stride pharma q1 fy25.pdf (1.3 MB)

Company achieved ebidta of 217cr which is ahead of their FY25 outlook even though H1 is a leaner half.

One Source is ebidta positive for 2nd consecutive quarter and 2nd half of FY25 can have commercial supplies for GLPs.

Net debt reduced by 36.7 cr, currently 1998cr.

Posts in category Value Pickr

Strides Pharma/OneSource – The Last Stand Will Create Wealth? (29-07-2024)

Shaily Engineering Plastic (29-07-2024)

Notes from Q1 call

-

2 new FMCG products, 2 new pen injector contracts (1 lanreo and 1 sema), 2 components for automotive customer

-

Getting into Human Factors Engineering to cater to big pharma

-

1 pen injector purchase order for 10 million devices per year (own IP insulin pen) – context is 11.5 million pens done in FY24 and most were contract manufactured

-

Revenue growth will be much higher over the next 5 years

-

Tirze clinical batches will start end of year or next year (tooling and design work going on now)

-

Teri/Lira launches this year in regulated markets in EU/US. Sema in ’26 India/Brazil/Canada/China. Rest by 2029. Tirze 2030 RoW and 2036 in regulated

-

Every pen in the market except Novo’s FlexTouch and Shaily’s Neo are mechanical pens for Semaglutide and not spring driven – others have IP challenges

-

3 Exhibit batches (3 PQ batches) are supplied on each contract for pen injectors. Per batch is 10k so 30k total in PQ batches. For different strength, there are separate exhibit batches – so for sema, it could be 90-120k per customer. Then operational qualification, design verification, final assembly trials are extra

-

Of the 25 projects, most of Teri, Lira, Sema (Ozempic) exhibit batches have been supplied. Sema (Wegovy) is starting

-

Shaily UK will see above 35-40% growth in FY25. Pipeline is quite strong

-

Two new projects in Shaily UK for two new type of drug delivery devices – which aren’t yet generating revenue but under active development (Premium Reusable device, Nasal soft-mist inhaler)

-

Working with some consumer electronics companies – very early stages

-

Home furnishing 50 Cr, Pharma new applicator 35 Cr and Engineering plastics for GE around 40 Cr have started and on track in Q2 (no delays)

-

Home furnishing demand in plastics and carbon steel – no big growth expected but some growth will be there from new projects. Carbon steel there will be some growth

-

Q1 healthcare business had a lower growth because of a technical issue which has got resolved and supplies have resumed in Q2

-

CDMO fill/finish partner has no involvement in verifying design (limited knowhow in India). Shaily’s contracts are with pharma companies and verification happens there

-

Working on Monoclonal Antibodies using autoinjectors but its too soon.

-

18-24 months to capacity expansion. Currently at 40 million devices (some platforms might need expansion)

-

Ypsomed moving away from Insulin towards GLP-1 opening up the space. So several ongoing discussions underway and order pipeline is getting stronger. (The 10 million order could be a precursor for more such)

-

2-3 million pens in Lira possible by FY26/FY27 – could be more depending on launches and Customer’s success rates

-

70% of sema generic market can be captured by Shaily. Working with MNCs and small biotechs as well, alongside Indian generic players

-

Consumer electronics – will be working with HPP (High-performance Engineerig polymers) than ABS.

-

Shaily devices won’t infringe – $180k spent to conduct FTO (freedom-to-operate) to ensure same

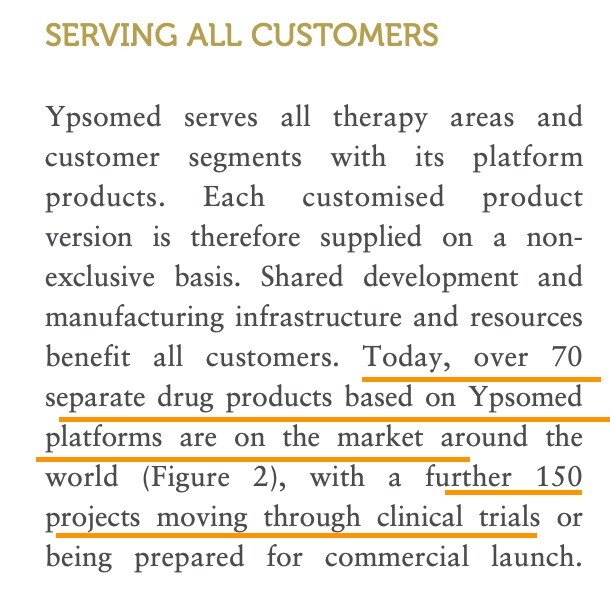

One of the informative pieces I came across from Ypsomed. Highlighting a few things I found interesting

The market is much beyond glp-1. Pretty much anything that’s a biological is a potential market and this market is growing. Some of the existing interferons, monoclonal antibodies are offered through pre-filled syringes (most generic humira launched last yr for eg.) and due to patient preference might migrate to auto-injectors as well. It is nice to know Shaily is working on auto-injectors for monoclonal antibodies as well.

Ypsomed has 220 projects (commerliased + pipeline) and shaily is today at 25 total. Shaily is picks and shovels player in the generic market which means a lot more projects for same molecule/therapy than a device maker that primarily works with innovators

Disc: Invested. Added in the last 30 days and likely to be biased

Waaree Renewables – old Sangam Advisors – can it keep on renewing? (29-07-2024)

Predicting stock prices is always uncertain, which is why the market exists since we will have differing opinions. However, I believe the Solar EPC sector is becoming increasingly crowded, with lower entry barriers allowing new players to enter regularly, driven by favorable conditions and government support. Ultimately, the market share will shrink, and valuations will stabilize. Most of re-rating is already done, now dust has to settle.

Between i just happen to open their website (never invested / researched waaree so far), looks like they are super busy for sure. Someone needs to move to 2024 ![]()

IDFC First Bank Limited (29-07-2024)

For F.Y. 2024,

Total Income – Interest Expended = 22,453 crores.

Now in Q1 this year, this number has grown by 25% YoY.

If they keep growing at same 25%,

This number will be around 43850 crores in F.Y. 2027.

With 65% Cost to Income PPOP can be around 15,350 crores.

And with 1.65% credit cost on this, after provisions and Tax, PAT can be in the range of 6500-7000 crores.

So 1.4% ROA in F.Y. 2027 is theocratically possible atleast.

Please rectify if you find anything wrong with these assumptions and calculation.

.

From 2015 to 2020 Bajaj Finance doubled PAT every 2 years,

Let’s hope that type of golden period begin for IDFC First 2025 onwards…

SWELECT ENERGY SYSTEMS LTD – some information from Annual report (29-07-2024)

Hi, was anyone able to attend the AGM?

IDFC First Bank Limited (29-07-2024)

Pl dont mind, but my sense is you are clutching at straws to vent your feelings and quoting out of context. I heard the full concall.

-

The comment was made in the context when someone asked why the nbfc was more profitable. He never said he regretted the license. On the contrary he praised dr. Lal for acquiring grama vidyal and helping them grow psl.

-

Cost to income ratio … see rbl bank, yes bank these are in 60s and 70 C I ratios.

You are sayiing deapite being in operation for 10 years by 2027. Hello, 10 years is nothing for building liab franchise. It takes much longer. Anycase first 3 of thise 10 years were useless…

On the contrary capital first shareholder like me should be and is upset that he cleaning the unsolvable issue of idfc bank with 1.6 pc nim 95 pc cost to income ratio. So 8 years effectively from 2019 to 2027, if vv really brings cost to income to 65, it will be a super great achievement.

I spoke to a few managers and they said they are using his name for raising deposits, customers also say if vv is there all is great and give more deposits… am not eulogising, just quoting. For whatever it is worth the name is a good name

On book quality, they have clearly called out the extent and said 20 bps.

On returns i have tracked and commented on this stock feom day 1 of merger (commented negatively). Stick was some 38 at merger. Today 75. Up 100 pc. Pls check your facts.

Nifty private bank given 69 pc probably because of hdfc kotak heavyweights

All in all think they are delivering on the counts and practically saved the bank, though doing a great job of a job they shouldnt be doing in the first place…

Warren buffet also said its not worth doing well what is not worth doing at all

What was the need for capital first to get banking licence so much? It should have just gone and got a banking license directly… it would be smiling all the way with its own deposits.

Krishca Ltd : A SME offering steel strapping Solution (29-07-2024)

The success story of Krishca Strapping Solutions.

Rajesh’s portfolio (29-07-2024)

Doing nothing is fine as almost all stocks are doing well as per hypothesis and will review next year in June unless something great comes up. Sonalis consumer has brought much anticipated quarterly business and looks multibagger. We dont need more than a dozen stocks with large allocation.

Voltamp Transformers (29-07-2024)

Q1FY25 results are very good Y-O-Y and lower than than Q4FY24.

The point to note here is that management has stated that commodity prices are going up and scarcity of CRGO material with increasing price trend would increase input costs .

… The Company at present is witnessing healthy enquiry pipeline. However, with the

steep run up in material prices, orders closing take longer time at purchasers’ end.

New projects announcement by private corporates is yet to get momentum post

election results. Looking ahead, the business outlook likely to remains stable,

boosted by steady domestic demand and continued government support for

green energy and infrastructure projects.

… The challenge going forward is with increased demand for transformers in local and international markets managing supply chain i.e sourcing required raw material and components at budgeted cost with timely supply. The lower commodity prices have supported corporate profitability in FY:24 but recent trends of uptick in input prices, led by industrial metal prices and scarcity of CRGO material is likely to result in higher input cost going forward.

In view of the above, it appears margins might have peaked in Q3/Q4FY24. And Q2 FY 25 results may not match sequential result trend.

Discl: Invested and pruned partial qty at todays’s price post results. I am not qualified to advice and take my opinion with pinch of salt.

Bull therapy 101-thread for technical analysis with the fundamentals (29-07-2024)

Associated Alcohols & Breweries Company came up with good set of results after muted last few quarters.

Fundamentally, company is slowly moving into premium products – introduced premium Gin in the last quarter, premium Single Malt whiskey this quarter and several other drinks lined up for the next couple of quarters. They are also tapping into several new states like Maharashtra, UP, Goa, Pondicherry etc. This should give a big boost to the overall revenue going into the future. On top of that capacity utilization for the ethanol plant will be fully ramped up this year.Promoter did some buying as well in the last quarter.

Technically, the chart is very well placed. It completed the rounding bottom pattern and broke the lifetime highs at 650 with good volumes, retraced and retested the level and continued its upward journey last week.

P.S. this is my first post in the thread, so please excuse if any mistakes.

disc. invested.