Decent results. Interest based revenues are increasing signifying higher loan book. Provisions have jumped but not as much as the marginal revenue change. Fees and subscriptions profits are flat. Revenues have dropped but so has expenses proportionally. Other expenses and depreciation has increased but could be onboarding costs, servers etc. Would like an explaination. This quarter hasn’t been a great one for nbfc and the likes so nice to see Apolly doing well. I would watch out for provisions not increasing further.

Posts in category Value Pickr

Voldemort’s Portfolio (10-11-2024)

Polymatech’s unlisted shares are down 50% is what I have seen.

I have flagged it earlier, will say it again – this company is vaporware.

Best to invest in the NVDA, TSMCs of the world.

E2E Networks Ltd – Listed small Cloud computing player (10-11-2024)

Speculating on the business direction, one possible pivot from a client targetting perspective could be E2E becoming a corporate client focussed company from the primarily startup focussed company it currently is. The L&T deal could lead to this important change, is what I feel.

Microcap momentum portfolio (10-11-2024)

@bindalpr007 As you are aware, Nifty 500 consists of Nifty 50, Next 50, Midcap 150 and Smallcap 250. I have separate pfs for all these universes.

In fact, I am sharing the pf for Midcap 150 and Smallcap 250 in this forum.

Voldemort’s Portfolio (10-11-2024)

Voldemort bro – You have reduced Jio and Infy, any particular reasons? I felt time for Jio Fin would be starting Q4 FY25 and beyond once various verticals start generating meaningful businesses and profitability, time to add more was/is now. Secondly, would you need some superstars like Hindcopper, Network18, Optiemus Infra, Ola, OYO types which have the potential to generate 3-4x in lesser timeframe than others?

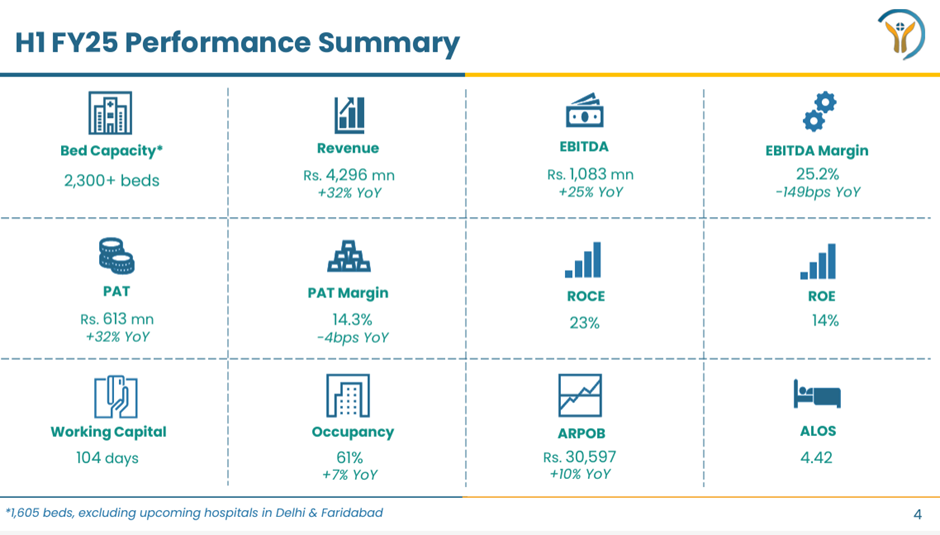

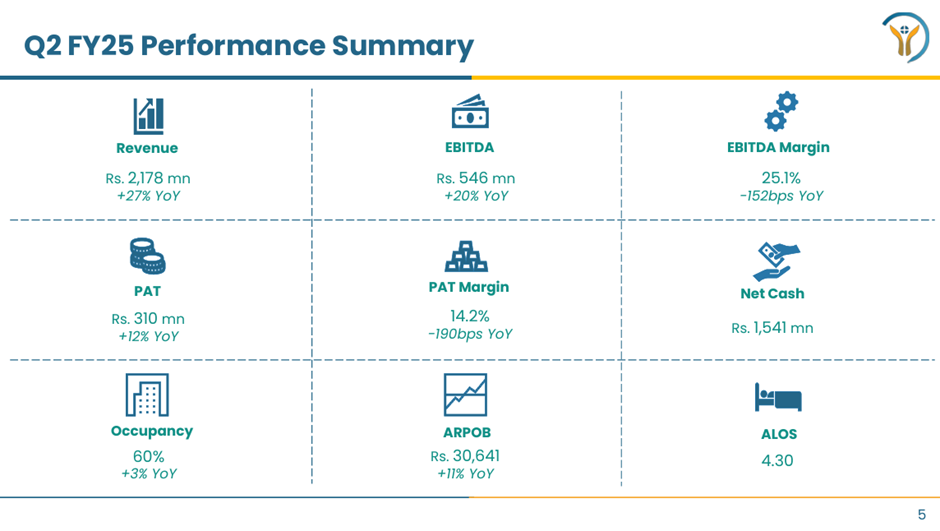

Yatharth Hospital & Trauma Care Services Limited (10-11-2024)

Q2 FY 2025 CONCALL HIGHILGHTS

Yatharth attracting leading doctors across NCR.

Deloitte is appointed as internal auditor.

Rise in employee cost due to new therapeutic areas, new doctors joining. Margins will be sustainable (25 to 26% at group level) with two more additional new hospitals. Mature Hospital margins is 28 to 29%.

Dropping occupancy in Noida hospitals due to reduction on government business. It is reduced by 1 to 2%. IPD volume increase. Focus on increasing cash and insurance segment. It will have positive impact in coming quarters.

EBIDTA loss in Faridabad Hospital, started in Q2 FY2025 is 28% Negative and reducing.

Planned CAPEX is from Internal accruals, 60 to 70 L per bed for expansion of beds in existing hospitals.

Decline in Jhansi ARPOB due to reduction in cash payments. Government panel drags in margin. It will be 15000 to 20000.

Max Hospital opened near Yatharth Hospital will build ecosystem in Noida, should benefit every operator. Continuous improving standards.

No difference between Q1 and Q2 Revenues due to no breakout of flu in areas of operation for Yatharth. Government business is reduced as per strategy by company.

Government business is reduced by 4% Q to Q, 6% H1 to H1. Target is to reduced government business to 25% in 3 years.

To fill available capacity government business is taken.

Expect Q3 and Q4 will be higher. Expect near to 1000cr. Revenue.

New Hospital in Model Town:

160cr. Will be paid to Union Bank. 25% paid by company’s book.

Additional 60 to 70 cr. For improving infrastructure and medical equipment. With this It will be 300 beds.

ARPOB in this hospital will be more than Noida hospital, will be super specialty in day one. It can be close to 40000 ARPOB easily achievable.

Existing capacity is 150 to 170 beds.

Hospital currently non-operational. It was operated by family of doctors. Face financial issue and bank take over. It was acquired by online auction.

Land, structure belong to Yatharth. No Rent.

Pay back period will be 3 to 3.5 years.

New Hospital in Faridabad:

Keep on investing on 60/40 % basis.

Minority shareholder is family from MGA. They do not operate any other hospital. One of the son is cardiologist.

Additional 90 cr will be spend to complete structure and medical equipment including Radiology.

Land, structure belong to Yatharth. No Rent.

Reason of adding one more hospital in Faridabad as they will be 15 to 20 km distance. Model of big player in city, which gives benefit of brand position, star doctors can be shared between two hospitals. Doctors wants to join as head of department as capacity will be 600 beds. Near to Airports and have great drainage of population and have massive expansion.

Expected ARPOB in this hospital can be 38000 Rs. Can be with start of and can go beyond.

Conclusion:

Revenue can continue grow with sustainable margin of 25 to 26%.

Have more debt, dilution in equity as company continue to acquire more hospitals.

Valuation is attractive compared to peers.

Room for improvement in ARPOB compared to peers.

Disclosure: Invested, may exit anytime. Reviewing.

Ranvir’s Portfolio (10-11-2024)

I feel that having concentrated portfolios make it easy to track companies and one have develop much better understanding of a lesser number of companies.

The advise of concentrated portfolios needs to be pushed back – as there are realities and trade offs of the real world.

- Tradeoff between deploying new money – within in your portfolio whose valuations are good to hold but not to enter – versus adding a new stock which one likes. In a bull market this is very common situation. It may be better to add a new stock than sit on cash.

- What is the risk of ruin (losing a lot on high conviction bet) one can take – 3%, 5%, 10%, 15%. For each person this is different.

- Inability to differentiate between some bets. In that case why not make an index of 2-3 stocks than pick one of them.

- Should one count the stocks which are on the way out of one’s portfolio?

Praveg Ltd: Play on Indian Tourism Industry! (10-11-2024)

As per company vision statement FY28:

FY24: Rooms 680

No of rooms sold: 62592

Rooms occupied days at current: 92 days

Total Revenue including other income: 94.55 Cr

Per Room Tariff (2 days): Rs 15105/- , Average room per night : Rs 7500/-

Now apply to same math’s on FY28 (Refer slide 41 of Q1 presentation)

Estimated room sold 2500 X 92 days = 230,000

Assume no change on room tariff / without inflation adjustment = 15000/-

Total Revenue = Rs 345 Cr

PAT @ 15% = Rs 51.75 Cr

PAT @ 25 % = Rs 86.25 Cr

EPS @ PAT 15% = 51.75 / 2.58Cr shares = 20.04/- (Base case)

EPS @ PAT 25% = 51.75 / 2.58Cr shares = 33.40/- (Bull case)

Wait and watch Q2 result and management commentary on business!!

Solara Active Pharma Sciences – Pure Play API (10-11-2024)

Solara’s strategic reset is going to plan.

First clear trigger is lowering debt. At the start of FY25 they were at 3x Net Debt/EBITDA and so far they’ve reduced it to 2.5x. This is from the proceeds of the rights issue that management has also subscribed to. Arun Kumar (promoter) is leading the company now and so management is taking an active role in operations and financials. If Net Debt comes to 1-1.5x and pledges are released itself will lead to a big rerating.

Now coming to growth: FY25 guidance is 1400-1500 crores sales. 230-260 crores ebitda. Q4 ebitda guided at 80 crores. H2 expected to be better than H1. Even on a low base in FY24, FY25 will post decent growth. Vizag plant is being retrofitted to make it fungible. No revenues are coming from there right now. Vizag should come online in Q1FY26 and should have 3 quarters of operations next year. Vizag plant will be fungible so there will limited Ibuprofen production there. It will be used for higher margin polymers custom synthesis contracts. So next few FYs might bring both top line and bottom line growth due to changing product mix + operating leverage. Management said they would guide for next year in Q4.

It’s still trading at 2.6x book value and 2.7x sales so still quite affordable. Debt related rerating and growth due to product mix + op leverage are the triggers.

Disc: invested

Buy Unlisted Shares (10-11-2024)

Thank you Rajpanda Ji, i was caught up in two minds only because of this dilemma. Numbers wise, i expect a significant fall in volumes, revenues and PAT starting Q3, FY25 itself and more visible starting Q4 FY25. With IPO some time away, IPO valuations might get impacted in the short term. Needless to mention IPO price and listing price could be significantly different since owning is an aspiration for many. Larger point was about, raking in the profits and either pre or post listing, on bad days accumulate lower, time will tell if that happens or not.