Ashish kacholia has reduced stake in the company, although his style of investing has been of if not completely momentum, then at least it is factored in in his investing, will have to check the results for the next quarter, then only i will take a call.

Posts in category Value Pickr

A Discussion Thread is missing: Poof! Gone (09-07-2024)

There used to exist a discussion thread named ‘Smallcap Hunter’. It’s gone missing since yesterday. Can anyone throw some light? What could have happened?

I used to think that one can delete one’s own reply, but is it possible to delete the whole thread by the initiator of the thread?

Responsive Industries: Luxury Flooring Brand? (08-07-2024)

The company seems to have good order book for the coming 2 quarters as per the recent con-call

Responsive Industries: Luxury Flooring Brand? (08-07-2024)

Any reason for no growth in sales ?

Raymond – The Complete Man (08-07-2024)

In demerger, the company’s worth or market capitalization before and after the demerger matches. Equity or number of shares pre and post does not match.

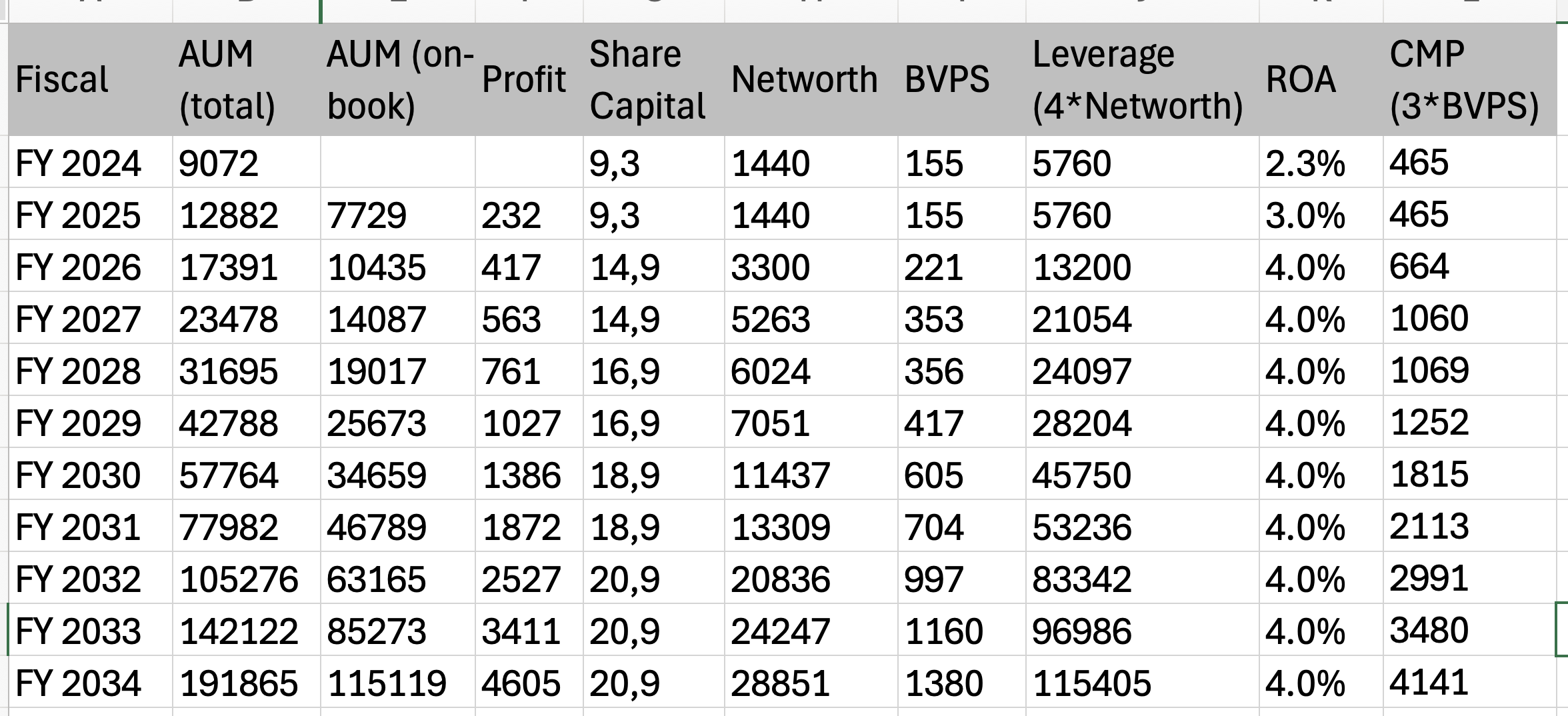

Ugro Capital – Opportunity To Invest in a Fintech-like Company Below Book Value (08-07-2024)

Assumption:

AUM growth of 30% continuously for the next 10years. IMHO it is doable, the TAM is huge, if management has a good control over the ALM, this rate of growth shouldn’t be a problem.

ROA on continuous basis = 4%

Co-lending percentage = 50%

Fund raising in 2028, 2030 and in 2032 by QIP of 2cr shares in each fund raise.

Note:

- Not considering any AUM and PAT addition from Myshubhlife acquisition and any other potential future acquisitions.

- ROA of 4% is on the lower side, it could be higher going forward basis controlled credit cost.

- Valuation of 3BVPS is also on the lower side. It could easily trade at 4BVPS if market wants to give the premium valuation.

Note2: This is a very naive and superfluous analysis with several assumptions, however I sill think Ugro capital has very scalable business model and market at some point in time reward it.

Invested and biased.

Ugro Capital – Opportunity To Invest in a Fintech-like Company Below Book Value (08-07-2024)

There is a lot of scope however in the short term, I feel competition is rising and there are headwinds with growing NPAs. Ujjivan lowered guidance and said its credit costs will normalize ( Source : recent concall ). Thus in the short maybe the thesis may not pan out

Sandhar Technologies – An emerging market leader (08-07-2024)

Sandhar Technologies ( very bullish commentary ) –

Q4 and FY 24 results and concall highlights –

Company’s product profile –

Automotive locking systems, Latches, Hinges and Door handles

Auto Vision Systems ( basically rear view mirrors )

Sheet metal components for 2W, 3W, PVs, CVs

Operator Cabins for OTR vehicles and CVs

Zinc dye-casting products for 2W, 3W, PVs and CVs

Aluminium dye – casting products for 2W, 3W, PVs and CVs

Magnesium dye – casting products – recently acquired a manufacturing facility for the same

Automotive Opto Electronic systems like – keyless entry systems, reverse parking assist systems etc

Polymer based products for 2W and 3W

Painting, plating and coatings

Fuel Pumps, filters and Wiper blades

Wheel rims and Handle bars for 2W

Q4 outcomes –

Sales – 918 vs 765 cr, up 19 pc

EBITDA – 98 vs 68 cr, up 35 pc ( margins @ 11 vs 9 pc )

PAT – 36 vs 25 cr, up 42 pc

FY 24 outcomes –

Sales – 3521 vs 2909 cr, up 21 pc

EBITDA – 341 vs 246 cr, up 34 pc (margins @ 10 vs 8 pc)

PAT – 110 vs 74 cr, up 45 pc

Company’s clients –

2W – Hero, TVS, RE, Honda, Ather, Suzuki, Mahindra

4W – Tata Motors, Mahindra, Honda, SML ISUZU

CV – JCB, Ashok Leyland, Volvo, Komatsu, Tata-Hitachi

Manufacturing facilities –

Company has manufacturing facilities located in –

Domestic – HP, Uttarakhand, Maharashtra, Gujarat, TN, Rajasthan, Karnataka

International – Poland, Romania, Spain, Mexico, South Korea, Japan, Taiwan

Product wise revenue split –

Locking and Vision systems – 25 pc

Cabins and fabrications – 15 pc

Sheet metal parts – 15 pc

Aluminium Dye Castings – 24 pc

Assemblies – 10 pc

Others – 10 pc

Segment wise revenue split –

2W – 58 pc

PV – 20 pc

Off-Highway vehicles – 15 pc

CVs – 2 pc

Others – 5 pc

New products line up –

EV Motor controller for 2W/3W – production to start in Jun 24

EV battery chargers for 2W/3W – production to start in Jul 24

DC – AC converter for 2W/3W – production to start in Oct 24

Company has done a lot of Capex in the last 2 yrs in its sheet metal parts and Dye – Casting divisions. This Capex can potentially add revenues of around 1500-1700 cr for the company without incurring any fresh capex. However, the company may still incur capex going fwd as it looks to add new components to its portfolio

Company should be able to grow its topline by 20 pc in FY 25 as well with a 50-100 bps margin expansion

Company has added Smart Locks to its product line up. Suzuki and Honda are moving onto these smart locks wef Oct and Nov 24. This should be a major Pivot for the company as the content per vehicle in these locking systems is far higher

Most of the growth in FY24 was led by Dye Casting and Sheet Metal segments

The value of Motor controllers that company is slated to begin to produce varies from Rs 4k-8k per vehicle

Company aspires to keep growing @ 15-20 pc CAGR ( revenues ) for next 3-5 yrs

Disc: planning to add, not SEBI registered, biased

Ranvir’s Portfolio (08-07-2024)

Sandhar Technologies ( very bullish commentary ) –

Q4 and FY 24 results and concall highlights –

Company’s product profile –

Automotive locking systems, Latches, Hinges and Door handles

Auto Vision Systems ( basically rear view mirrors )

Sheet metal components for 2W, 3W, PVs, CVs

Operator Cabins for OTR vehicles and CVs

Zinc dye-casting products for 2W, 3W, PVs and CVs

Aluminium dye – casting products for 2W, 3W, PVs and CVs

Magnesium dye – casting products – recently acquired a manufacturing facility for the same

Automotive Opto Electronic systems like – keyless entry systems, reverse parking assist systems etc

Polymer based products for 2W and 3W

Painting, plating and coatings

Fuel Pumps, filters and Wiper blades

Wheel rims and Handle bars for 2W

Q4 outcomes –

Sales – 918 vs 765 cr, up 19 pc

EBITDA – 98 vs 68 cr, up 35 pc ( margins @ 11 vs 9 pc )

PAT – 36 vs 25 cr, up 42 pc

FY 24 outcomes –

Sales – 3521 vs 2909 cr, up 21 pc

EBITDA – 341 vs 246 cr, up 34 pc (margins @ 10 vs 8 pc)

PAT – 110 vs 74 cr, up 45 pc

Company’s clients –

2W – Hero, TVS, RE, Honda, Ather, Suzuki, Mahindra

4W – Tata Motors, Mahindra, Honda, SML ISUZU

CV – JCB, Ashok Leyland, Volvo, Komatsu, Tata-Hitachi

Manufacturing facilities –

Company has manufacturing facilities located in –

Domestic – HP, Uttarakhand, Maharashtra, Gujarat, TN, Rajasthan, Karnataka

International – Poland, Romania, Spain, Mexico, South Korea, Japan, Taiwan

Product wise revenue split –

Locking and Vision systems – 25 pc

Cabins and fabrications – 15 pc

Sheet metal parts – 15 pc

Aluminium Dye Castings – 24 pc

Assemblies – 10 pc

Others – 10 pc

Segment wise revenue split –

2W – 58 pc

PV – 20 pc

Off-Highway vehicles – 15 pc

CVs – 2 pc

Others – 5 pc

New products line up –

EV Motor controller for 2W/3W – production to start in Jun 24

EV battery chargers for 2W/3W – production to start in Jul 24

DC – AC converter for 2W/3W – production to start in Oct 24

Company has done a lot of Capex in the last 2 yrs in its sheet metal parts and Dye – Casting divisions. This Capex can potentially add revenues of around 1500-1700 cr for the company without incurring any fresh capex. However, the company may still incur capex going fwd as it looks to add new components to its portfolio

Company should be able to grow its topline by 20 pc in FY 25 as well with a 50-100 bps margin expansion

Company has added Smart Locks to its product line up. Suzuki and Honda are moving onto these smart locks wef Oct and Nov 24. This should be a major Pivot for the company as the content per vehicle in these locking systems is far higher

Most of the growth in FY24 was led by Dye Casting and Sheet Metal segments

The value of Motor controllers that company is slated to begin to produce varies from Rs 4k-8k per vehicle

Company aspires to keep growing @ 15-20 pc CAGR ( revenues ) for next 3-5 yrs

Disc: planning to add, not SEBI registered, biased

Ugro Capital – Opportunity To Invest in a Fintech-like Company Below Book Value (08-07-2024)

Hi Deepak, could you explain the rationale and assumptions behind 15x?