should be continuous margin improvement going fwd – in the medium term

Disc: holding from lower levels, biased, not SEBI registered, not a buy / sell recommendation

Ranvir’s Portfolio (13-08-2024)

Insecticides India –

Q1 FY 25 results and concall highlights –

Revenues – 657 vs 640 cr, up 3 pc ( volume growth was 15 pc, lower topline growth is due to fall in RM and end product prices )

Gross Margins @ 27 vs 21 pc YoY ( pure generic products have a GM of around 15 pc )

EBITDA – 72 vs 46 cr, up 57 pc ( margins @ 11 vs 7 pc – massive improvement YoY )

PAT – 49 vs 29 cr, up 68 pc

Product wise sales breakup –

Insecticides – 33 pc

Herbicides – 61 pc ( doing very well vs LY )

Fungicides – 4 pc

PGRs – 2 pc

Channel wise sales breakup –

B2C – 71 pc ( vs 66 pc LY – good improvement )

B2B – 26 pc

Exports – 3 pc

In B2C category, 60 pc of sales in Q1 FY 25 came from premium products vs 57 pc LY vs 51 pc in FY 23 ( company calls them Maharatna and Focus Maharatna products ). These r higher margin products vs pure generics. At the company level, they contributed to 42 pc of sales. Gross margins in these products are > 40 pc vs around 15 pc for pure vanilla generics

The monsoon distribution has been good this season + the reservoir levels are healthy. This makes the Industry outlook positive

Company is working with Nissan Chemicals on half a dozen products ( these tech – transferred products obviously have higher margins )

Products launched after 2020 are already contributing to > 500 cr on the topline ( this is a very encouraging sign )

Q2 looks promising across India. Should exit the FY25 with double digit EBITDA margins

For most of the new products that the company is launching, AIs ( or technicals ) for them are made In-House

At present, company has 11 Focus Maharana products. These r high growth, high margin products ( mostly with Pan India presence ). Aim is to keep graduating more products from Maharatna to Focus Maharatna category. Maharatna products are currently smaller with regional presence

Pricing pressures continue to remain in B2B and Exports mkt. Reversal of this scenario may take some more time

Will be launching 04-05 new products this FY. All these will be differentiated products in the Maharatna category

Company is guiding for volume growth of > 15 pc with a value growth of around 10 pc for FY 25 ( due price corrections in finished products ). Should be able to do an EBITDA of around 220 cr for FY 25

Company’s new Technicals facility at Dahej is expected to start production in 1-2 months time ( awaiting Govt approval ). Company has spent around 150 cr on this plant. This plant has a revenue potential of around 250 cr ( realisable from next FY ). However, if the company chooses to use this plant for captive consumption to lower the costs of its formulations, this revenue potential may come down but the company level margins may increase

Company intends to keep improving the contribution of Maharatna + Focus Maharatna products in its overall revenue pie for the foreseeable future. Hence, there should be continuous margin improvement going fwd – in the medium term

Disc: holding from lower levels, biased, not SEBI registered, not a buy / sell recommendation

Xpro India – getting bigger? (13-08-2024)

I am not ascribing any value to this segment. If they r able to break even and not be a drag on the di-electric segment, that’s enough for me ![]()

![]()