Regarding Blue Pebble, agree with MOATs mentioned in the article

For Anti-thesis pointers, would like to add attrition risk in the design team. They have a fantastic team, but such team can be easily poached in the industry by competitors.

Regarding Blue Pebble, agree with MOATs mentioned in the article

For Anti-thesis pointers, would like to add attrition risk in the design team. They have a fantastic team, but such team can be easily poached in the industry by competitors.

This was a great read Anshul.

Went through other articles in your blog as well- must say you ve shared some great ideas there!

Stable topline, however bottomline improved substantially…

65f7b14a-9328-410a-8398-ed788d1fd2aa.pdf (1004.5 KB)

not right to compare on the basis of YOY as the base was too low , I believe in Q1 quarter constructions are in full swing, however some of it may have delayed due to elections (management may say the same in concall). But I believe, it won’t be easy to grow multifold revenue for the company on this base. 15% to 20% revenue growth in a low margin business, so the current valuations are justified or may be stretched.

X- @amitsinghpal

I was afraid of fusion like results, over the past few days.

Due to election quarter.

But I think, results are fair.

Growth has tapered , but that’s in line with expections , management has stated in last concall only, they are expecting a subdued quarter due to elections.

Will know how market reacts to it,but I think results are more than fair, beating the expectations, if compared with peers.

Thanks for your view…

I have bought sw solar because of my higher conviction and good level to buy… future I will definitely diversified this with others stock too but currently I think sw solar gives me margin of sefty compare to other’s.

Creadit access Grameen maybe not perform good currently but in future I am sure when rate cut start it’s one of the best beneficiary of this…

Results are out.

129Cr revenues vs 112Cr last year. Around 15% up yoy. Pretty much no change qoq

27.4Cr PAT vs 15.8Cr last year. Around 73% up yoy. 12% up qoq.

PAT has increased by 3Cr qoq. There is a 3Cr increase in other income and around 2Cr lesser expenses this quarter.

OPM is declining qoq yoy…

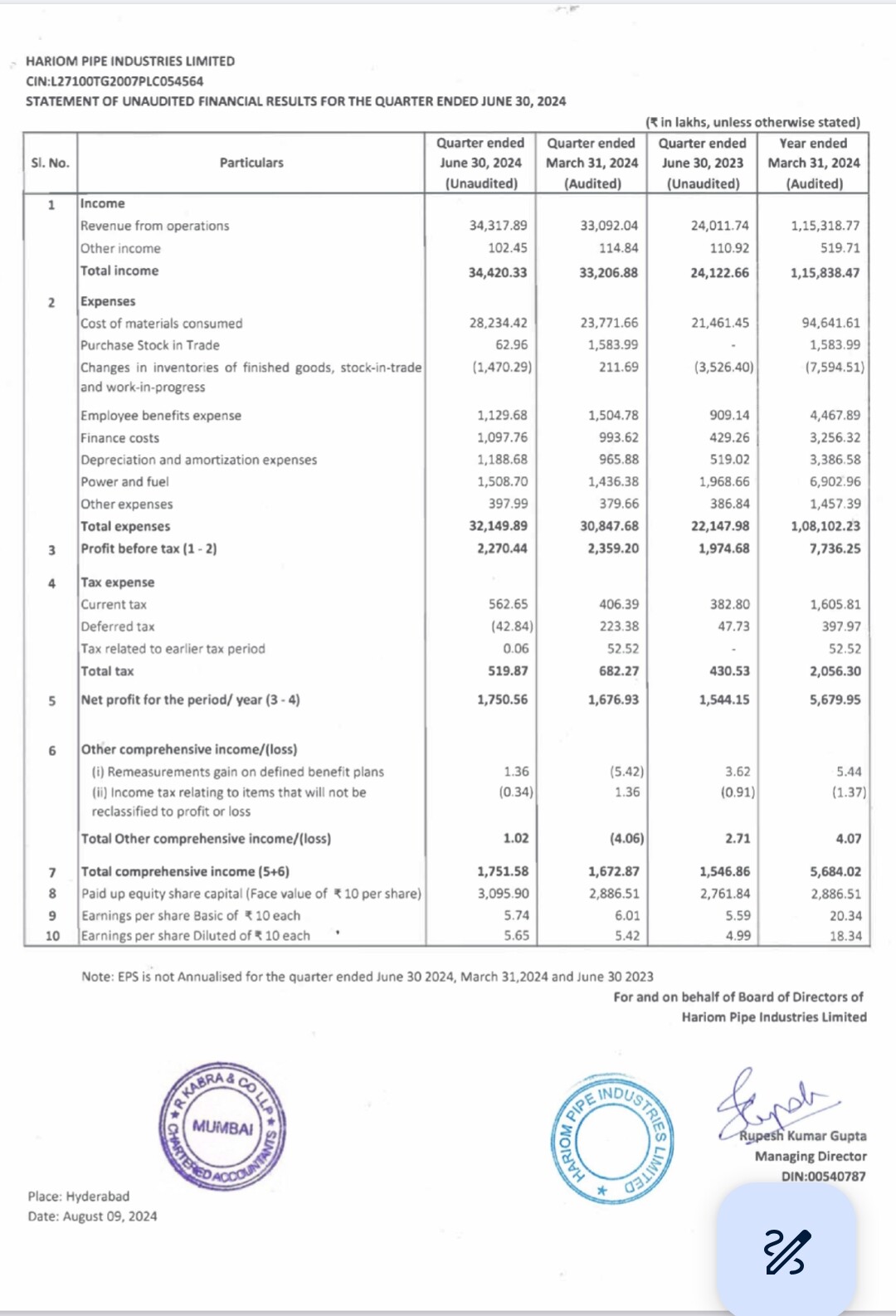

Hariom Pipe Results

Very Good Results beyond my expectations ![]()

Revenue up 43% YoY n Flat QoQ

EBITDA up 59% YoY n 6% QoQ

EBITDA margin at 13% vs 12% YoY n 12.6% QoQ

PAT up 13% YoY n 4% QoQ

Finance cost up

Operating Leverage now comes in Play (QoQ momentum started)

Overall very good set… Q1 is weak for sector and then too it has beaten Q4…

Might be Revenue expectations were high from market but Hariom has clearly beaten on Margin side

Now onwards Q1 < Q2 < Q3 < Q4

Based on guidance FY25 Revenue would be 1650-1750 Cr

Q1: 343 Cr

Left: 1300-1350 Cr

If Revenue would be around 375 Cr than it would be real beat… but still track this number whether they would able to achieve this or not

Debt free target till FY27

No Reco

Hi

They Cater to niche category and dont compete with general grade imported material whixh is available cheap in the market

They are working at a full capacity and looking to expand and hence they hold Cash in balance sheet

Also Companies in this field are all seeing great demand for their products

Disc – Invested at lower levels