Absolutely. Though management highlights every quarter that when Ugro started things were bad, then Covid came, after that now we are going great in our strength due to our business model, in all those times the management was in sideline watching. Now they have their foot in water, we will see how things work out. This now is going to be true test of management and business model.

But for us investors, I think this will help us to assess the company with AUM well under 10000 crores. Would have been much worse, had the tough times came later, like at AUM around 25000 crores.

Posts in category Value Pickr

Ugro Capital – Opportunity To Invest in a Fintech-like Company Below Book Value (09-08-2024)

Midhun’s Investment journey and Space to organize investment ideas (09-08-2024)

Sharing my portfolio update. Lots of new entrants post the last update. Overall portfolio size has grown at descent clip (Almost everyone would have the same experience).

Not very proud if the way the portfolio looks like. Need pruning of stocks since the portfolio looks like a potpourri of sorts. Will be happy to discuss on the investment thesis of any of the stocks further.

Bharti Airtel – What doesn’t kill you makes you stronger? (09-08-2024)

Bharti Airtel fined Rs. 258,000

The telecom giant has been slapped with a penalty by the Department of Telecommunications (DoT) for allegedly violating subscriber verification norms. The fine was imposed based on a CAF audit conducted for May 2024.

Godrej Properties – Brand, Business model & Scale (09-08-2024)

Godrej Properties secures prime land in Greater Noida:

The company has emerged as the top bidder for two land parcels in Greater Noida, with a combined bid value of Rs 842 crore. This acquisition will add ~3.75 million sq ft to its development pipeline and has the potential to generate over Rs 5,000 crore in revenue.

This move strengthens Godrej Properties’ presence in the NCR market.

Granules India Ltd (09-08-2024)

Granules India has received approval for its generic version of Trazodone tablets. This is a positive development as it expands Granules’ US market presence in the anti-depressant segment. Expect increased revenue and profitability from this product in the coming quarters.

Kilburn Engineering – Huge undervaluation (09-08-2024)

The company has secured new orders worth Rs. 1,903 lakhs, primarily for rotary and paddle dryers. This brings the total order intake for the year to a substantial Rs. 17,930 lakhs.

Cummins – Generating Power (09-08-2024)

Q1FY25 Concall Summary

Business Updates

Participants

Macquarie

HDFC Securities

PL Capital

LIC Mutual Fund

Axis Mutual Fund

Nomura

360 One Asset Management

Goldman Sachs

Birla Mutual Fund

Kotak Securities

QnA

- All segments of industrial business viz construction, mining, marine etc have done well during the quarter gone by and this is broadly correlated to infrastructure growth in the country which continues to do well

- There have been benefits of a better product mix with CPCB IV plus becoming a part of the product portfolio and with commodity prices easing off the gross margins have benefitted but this trend should not sustain and if commodity prices come up there could be a normalization of margins

- The export market seems to have bottomed out and that is why there was growth in exports in Q1 and the growth has come from Middle East and Africa while rest continues to remain flat

- Globally data centre contributes around 10% of the parent organization’s revenue and that is what is expected in the domestic market as well

- The domestic operations continue to aspire for growth of 12-14% and the parent entity guided lower because of global slowdowns and not looking at India market

- The channel inventory is zero and the inventory of CPCB II gensets is now over and the overall level of inventory within the system too is very low

- India was a power deficit market earlier, which has kept reducing gradually, but still the demand has continued to grow. As the country becomes affluent the non availability of power becomes a big deterrent as backup power becomes critical which is happening in India

- Construction is directly related to infrastructure where engines are supplied to all earth moving equipment’s and that is in a multi decade up cycle as it is needed in all aspects of infrastructure

- The railways business since it migrated from diesel to electric saw a business downturn but the company continues to work on the electrification side and there are orders from that segment now as well

- The channel inventory remains low and the order book continues to swell and now the expectation is that the demand is agnostic to the price hike that CPCB IV calls for

- From a 10 year window the growth opportunity looks good which will face challenges in short term due to product related transitions and that turbulence will cause short term challenges but overall situation looks better

- Historically the company has always been the weakest in the lower HP ranges because in the last two decades the lower HP segment has become a commoditized product and thus the company allowed competition to take a larger share of this segment

- CPCB IV Plus is a game changes because it forces the industry to turn towards a better technology product which is not a capability for every company and thus this transition should lead to a higher market share for Cummins

- The management feels the industry is at an inflection point and a high growth rate can sustain for many more years and if the economy grows to $10 trillion and more as envisaged the demand for power and power gen. equipment will be very high

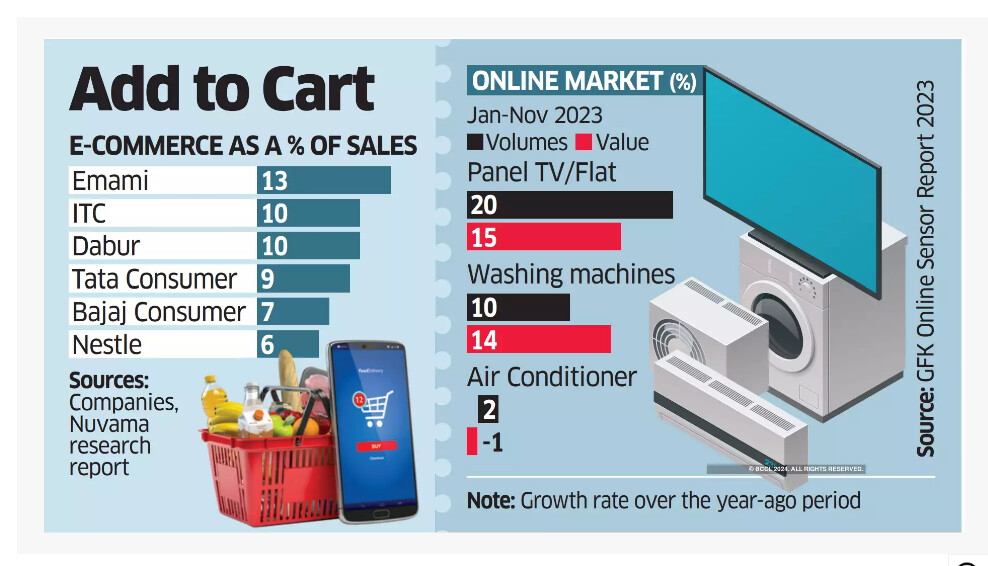

Zomato – Should you order? (09-08-2024)

its a clickbait

if you read the whole article it says:

E-commerce is about 7% of our overall sales, Q-commerce is one-sixth of that and continues to grow.

HUL is FMCG company and as of 2024 93% of its sales comes from offline stores according to the same article.

You can already see they are not able to sell a lot from quick commerce. If you still have doubt then keep track of dmart shares, modern trade is emerging as the biggest threat to these quick commerce companies and dmart is not giving rosy hopes, they are delivering hard profits, even reliance is not able to compete with dmart without pumping money from oil refinery business.

I personally believe in investing in companies with atleast having some profit, I will never invest in something which is based on story and making lots of losses. If you got crores in your pocket to tolerate the risk then you can bet on quick commerce.

For now I will end this discussion. I am not getting any convincing argument that tells me otherwise.

Garware Hi-tech films (Earlier Garware polyester) (09-08-2024)

Great numbers achieved by the company, especially the increase in Operating margins from 18% to 25 % is commendable.

Majority of the increase in revenue has come from SCF business this quarter, which is again a highly value added but seasonal business.

The IPD segment seems to have performed well on account of raw material prices.

However it is yet to see if margins at this level are sustainable.

AllCargo Logistics – Are good time ahead? (09-08-2024)

As I understand it, the value of AllCargo Logistics shares is likely to drop after the AllCargo ECU demerger. The Gati ↔ AllCargo Logistics swap will occur after this demerger, so everything hinges on the valuation of AllCargo ECU.