Posts in category Value Pickr

Varun beverages fast growth duopoly business (22-07-2024)

Commercial production of carbonated soft drinks and packaged drinking

water at its production facility at Kinshasa, Democratic Republic of Congo has been started as stated by company

Stylam- Decent Fundamentals with Cheap Valuation (22-07-2024)

Thank you for sharing this new product of Stylam.

Countertop material decision is driven by use-case and price difference between the alternatives.

Quartz really made its inroads and started replacing granite on a bigger scale when the designs of Quartz started matching and improving that of natural granite while the pricing difference also came to a level where user was ready to pay up for that upgrade. Long time ago price difference between granite and quartz was so huge that Quartz was considered a luxury countertop.

This acrylic solid surface product might find its applications in hotels (extended stays), rental properties, apartment complexes, hospitals, businesses, etc. I don’t think it can make inroads in residential houses which are mid grade and above.

One needs to dig through the price difference between laminate solid surface, acrylic solid surface, quartz, and granite to better understand the value migration and size of opportunity.

Once we understand the price difference (including final application project cost), only then we can have a view on what level of impact it can have on Pokarna, Acrysil type of businesses.

Piccadily Agro Industries Ltd (22-07-2024)

With the little knowledge I have of capital markets, I find it little difficult to compare as Allied Blenders focuses more on volume growth with their entry level IMFL segment whiskey (OPM 7%) as compared to Piccadily which is more into the premium segment with more focus on margin growth as compared to volume with OPM of 25%. Still volume wise, Piccadily still has a long way to go. Hopefully the ongoing capacity expansion which gets completed next year will help with volume growth. Also, since the number of investors in Piccadily has gone up from 21k to 70k in past 3 years, whether the stock is still undiscovered is anyone’s guess.

Request senior VP members to correct my mistakes

Aarti Pharma Labs (22-07-2024)

Aarti Pharmalabs – ( extremely bullish commentary wrt medium to long term ) –

Q4 and FY 24 results and concall highlights –

Manufacturing footprint –

Atali – New Unit under construction for CDMO, making Intermediates

Dombivali – Unit -1 – APIs, Intermediates, CDMO

VAPI – Unit -2 – APIs, Intermediates, CDMO

Tarapur – Unit -3 – Xanthine Unit

Unit -4 – APIs, CDMO

Unit -5 – Xanthine Unit

Unit – 6 – Xanthine intermediates and allied products

Segment wise revenues breakup in Q4 –

Xanthine, its derivates and allied products – 44 pc vs 50 pc YoY

API and Intermediates – 37 vs 43 pc YoY

CDMO / CMO – 19 vs 6 pc ( that’s a huge jump )

Aarti Pharma labs is the largest manufacturer of Xanthine, Caffeine ( a Xanthine derivative ) in India. Aarti Pharma’s global mkt share in Xanthine and derivatives is > 15 pc

Other Xanthine derivates are used as mild stimulants and bronchodilators ( for management of Asthma and Influenza )

Aarti Pharmalabs is a key beneficiary of China +1 wrt all its business segments

Most of the APIs that the company makes have a good degree of backward integration giving them good control over the entire value chain

Domestic : International sales breakup for FY 24 @ 56:44. Out of the total international sales, aprox 80 pc are to the regulated Mkts ( a great indicator of organisations’s compliance and quality culture )

In their CDMO business, they are currently working on 16 innovator molecules in various stages of development

Aim to grow topline by an avg of 10-15 pc for next 3 yrs

FY 24 outcomes –

Revenues – 1852 vs 1945 cr

EBITDA – 386 vs 342 cr

PAT – 216 vs 193

Net Debt / Equity @ 0.14 vs 0.13 pc

RoCE – 18 pc

RoE – 14 pc

Q4 outcomes –

Revenues – 505 vs 448 cr

EBITDA – 117 vs 80, up 47 pc ( margins @ 23 vs 17 pc )

PAT – 65 vs 42 cr, up 53 pc

Company’s API business has a greater focus towards regulated mkts. Their key therapeutic areas include – Anti-Hypertensive, Ant-Diabetic and Oncology drugs

Company is going to undertake brownfield expansion for capacity addition of the Xanthene and derivatives. Aim to take the total capacity up to 750 MT/ Month by end of FY 25. Current capacity is around 425 MT/ Month – so that’s a substantial jump

Guiding for a 10-12 pc EBITDA growth in FY 25. Management admitted that its a conservative guidance since the company did have exceptionally good q4

CMO / CDMO is likely to remain a high growth area for the company for next 2-3 yrs.Should grow @ > 30-35 CAGR for next 2-3 yrs. CMO/CDMO business is margin accretive for the company

Current capacity utilisation of the Xanthene plants @ 90 pc, hence the brownfield expansion

Company believes that the Xanthene prices have bottomed out. Should only go higher from here

FY 25 is going to be a Capex heavy year. Company may end up spending to the tune of 600 cr for the brownfield Capex for Xanthene + plus the ongoing projects projects @ Atali ( that’s a lot of Capacity addition )

Most of the company’s CMO business is concentrated on supply of KSMs ( key starting products ) / RSMs ( regulated starting materials )

Breakup of capex for FY 25 –

Aprox 300 cr for ongoing expansion @ Atali

80-90 cr for Solar power projects ( for future savings on the energy costs. Post this, 1/3rd of company’s power requirements shall be met internally )

Rest for brownfield expansion for Xanthene and other small capexes at various locations

Company is confident of achieving ideal capacity utilisation on the expanded Xanthene capacities inside 2-3 yrs !!! ( this should result in a lot of growth )

Tax rate for FY 24 for the company was 28 pc. Should be around of 25 pc for FY 25

Disc: holding, biased, not SEBI registered, not a buy / sell recommendation

How to register with SEBI as a Research Analyst? (22-07-2024)

any NISM Exam Preparation Guide for NISM-Series-XV.

please give me some pdf

Ranvir’s Portfolio (22-07-2024)

Aarti Pharmalabs – ( extremely bullish commentary wrt medium to long term ) –

Q4 and FY 24 results and concall highlights –

Manufacturing footprint –

Atali – New Unit under construction for CDMO, making Intermediates

Dombivali – Unit -1 – APIs, Intermediates, CDMO

VAPI – Unit -2 – APIs, Intermediates, CDMO

Tarapur – Unit -3 – Xanthine Unit

Unit -4 – APIs, CDMO

Unit -5 – Xanthine Unit

Unit – 6 – Xanthine intermediates and allied products

Segment wise revenues breakup in Q4 –

Xanthine, its derivates and allied products – 44 pc vs 50 pc YoY

API and Intermediates – 37 vs 43 pc YoY

CDMO / CMO – 19 vs 6 pc ( that’s a huge jump )

Aarti Pharma labs is the largest manufacturer of Xanthine, Caffeine ( a Xanthine derivative ) in India. Aarti Pharma’s global mkt share in Xanthine and derivatives is > 15 pc

Other Xanthine derivates are used as mild stimulants and bronchodilators ( for management of Asthma and Influenza )

Aarti Pharmalabs is a key beneficiary of China +1 wrt all its business segments

Most of the APIs that the company makes have a good degree of backward integration giving them good control over the entire value chain

Domestic : International sales breakup for FY 24 @ 56:44. Out of the total international sales, aprox 80 pc are to the regulated Mkts ( a great indicator of organisations’s compliance and quality culture )

In their CDMO business, they are currently working on 16 innovator molecules in various stages of development

Aim to grow topline by an avg of 10-15 pc for next 3 yrs

FY 24 outcomes –

Revenues – 1852 vs 1945 cr

EBITDA – 386 vs 342 cr

PAT – 216 vs 193

Net Debt / Equity @ 0.14 vs 0.13 pc

RoCE – 18 pc

RoE – 14 pc

Q4 outcomes –

Revenues – 505 vs 448 cr

EBITDA – 117 vs 80, up 47 pc ( margins @ 23 vs 17 pc )

PAT – 65 vs 42 cr, up 53 pc

Company’s API business has a greater focus towards regulated mkts. Their key therapeutic areas include – Anti-Hypertensive, Ant-Diabetic and Oncology drugs

Company is going to undertake brownfield expansion for capacity addition of the Xanthene and derivatives. Aim to take the total capacity up to 750 MT/ Month by end of FY 25. Current capacity is around 425 MT/ Month – so that’s a substantial jump

Guiding for a 10-12 pc EBITDA growth in FY 25. Management admitted that its a conservative guidance since the company did have exceptionally good q4

CMO / CDMO is likely to remain a high growth area for the company for next 2-3 yrs.Should grow @ > 30-35 CAGR for next 2-3 yrs. CMO/CDMO business is margin accretive for the company

Current capacity utilisation of the Xanthene plants @ 90 pc, hence the brownfield expansion

Company believes that the Xanthene prices have bottomed out. Should only go higher from here

FY 25 is going to be a Capex heavy year. Company may end up spending to the tune of 600 cr for the brownfield Capex for Xanthene + plus the ongoing projects projects @ Atali ( that’s a lot of Capacity addition )

Most of the company’s CMO business is concentrated on supply of KSMs ( key starting products ) / RSMs ( regulated starting materials )

Breakup of capex for FY 25 –

Aprox 300 cr for ongoing expansion @ Atali

80-90 cr for Solar power projects ( for future savings on the energy costs. Post this, 1/3rd of company’s power requirements shall be met internally )

Rest for brownfield expansion for Xanthene and other small capexes at various locations

Company is confident of achieving ideal capacity utilisation on the expanded Xanthene capacities inside 2-3 yrs !!! ( this should result in a lot of growth )

Tax rate for FY 24 for the company was 28 pc. Should be around of 25 pc for FY 25

Disc: holding, biased, not SEBI registered, not a buy / sell recommendation

Long term investment strategy (Buy, hold but don’t forget) (22-07-2024)

Hi @Amit_Paul

Thanks for remembering me:joy:![]() . Yup am doing excellent as of now, its 45X on PF in last 4 years, from March 24, up close to 45% now.

. Yup am doing excellent as of now, its 45X on PF in last 4 years, from March 24, up close to 45% now.

Hits Kalyan, AB Fashion, Force, moderate gains in rest of stocks (20-80%)

Exits: Narayana Hrudalaya (-4%) brand concepts (150%)

New entries Piccadilly agro, Samhi Hotels

Kalyan Jeweller ( 24%) 450% gains

Force motors ( 8%) 700% gains

Aditya Birla Fashion ( 25%) 30% gain

Aditya Birla Capital ( 9%) 100% gains

Tata power ( 3%) 25% gains

AGI Green ( 3%) 225% gains

Arvind Fashion ( 6%) 60% gains

Sanghvi Mover ( 3%) 20% gains

LT Food (3%) 90% gains

Thomas Cook (2.5) 100% gains

Wockhardt ( 7%) increased bet size

New

Piccadily agro 3% ( testing waters)

Samhi Hotels 3.5 % (accumulation)

Trading positions

- Swelect Energy

- Ion exchange

- PVRINOX

- Rushil Decor

5 BHEL

6 LIC Housing

7 Suzlon

8 watech vabag

9 Gulshan Poly

I am bit cautious on markets now as froth is building everywhere. Main killer in last 3 months was AB Fashion which was a losing position and gained from 208 levels to 330 in 4 month, capital allocation at 208 was close of 35% of PF with highly leveraged position, cashed out gains on 50% and converted remaining to delivery, playing on upcoming demerger as i feel post demerger valuation will rise to 500 levels.

Kalyan and force are real star, its nonstop for Kalyan, thanks to initial capital allocation of 20% despite its rise of 5.3 X from May 23, it still around 24% amid surge in other portfolio stocks, diluted 10% to shift capital in wockhardt. Still planning to hold this for 1000 as titan is shaken now by kalyan hence MF FII loyalty is shifting.

I am avoiding all Cap goods, Defence, Semi conductor stocks for now and all PSU basket, BHEL is exception as i still finding value in it.

Samhi Hotels looks interesting bet from risk reward perspective.

Water is next theme to invest, Ion exchange, EMS, Va tech wabag and Jash are good choice.

Cautious outlook on markets post budget as lot of churn will take place from hot sectors, consumer focus might come back due to political setback for BJP in last elections.

RS Software – Will they pay investors too? (22-07-2024)

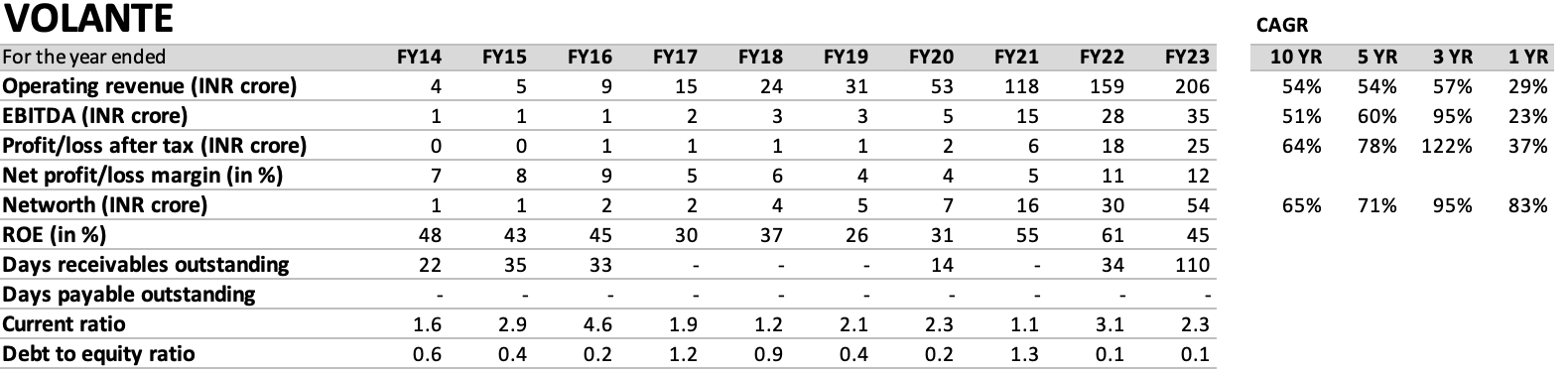

Here are Volante’s financial statements from the last decade. The company has shown a consistently high CAGR; quality growth it has been.

Source: Tofler

Volante Financials v1.xlsx (13.7 KB)

Can RS Software deliver similar return ratios and growth if (big IF) and when the co starts firing on multiple product lines?