Significance lies in the repetition of the order and not the value.

Posts in category Value Pickr

Rajesh’s portfolio (12-08-2024)

Result is below expectations and management explained the reason. This will unfold fully by Q4 when their capacity is built fully.

Addictive Learning Technology limited (LAWSIKHO) (12-08-2024)

Management to meet on 19th aug to consider Fund raising.

Interesting deviation. Acquisition on the cards? As far as I understand, they don’t really need additional funds to expand the current business

Tilaknagar Industries- Potential Turnaround Candidate (12-08-2024)

Key highlights of Q1FY25 results. Excellent result inspite of disruption due to elections.

Financial performance:

![]() Achieved HIGHEST ever Q1 EBITDA at Rs. 50.2crs, 30.8% YoY

Achieved HIGHEST ever Q1 EBITDA at Rs. 50.2crs, 30.8% YoY ![]()

![]() EBITDA margin at 16%, 341 bps expansion YoY

EBITDA margin at 16%, 341 bps expansion YoY

![]() Profit after tax at Rs. 40.1 crs; YoY growth of 55.7%

Profit after tax at Rs. 40.1 crs; YoY growth of 55.7%

![]() Gross debt reduction of Rs.22.3 crs in the Qtr, net debt at Rs.42.6 crs

Gross debt reduction of Rs.22.3 crs in the Qtr, net debt at Rs.42.6 crs

Market share and leadership position:

![]() Increasing share of premium products visible in EBITA margin

Increasing share of premium products visible in EBITA margin

![]() Continue to be the largest IMFL player in Puducherry in Q1FY25

Continue to be the largest IMFL player in Puducherry in Q1FY25

![]() Launch of Green Apple Flandy in Telangana and Andhra Pradesh.

Launch of Green Apple Flandy in Telangana and Andhra Pradesh.

![]() Within first quarter of launch, achieved 20% share of Flandy volumes.

Within first quarter of launch, achieved 20% share of Flandy volumes.

![]() Expects favourable excise policy in Andhra Pradesh & Telangana

Expects favourable excise policy in Andhra Pradesh & Telangana

NewJaisa Technologies: A D2C Refurbished Electronics Play (12-08-2024)

3 inputs:

- If one just googles ‘used laptops’, this company does not appear in search ( cashify,amazon,olx happen to be there)

- Apart from online competition, these guys are competing with small computer shops across the country. Advantage with small shops is that you’ve a face behind the sale. This also helps in faster repair if you find a problem with the product you purchased.

- Only path to survival and growth for this compay is to create a big brand (needs huge money) as well as to have offline stores ( but it would depend upon the TAM)

Great articles to read on the web (12-08-2024)

Well explained all in one session on PE, PEG, Valuation. Must for new to market investors, others also will appreciate this.

Macfos Limited- A niche E-commerce Company (12-08-2024)

Are you spokesperson or “related parties” to the company?

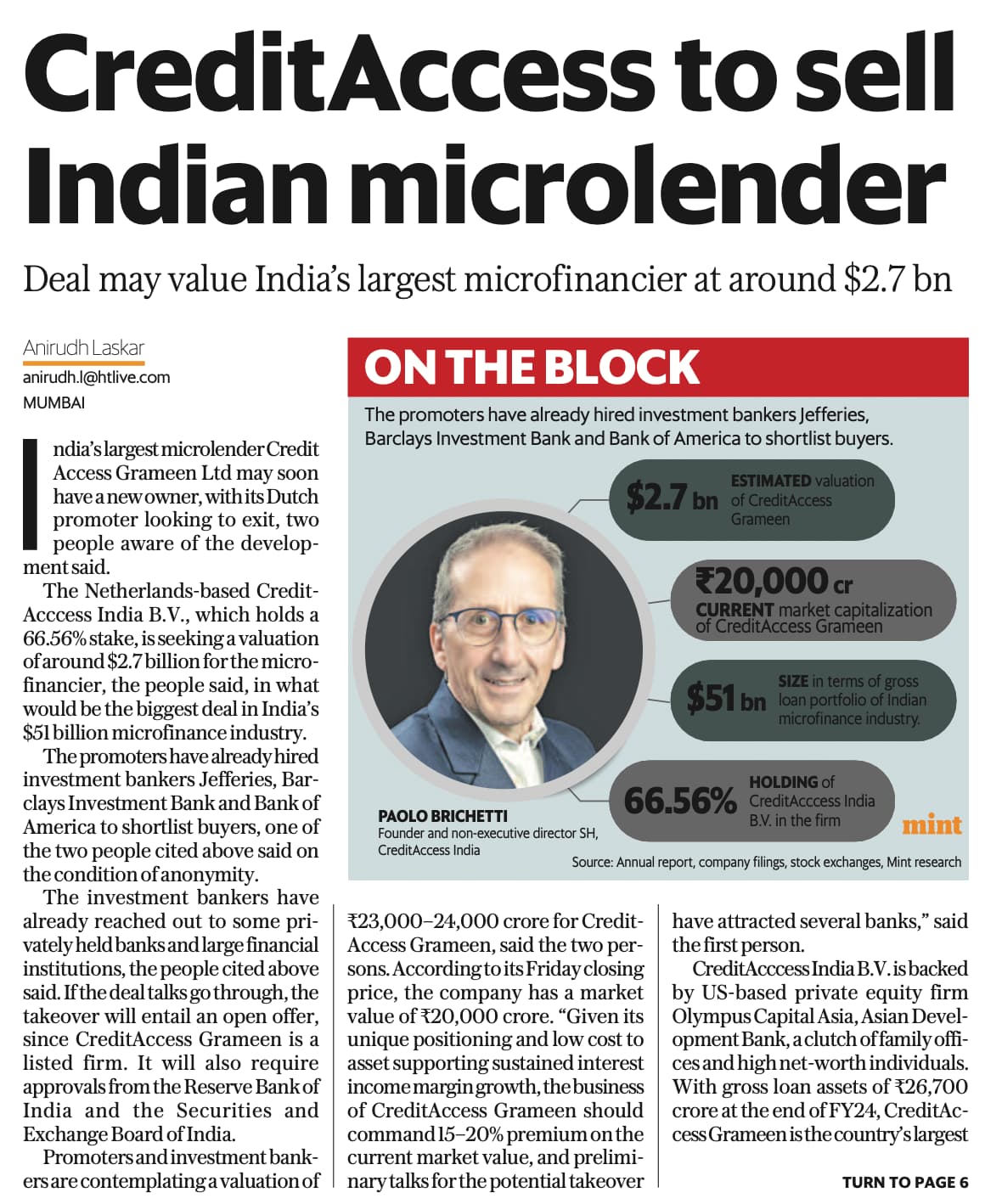

CreditAccess Grameen: Traditional MFI model, efficiently operating at scale (12-08-2024)

Today there was an article on Livemint paper, about the promoters looking to exit.

PS: Admin, if this violates any regulations/rules of share, please delete it.

Saregama India Ltd: India’s premier music publishing label (12-08-2024)

Q1_2025 concall takeaway (Source: Screener note)

Financial Performance:

- Q1 FY25 operating revenue stood at ₹205 crores, representing a 26% year-on-year increase.

- Profit Before Tax (PBT) was reported at ₹51 crores.

- EBITDA increased by 9%, maintaining 33% of revenue, aligning with guidance for adjusted EBITDA.

Music Segment Insights:

- Music segment revenue showed a decline primarily due to the scaling down of Carvaan.

- Management reassured that music revenue, combining music and artist management, is on track for 25%-26% growth in FY25.

- Major releases included “Tauba Tauba” from “Bad Newz,” which topped multiple charts, including global YouTube and Spotify.

- A total of 330+ original and premium recreation songs were released across various languages.

- Upcoming releases include music from high-profile films such as “Stree 2,” “Jigra,” and more.

Artist Management:

- Over 150 influencers and music artists are now part of the portfolio, collectively boasting over 100 million followers.

- Artist management is expected to contribute significantly to revenue, with a target of 25%-30% growth in new music releases over the next 3-3.5 years.

Content Investment Strategy:

- The company is in a transitional phase, increasing content investment by 48% year-on-year.

- Long-term strategy includes investing over ₹1,000 crores in new music content over the next 3 years.

- Emphasis on a 5-year payback period for content investments, with the expectation of significant long-term returns.

Video and Event Segments:

- The video vertical is expected to grow at a CAGR of 25% over the next 5 years, driven by increased smartphone ownership and affordable data.

- The events business, while low margin, is projected to yield high Internal Rate of Return (IRR) due to short capital lock-in periods.

- Notable events include the successful “Dil Luminati” tour in North America.

Carvaan Strategy:

- Revised retail strategy focuses on e-commerce and modern trade, leading to a significant drop in Carvaan revenue to ₹24.7 crores compared to Q1 FY24.

- The management expects improved profitability margins as costs associated with physical distribution are reduced.

Industry Trends and Challenges:

- Transition from free streaming to paid subscriptions is anticipated to enhance revenue realization.

- The management believes that piracy is declining in major cities, with a significant portion of users likely to migrate to paid platforms.

- Management remains optimistic about the future, projecting a consolidated revenue CAGR of 30% and doubling PBT over the next 3-4 years.

Guidance and Outlook:

- The management maintains a guidance of 32%-33% adjusted EBITDA and a minimum of 26% growth in music revenue for FY25.

- Confidence in achieving long-term growth while maintaining profitability, despite initial investments in new content.

Disc :Invested

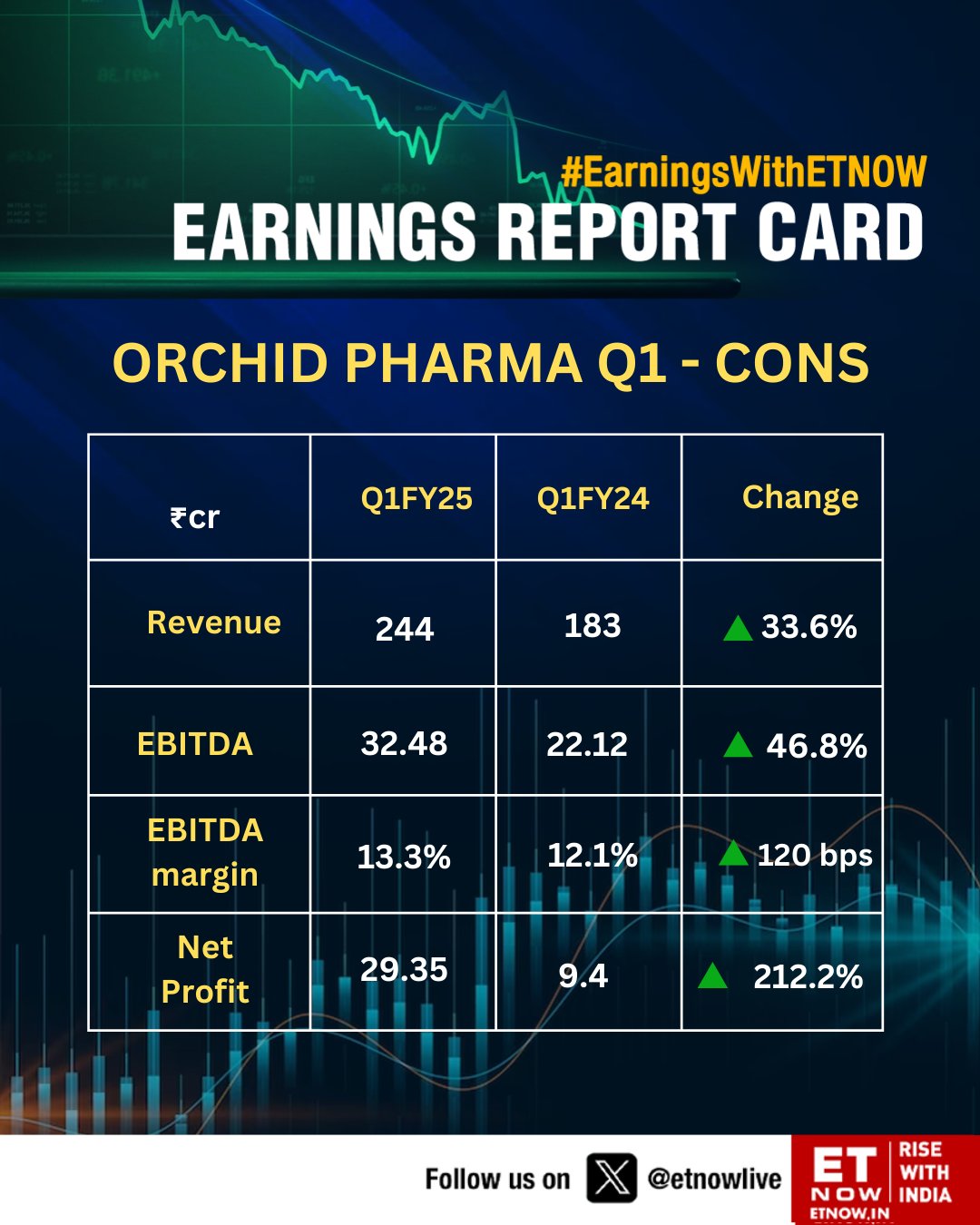

Orchid Pharma Ltd (12-08-2024)

Results Q1