are the prices given on this site correct?

Posts in category Value Pickr

Arman Financial Services Ltd (01-08-2024)

So just had a peak at this co, looks impressive considering other banks/nbfcs in MFI category majorly faced a lot of headwinds with declining profits YoY for Q1FY25. And the recent fall in the stock price does it make this co. undervalued and good to invest for long term has anyone researched it in-depth/is tracking. My apologies for asking straight away but I’m still trying to understand banking/nbfc sector

Wonderla Holidays (01-08-2024)

Q1FY25 Concall Summary

Business Updates

- The growth was lower due to external factors and footfalls were affected by heat wave, elections and water shortages

- There has also been a decline in discretionary spending

- The fourth park at Bhubaneswar has commenced operations during the quarter

- The park in Chennai is expected to operationalize in Dec 2025

- The management is in talks with other states for new parks and board has given approval for a fund raise to setup capex for the new parks over the next 7-8 years

Participants

Ambit Capital

RK Bhojani & Associates

RSPN Ventures

DSP Mutual Fund

QnA

- The expectation for Bhubaneswar park is a footfall of 4.5 lakhs for the first year and expecting a double digit footfall growth post that for the initial years

- There are 2-3 projects already in the pipeline so would like to raise the capital first and it will be declared to exchange in due course of time once finalized

- Presently there are 4 operating parks and one under construction. The company is in talks with state governments for 5 other parks and thus the capital raise will be for this expansion over the next 7-8 years

- The revenue from Bhubaneswar in Q1 was Rs 9 crores and EBITDA in Q1 was around Rs 85 lakhs. This was operational for around 38 days

- The moat with the company is a combination of an amusement park and water park and the ride quality is better with lower cost of setup

- The focus will be to get the footfall back and could resort to discounting as well which will keep the ARPU in check and hence not much growth in this number should be expected

Tips Industries Limited – Ready to RACE ahead! (01-08-2024)

Excerpts from the concall.

- Guidance is conservative as always, ~30% though it might probably be elevated for FY25 looking at Q1 results.

- Count of songs released: in Q1, ~100. Target for FY25 is 300. This number was around 900 for FY24 and 700 for FY23.

- Content costs target for FY25 is 80Cr. This number was 55.6 in FY24 and 62.4 in FY23. Essentially back to 30% YoY (from FY23 number) in line with topline guidance.

Overall, yes, partially agree that there might some more room for peak valuations. There also appear to be enough avenues for growth in coming quarters to sustain the added content cost jump. My take is we might see time correction if this doesn’t align. That will allow earnings to catch up to valuations.

Disc: Not invested, tracking.

Greenply Industries (01-08-2024)

Q1FY25 Concall Summary

Business Updates

- In plywood business volume growth was around 8.6% yoy in Q1

- The net debt level is at Rs 431 crores which has reduced by around Rs 70 crores

Participants

Kotak

HDFC Securities

Yes Securities

Investec

Asian Market Securities

QnA

- The product mix in MDF was better in Q1 and that has led to better realisations and better profitability as well

- The focus on MDF too remains the same as in plywood is to sell more of value added products

- There was a price hike in June and looks like another price hike needs to be planned in the coming quarter as well

- Pricing power is also a function of how the industry operates and if other players too start hiking it will become easier to pass on cost pressures

- There has not been any additional incentive or discount given in Q1 compared to Q4 while a lot of players in industry have done the same

- Entire Q1 including the month of July most of the players in the industry have been cutting prices

- There has been delays in the Samet project due to delay in receipt of machinery and also not being able to hire enough sales team staff and expecting to start sales from 1st Sept. The plant is ready to produce but some key machinery is still held up

- The investment into value added products is an ongoing process and the idea is to add 1-2 new products in the value added segment every year

- Most of the material that is imported is rubber wood while what is manufactured in India is different. In the commercial/industrial grade the company is not even competing with the peers

- There is a good 30% of industry in plywood where an organized manufacturer would not want to operate because of the lower grade margins and the product grade

- The next large capex will happen only for MDF and for plywood the additional capex to give growth for a 2-3 year perspective is only Rs 100-120 crores

- The business under Samet looks to be very good and the revenue potential post completion of the capex over three phases is Rs 750 crores with EBITDA margins of 25%. However this will be a tough market as there are entrenched players in the industry

- The total investments in Samet over three phases will be Rs 250 crores

IDFC First Bank Limited (01-08-2024)

Your question in ps is a complex one. Will check with my analyst friends and revert in evening. They have put out a research on the bank so they would know. Thanks

Black Box Ltd. – Riding the data center wave (01-08-2024)

Makes sense. The existing thread didn’t show up yesterday despite searching for it a few times.

NPST – Technology Provider for UPI Tech (01-08-2024)

Here is their AR, which might be helpful to understand.[

SME_AR_24756_NPST_2023_2024_31072024233655[1].pdf (3.9 MB)

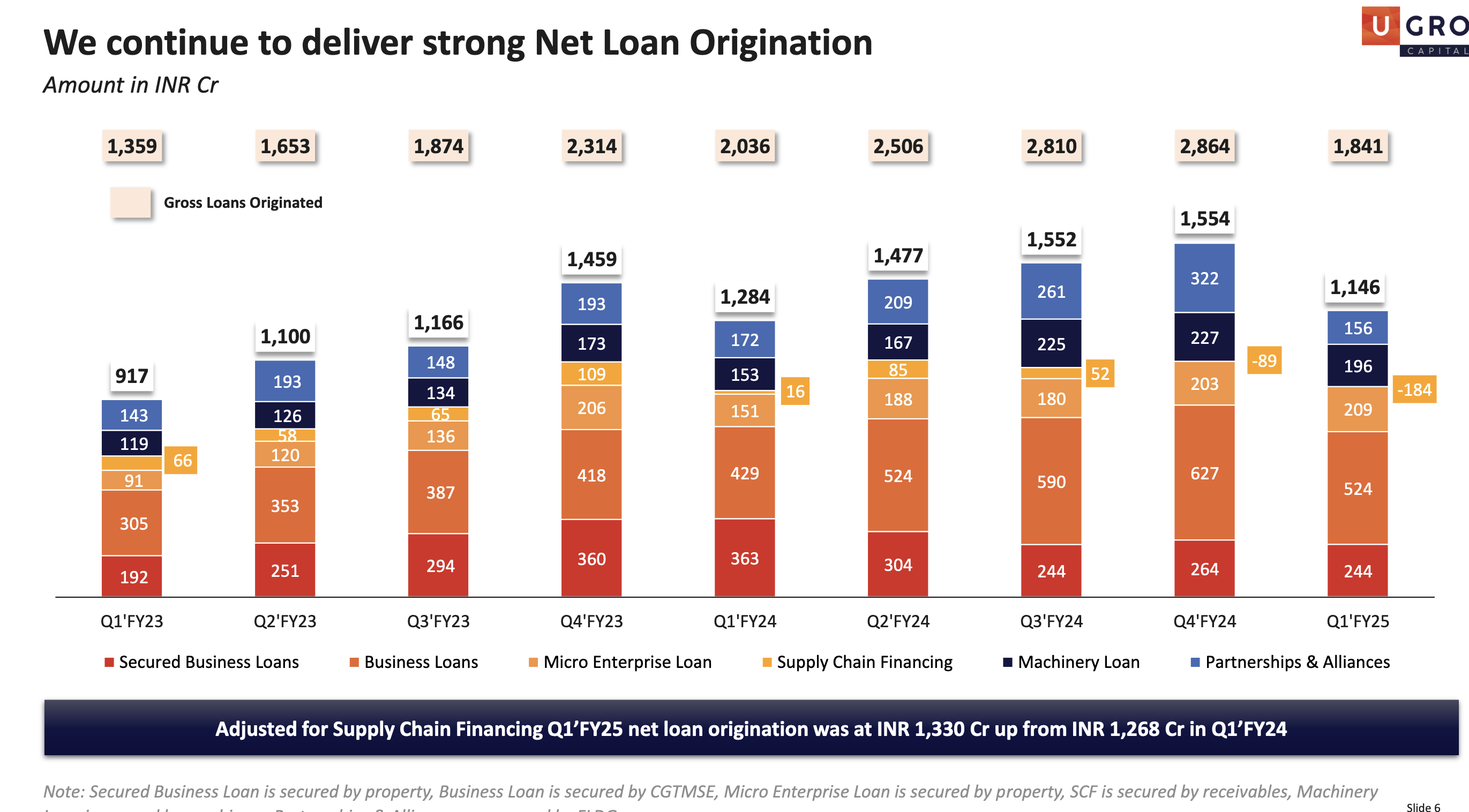

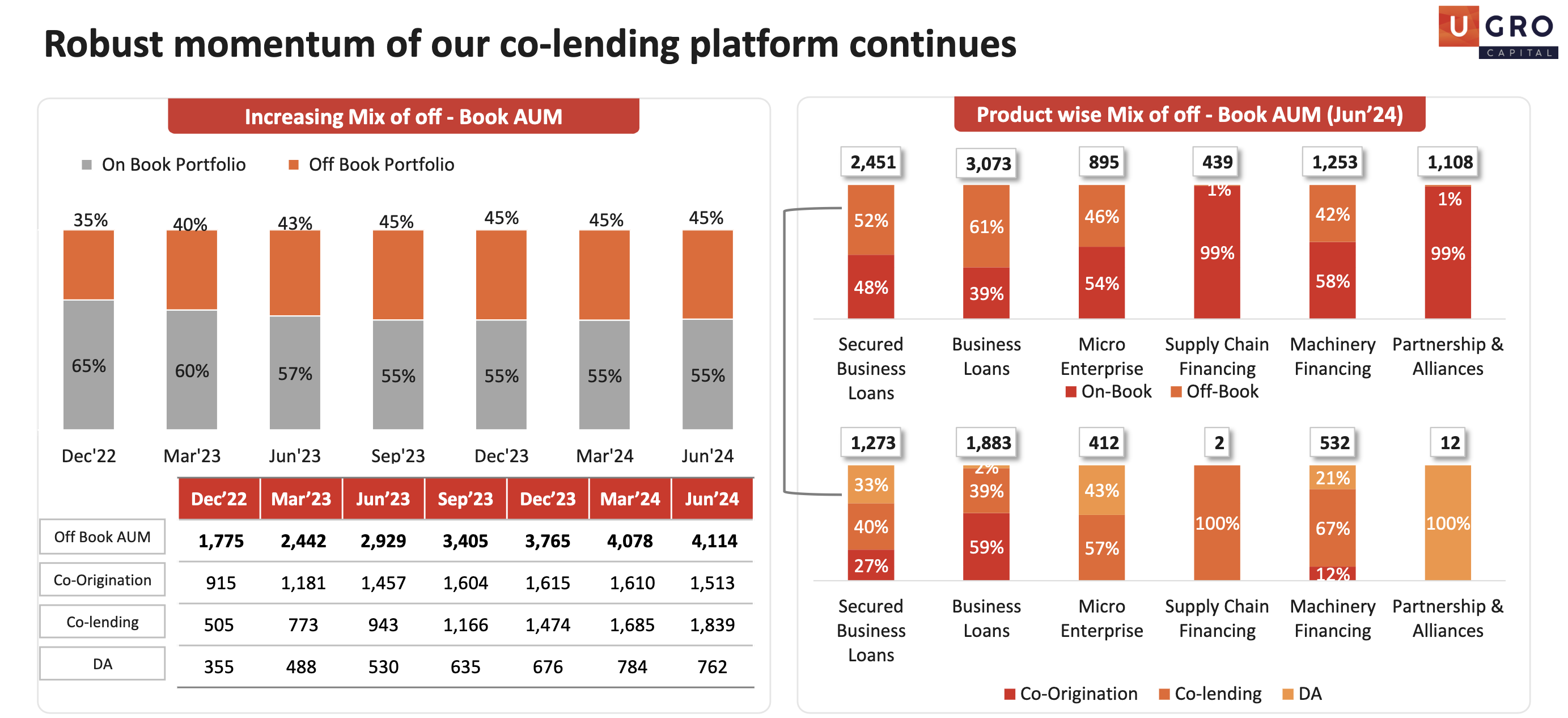

Ugro Capital – Opportunity To Invest in a Fintech-like Company Below Book Value (01-08-2024)

Few insights:

-

They are continuously increasing their co-lending book, got increased by 9% qoq. This is aligned with the long term objective of the management.

-

They are focusing on Secured and unsecured business loans for co-lending and using their balance sheet to ramp-up Micro enterprise loans. This way they will earn a good fees from banks for co-lending and high spreads from Micro enterprise loans. Good proposition for Ugro.

Question(refer the screenshot below):

-

What is co-origination, is it same as co-lending and why it got decreased?

-

Why over all net loan origination is muted in the quarter for all the buckets(only micro enterprise loan-book increased minimally), need some clarity here?