Shouldn’t this apply to Suprajit as well?

Posts in category Value Pickr

Omkar’s Portfolio Analysis and Discussion (27-07-2024)

Mankind is buying BVS with EV = 13500 Cr for EV/EBIDTA = 22. The current cash on the book is around 2500 Cr. This falls in bucket 2 capital allocation error for me where I perceive it is wrong and I can not relate with the decision

Again it can turn out to be one of the best acquisitions in the history but I am not confirmable and willing to put my money and time on such managements. I am more than happy to watch them becoming multi baggers from side lines

In capital markets, growth is ‘addictive’. I like to partner with managements which exercise “restraint” but still show agrresion. My belief is managements will not say these things explicitly in investor interactions but one has to deduce them by observing their actions over cycles

Gujarat Themis Biosyn Ltd – Bulk Drugs growth momentum (27-07-2024)

- Positive Start to Fiscal Year:

- Performance met expectations in Q1.

- Sales and Production:

- Sales lower due to selling built-up inventory in previous quarters.

- Production capacity remained optimal.

- Strong demand for products.

- Capex Updates:

- New R&D facility: Half operational, new molecule development underway.

- More R&D sections to be commissioned in the next few months.

- API block: Plant and lab work ready, equipment qualification ongoing.

- Pilot plant batches to begin in a couple of months.

- Additional fermentation capacity: Civil construction halfway completed.

- Capex execution progressing as planned.

Investing Basics – Feel free to ask the most basic questions (27-07-2024)

Thank you @Prashant_Karandikar @aditya14920251 @keeyes for sharing your views on the matter. I too find the reasoning a little unconvincing.

Ranvir’s Portfolio (27-07-2024)

FEDERAL BANK –

Q1 results and concall highlights –

Deposits @ 2.66 lakh cr, up 20 pc

Advances @ 2.20 lakh cr, up 20 pc

NII up 19 pc @ 2592 cr

Fee income grew 22 pc @ 652 cr

Other income grew 25 pc @ 915 cr

NIMs @ 3.16 vs 3.20 pc

Gross NPAs @ 2.11 vs 2.38 pc

Net NPAs @ 0.60 vs 0.69 pc

High yielding segments grew at faster rates ( However, these segments grew on a lower base ) –

CV/CE loans up 51 pc @ 3.7k cr

MFI loans up 107 pc @ 3.7k cr

MSME book up 22 pc @ 40.1 k cr

Credit cards book up 73 pc @ 3.2k cr

Gold loans book up 31 pc @ 27.4k cr

Total high yielding book @ 35 pc of total loan book. Growth in high yielding segments is critical for the bank as their NIMs are on the lower side

CASA deposits grew by 10 pc @ 77k cr vs 70k cr YoY. CASA ratio @ 29 vs 33 pc YoY

CASA + Deposits < 3 cr form 80 pc of the Deposit book vs 84 pc YoY

Retail : Wholesale loan book @ 56:44

Yield on advances @ 9.43 vs 9.21 pc

Fresh slippages @ 417 cr – very well controlled – this to me is the key highlight of the results

Expecting the credit quality to remain within control for rest of FY 25 ( at similar levels as in Q1 )

Cost / Income @ 53 pc. Added 210 branches in last 18 months. Despite that, cost / income is trending downwards ( vs Q4 ). Aim to bring to down to 50 pc within 1.5-2 yrs time

Aim to add > 100 branches in FY 25. This should also help in deposit mobilisation

Federal bank’s loans are generally priced lower than other banks in most of the segments they operate. As a result, they are able to get best customers, lower slippages ( its reflected in the numbers as well ). But it comes at the cost of lower NIMs. But this is a deliberate ( and very conservative ) policy

Expect the NIMs to be around Q1 levels for Q2,Q3

Expect to exit FY 25 with RoA @ 1.35 pc vs 1.27 pc in Q1. That should mean – continued momentum in Deposits, Advances and control over slippages

Disc: holding from lower levels, things looks well within control, doesn’t look expensive at CMP, not SEBI registered, biased, not a buy / sell recommendation

Federal Bank – A Turnaround banking Story? (27-07-2024)

FEDERAL BANK –

Q1 results and concall highlights –

Deposits @ 2.66 lakh cr, up 20 pc

Advances @ 2.20 lakh cr, up 20 pc

NII up 19 pc @ 2592 cr

Fee income grew 22 pc @ 652 cr

Other income grew 25 pc @ 915 cr

NIMs @ 3.16 vs 3.20 pc

Gross NPAs @ 2.11 vs 2.38 pc

Net NPAs @ 0.60 vs 0.69 pc

High yielding segments grew at faster rates ( However, these segments grew on a lower base ) –

CV/CE loans up 51 pc @ 3.7k cr

MFI loans up 107 pc @ 3.7k cr

MSME book up 22 pc @ 40.1 k cr

Credit cards book up 73 pc @ 3.2k cr

Gold loans book up 31 pc @ 27.4k cr

Total high yielding book @ 35 pc of total loan book. Growth in high yielding segments is critical for the bank as their NIMs are on the lower side

CASA deposits grew by 10 pc @ 77k cr vs 70k cr YoY. CASA ratio @ 29 vs 33 pc YoY

CASA + Deposits < 3 cr form 80 pc of the Deposit book vs 84 pc YoY

Retail : Wholesale loan book @ 56:44

Yield on advances @ 9.43 vs 9.21 pc

Fresh slippages @ 417 cr – very well controlled – this to me is the key highlight of the results

Expecting the credit quality to remain within control for rest of FY 25 ( at similar levels as in Q1 )

Cost / Income @ 53 pc. Added 210 branches in last 18 months. Despite that, cost / income is trending downwards ( vs Q4 ). Aim to bring to down to 50 pc within 1.5-2 yrs time

Aim to add > 100 branches in FY 25. This should also help in deposit mobilisation

Federal bank’s loans are generally priced lower than other banks in most of the segments they operate. As a result, they are able to get best customers, lower slippages ( its reflected in the numbers as well ). But it comes at the cost of lower NIMs. But this is a deliberate ( and very conservative ) policy

Expect the NIMs to be around Q1 levels for Q2,Q3

Expect to exit FY 25 with RoA @ 1.35 pc vs 1.27 pc in Q1. That should mean – continued momentum in Deposits, Advances and control over slippages

Disc: holding from lower levels, things looks well within control, doesn’t look expensive at CMP, not SEBI registered, biased, not a buy / sell recommendation

Aurion Pro : Yet another IP product company? (27-07-2024)

I’m also invested in the comp. since 49 CMP. ![]()

I am slightly concerned about 4 separate businesses the company is trying to push forward. In the recent investor meet, the question was raised on this regarding how they plan to run 4 different business verticals with the same funds and then plan to become global top 3. I wasn’t totally convinced by his answer that some years some business will be pushed based on the conditions.

I don’t expect them to become top player in all those business and I think they are kind of hedging their bets. They are not married to a business rather the goal is to become a large player in one/more of these businesses.

I wish they’d start reporting the numbers by the business for more transparency, probably this is a question/request to be raised in the next concall.

Disclaimer: I am invested and biased.

Aurion Pro : Yet another IP product company? (27-07-2024)

(post deleted by author)

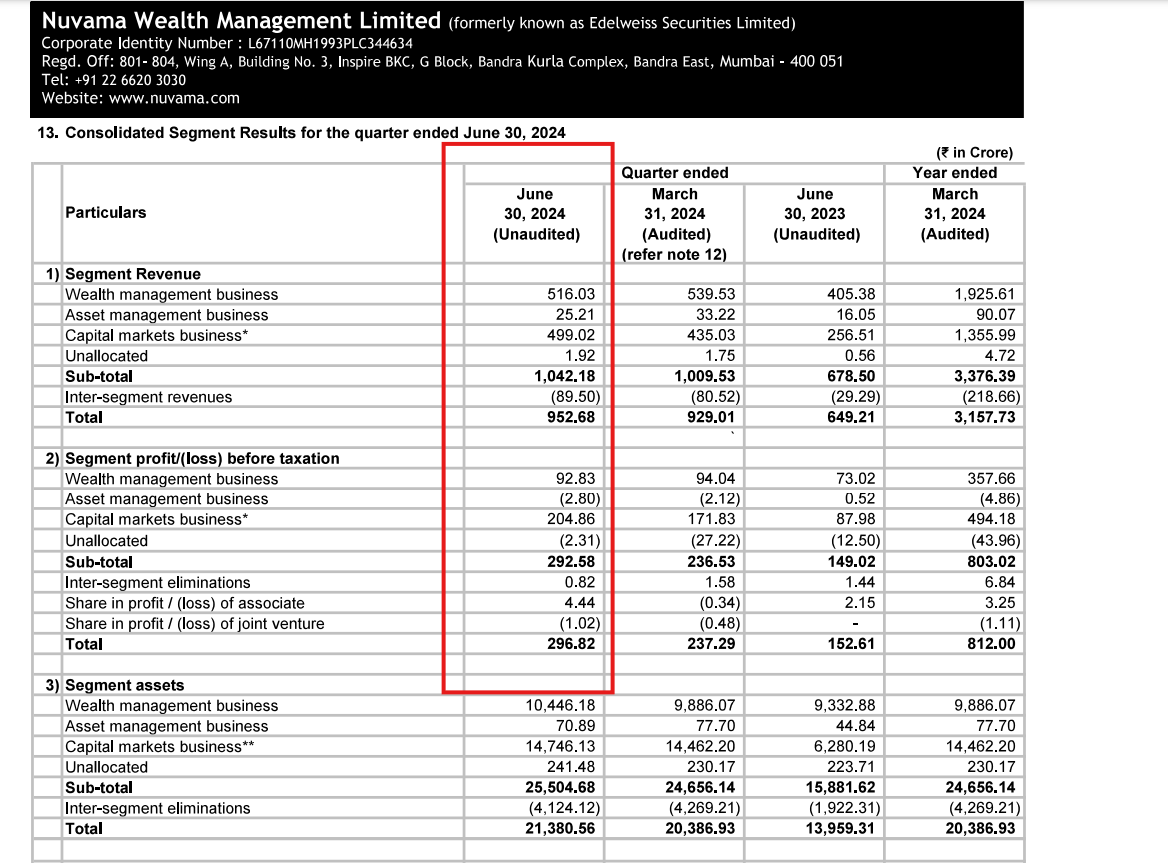

Nuvama Wealth Management: Proxy to Affluent India (27-07-2024)

I agree with the profit part, but I don’t understand how this RM addition and Dubai investment could affect the WM segmental revenue(topline) growth.

In fact, looking at the WM segment on a longer time frame

Revenue: Q2FY23 → 455 : Q1FY25 → 516

PBT: Q2FY23 → 105 : Q1FY25 → 93

I know revenue to AUM should not be looked at in a linearity. But in about 2 years where AUM grew 30-40% CAGR, where is the incremental ARR?

On a positive note, I hope the WM revenue can jump exponentially in the coming quarters, looking at how revenue recognition has been falling behind the exceptional AUM growth.

Microcap momentum portfolio (27-07-2024)

deploying same amount to each stock each week.

for eg, you have 2L to invest for this week, it’ll be 2L/20stocks = 10k in each stock irrespective of their current weight.

@visuarchie , suggests that you invest money in each stock so that their weights become equal.