Posts in category Value Pickr

Pratik’s Portfolio – Review (27-06-2024)

Shakti Pumps

Beneficiary of PM Kusum Scheme*1 – Subsidy scheme to install new solar pumps and replace the existing electrical/diesel pumps to reduce the dependency of grid power. In FY 2018-19, a ₹480 bn budget was setup for a 10-year period

Market Share – SPIL claims to have a ~26% Market Share* in PM KUSUM Scheme in volume terms. My estimate indicates that they are now installing approx. 40% of total pumps under this scheme.

Fund raise: SKPI has raised INR200cr (at INR1,209/share) via a qualified institutional placement (QIP) with SBI Mutual Fund and LIC Mutual Fund in March. This boosts the fund’s holding by ~4.1% each. The proceeds will be utilised to fund capacity expansion at its new facility in Pithampur, Madhya Pradesh. This facility will manufacture pumps and motors, inverters, variable frequency drives (VFDs), and structures.

Current Capacity – 5,00,000 units of pumps manufacturing facility located at Pithampur (MP). Solar structure for solar panel 1,00,000 units capacity. Inverters/VFD’s 2,00,000 units

New capacity – “With the recent fund raise, the management aims to set up a new facility which will double the production capacity of pumps/motors to 10lk units, inverters/VFD’s to 4lk units, and structures to 2lk units” Source – Nuvama

Revenue Mix: FY 2023-2024 revenue of 1371 crore. 70% from government projects, 20% from exports, 10% from domestic non-government customers

Revenue Potential–

Annual Revenue potential using 5 lakh pumps: 5 lac units * 3.1 lakh price * 80% OEE = 12,400 crore

Revenue potential using Kusum opportunity capture over 2 years: 50 lac units * 3.1 lakh price * 75% target achievement * 25% market share = 29,000 crore for 2 years

Both the data points indicate significant revenue increase potential over the next couple of years for Shakti Pump if Kusum scheme continues to get traction

Company has an order book of 2,400 crore as at end-FY24

EV upside: Shakti EV Mobility is engaged in the manufacturing and sale of EV motors, charging stations, battery management systems, electric control panels, smart electric control panels, VFDs and other items. SPIL Board has approved investments of Rs. 114.3 crores in Shakti EV Mobility, in one or more tranches over 5 years. Shakti EV has already catered to the two-wheeler and three-wheeler segments and is in the process of testing and developing of other products.

Other considerations:

Promoter is providing conservative estimates and beating it

Promoter forwent his sales commission – sign of a good promoter

I am estimating Arp-Jun 2024 revenue for Shakti pumps to be more than 750 crores

*1 Relevant part of PM Kusum Scheme

Component B:

Individual farmers will be supported to install standalone solar Agriculture pumps of capacity up to 7.5 HP in off-grid areas, where grid supply is not available

Installation of 14 lakh Solar-powered Agricultural Pumps (Offgrid)

Central Financial Assistance of 30% of the cost pump will be provided. The State Government will give at-least a subsidy of 30%; and the remaining at-most 40% will be provided by the farmer. Bank finance can be availed by farmer, so that farmer has to initially pay only 10% of the cost and remaining up to 30% of the cost as loan.

Component C: Individual Pump Solarisation (IPS)

Individual farmers having grid connected agriculture pump will be supported to solarise pumps.

The farmer will be able to use the generated solar power to meet the irrigation needs and the excess solar power will be sold to DISCOMs.

Solarisation of 35 lakh existing Grid-connected Agriculture Pumps (on-grid)

Other opportunity: Replacement of existing diesel pumps • Replacement demand is ~320 lakh pumps with ~220 lakh electric pump and ~100 lakhs diesel pumps

Lt foods (daawat) (27-06-2024)

They got it

Check latest announcements

Last month only high court gave order

Pratik’s Portfolio – Review (27-06-2024)

I didn’t mean that the current PE was cheap. I am looking at the forward PE and find it reasonably valued.

Manappuram Finance (27-06-2024)

Don’t know if it’s a coincidence, but both Muthoot & Manappuram are hiving off their microfinance subsidiaries at a time when there are signs of the cycle turning.

Irrespective of that, I think worth monitoring as MFI has done very well for them in the recent past.

DLINK: Small Company with a Big Brand (27-06-2024)

PnL Statement: (last 9 years)

· Low sales growth except for 2019/22/23

· Low OPM except for 2023/24

· Other income high from 2020

· Low NPM except for 2023/24

· High capex 2020/23

· Low growth of Net Fixed Assets

· Fluctuating receivable days

· Fluctuating Inventory Turnover

· Low RoE except for 2023/24

· Low RoCE except for 2023/24

· High Dividend payout

Highly Competitive Indian Market. Jio, Airtel & others providing their own router.

The revenue & profitability improvement in the year2023 is because of the below factor. Although when we see the year2024 revenue/profitability, there is not much further improvement or progress.

Looks like a highly commoditized market with low profitability margins.

Positive-

D-Link (India) Limited is strongly focusing on local products as part of its ‘Make in India’ initiative. “Make in India,” and localization of products are two important initiatives of the Indian government that are closely linked. D-Link (India) has been granted exclusive rights/ license by the parent company to use the D-Link trademark for such

locally manufactured products. The Company had made strategic decisions on manufacturing certain products locally through third-party or contract manufacturing with its own brand names, under its own proprietary designs, quality control and supervision.

The Company has made noteworthy progress in this direction and has entered into arrangements with local manufacturers.

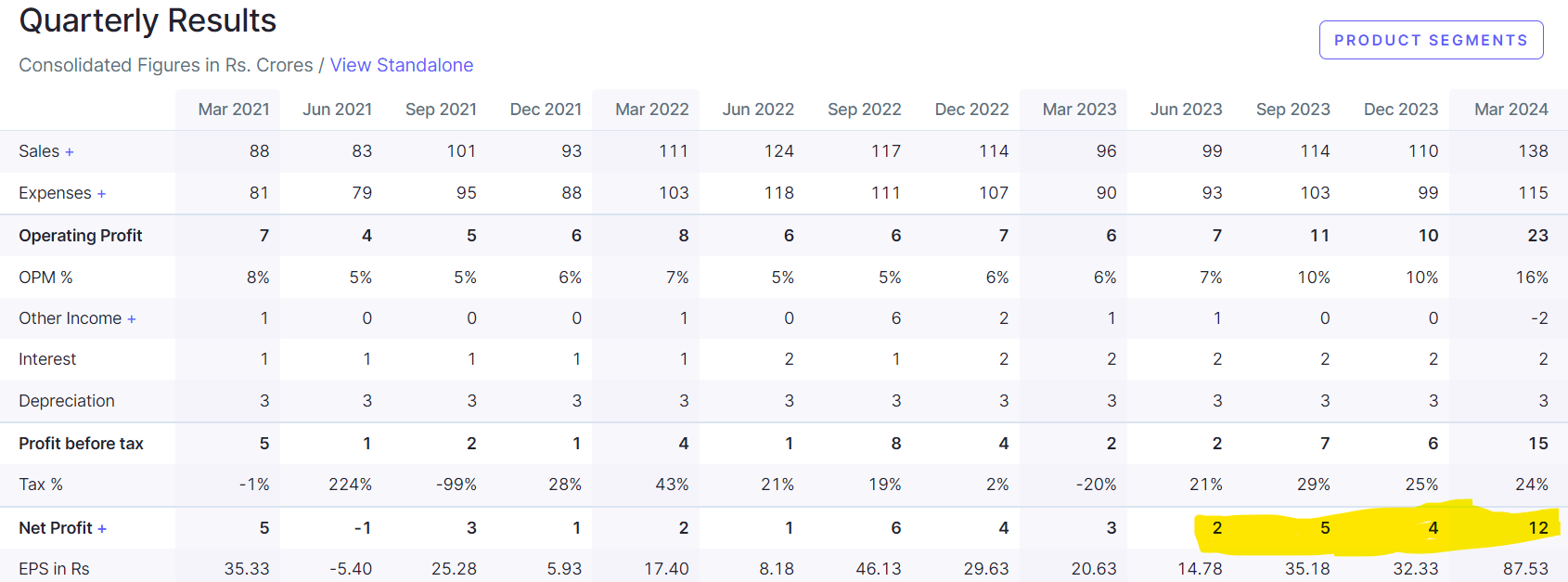

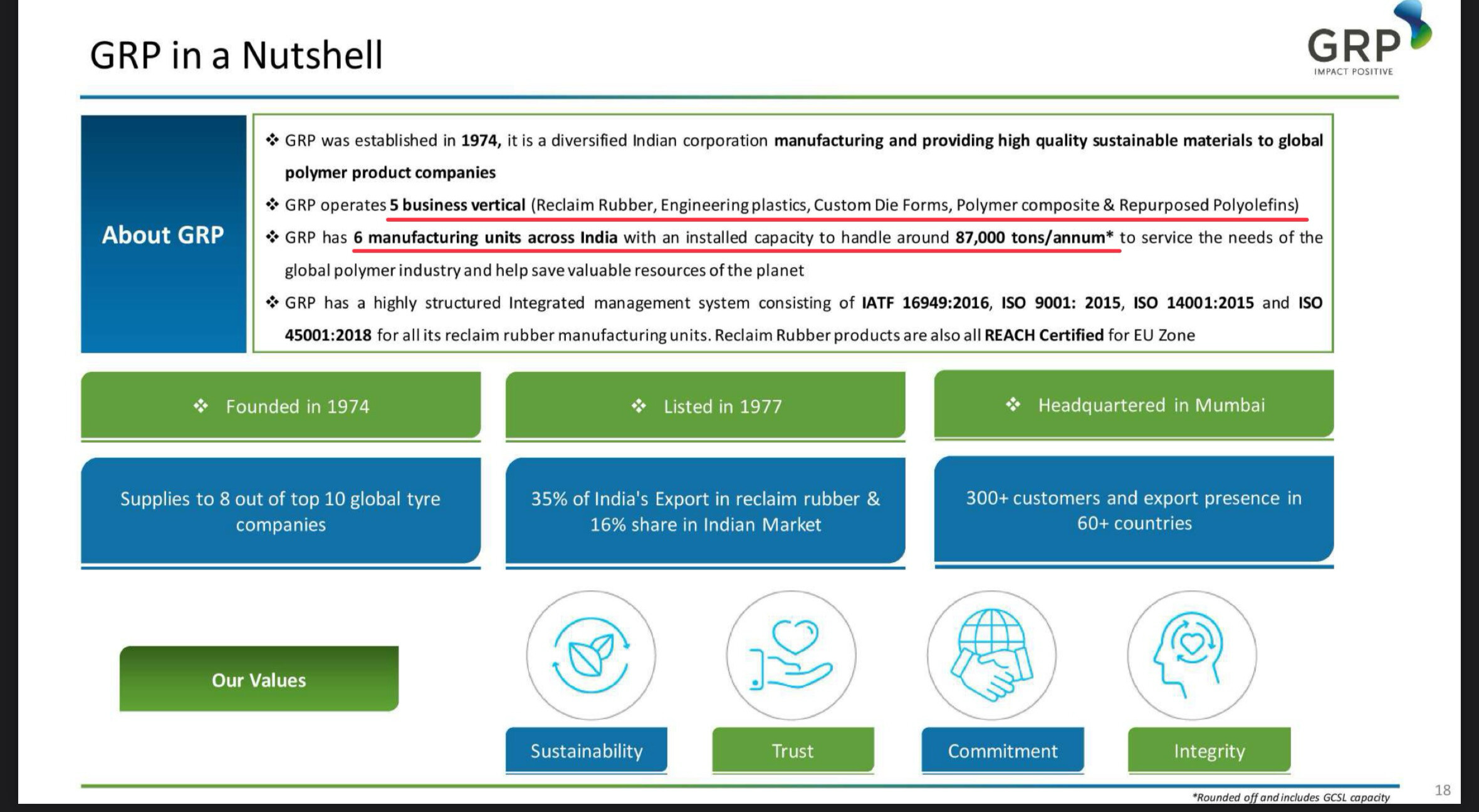

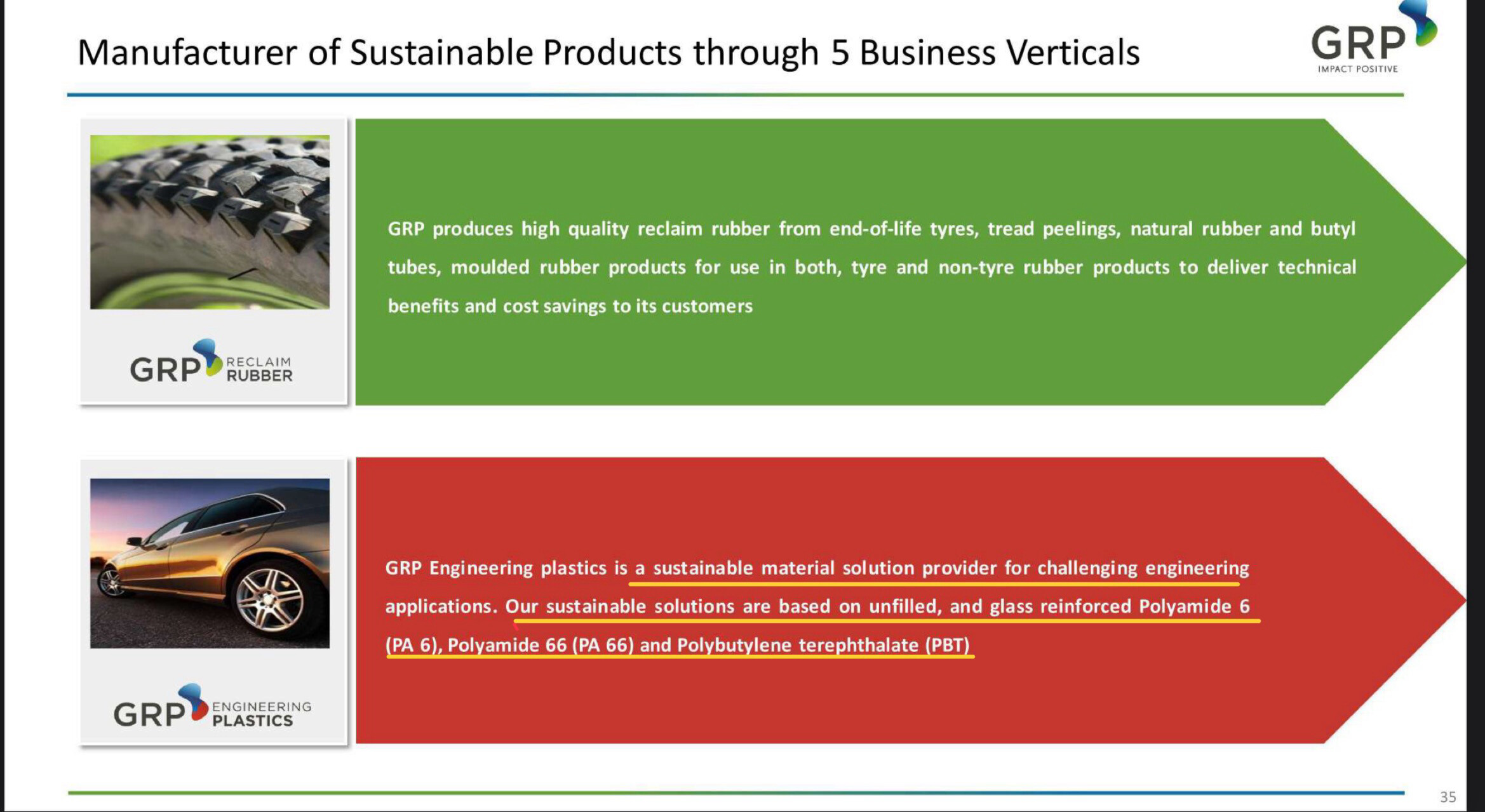

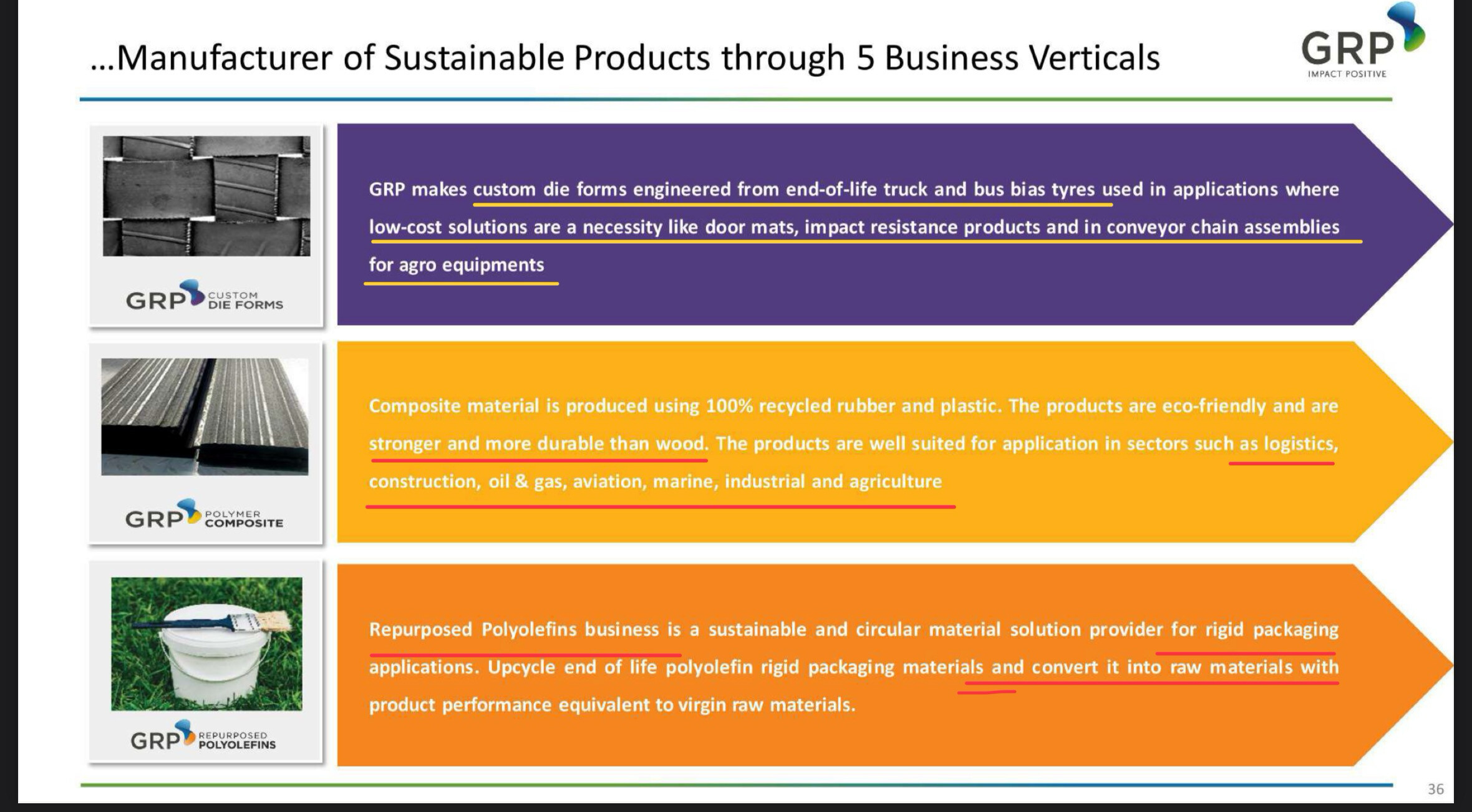

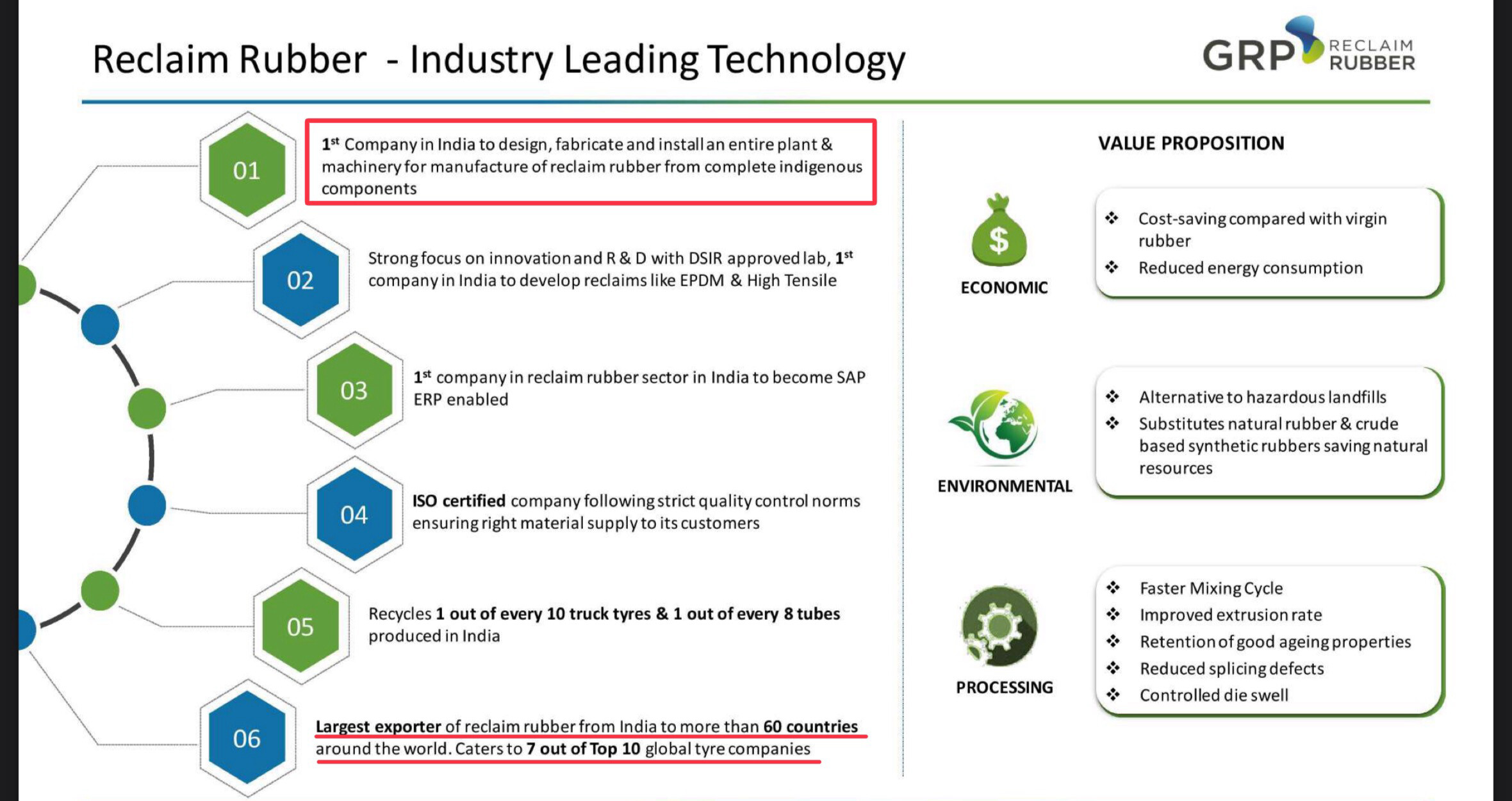

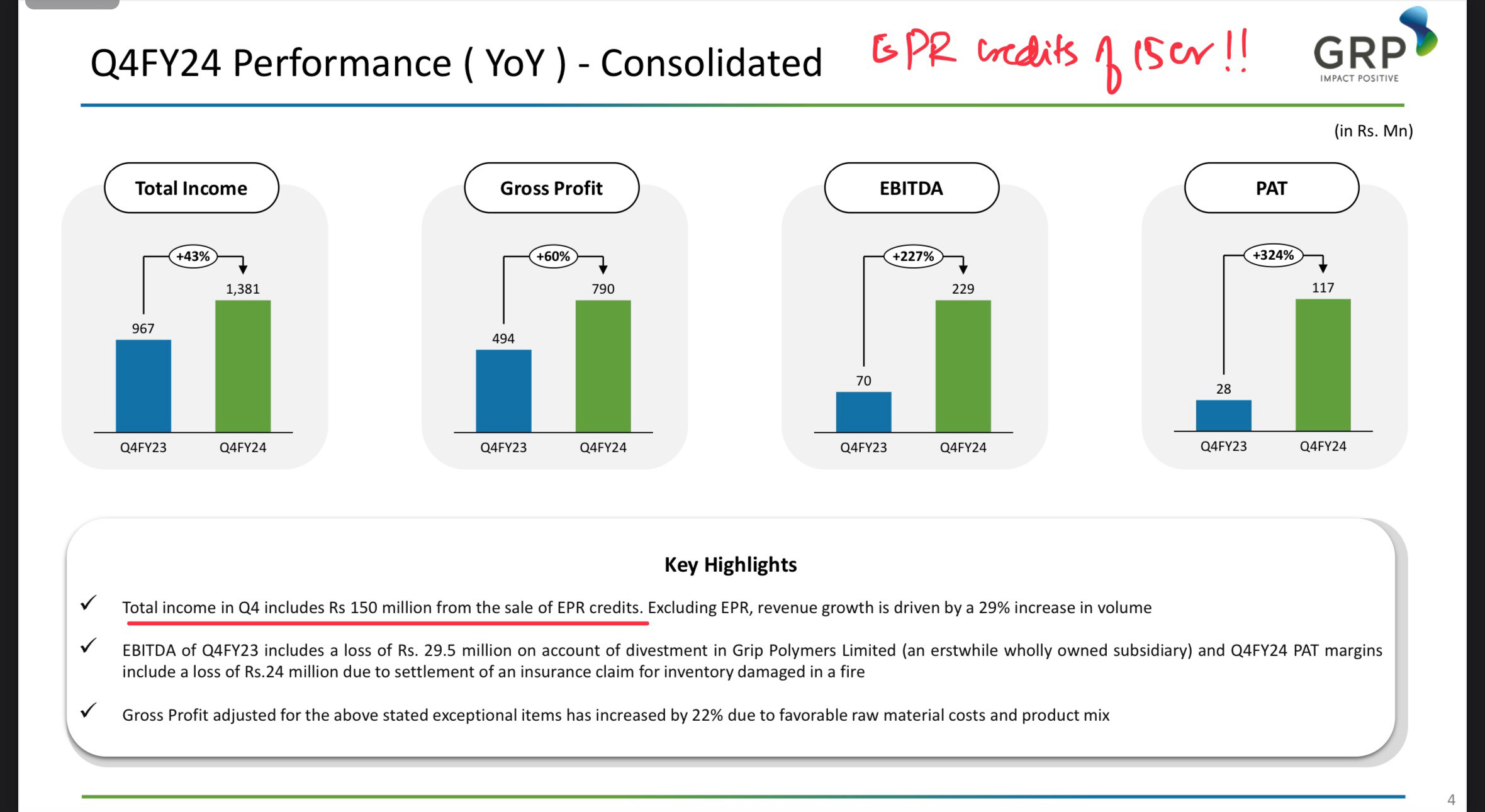

Gujarat Reclaim Rubber (now GRP Ltd) (27-06-2024)

This stock delivered 3x of their usual PAT avg in Q4 . This is what piqued my interest.

.

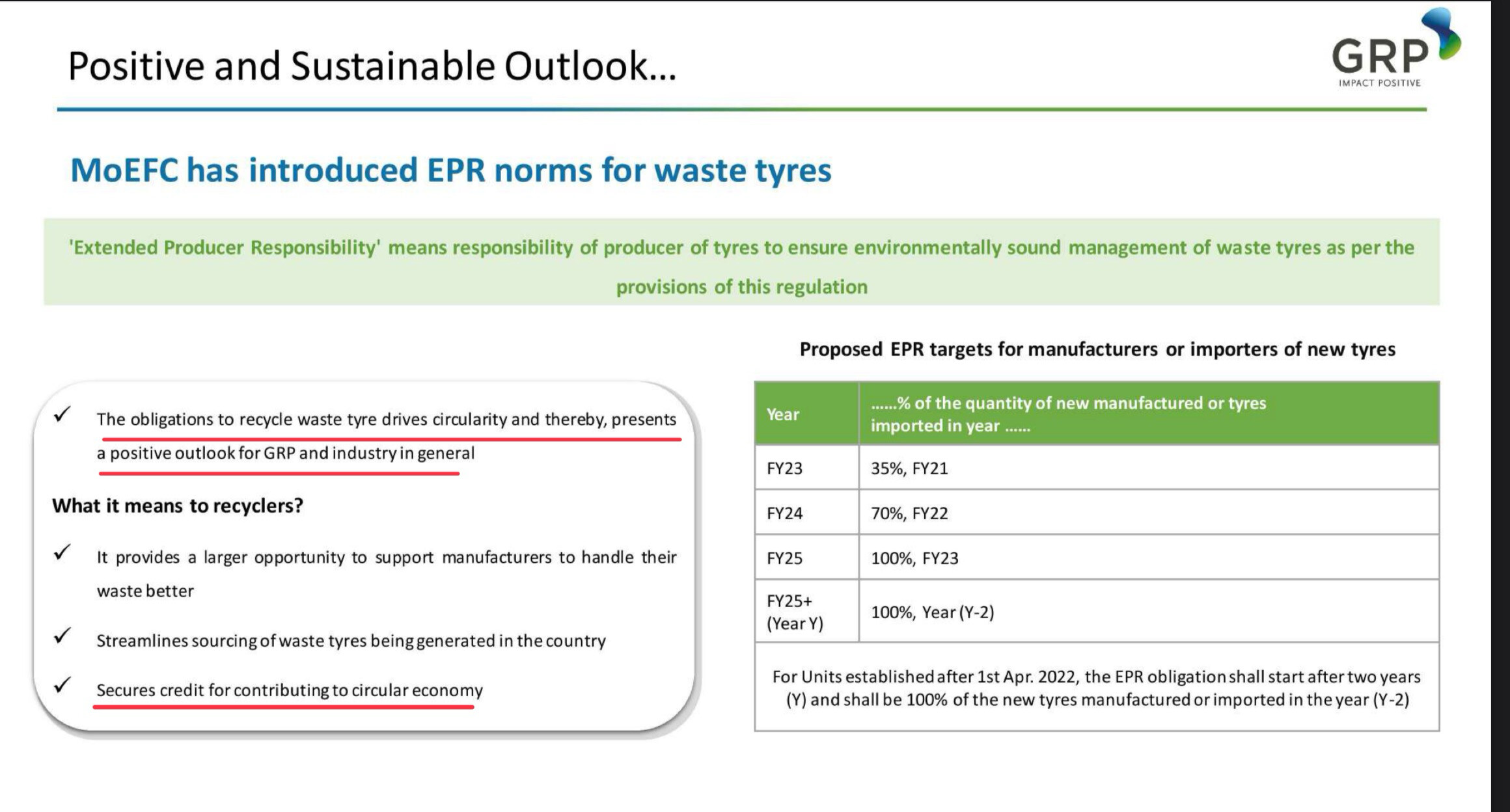

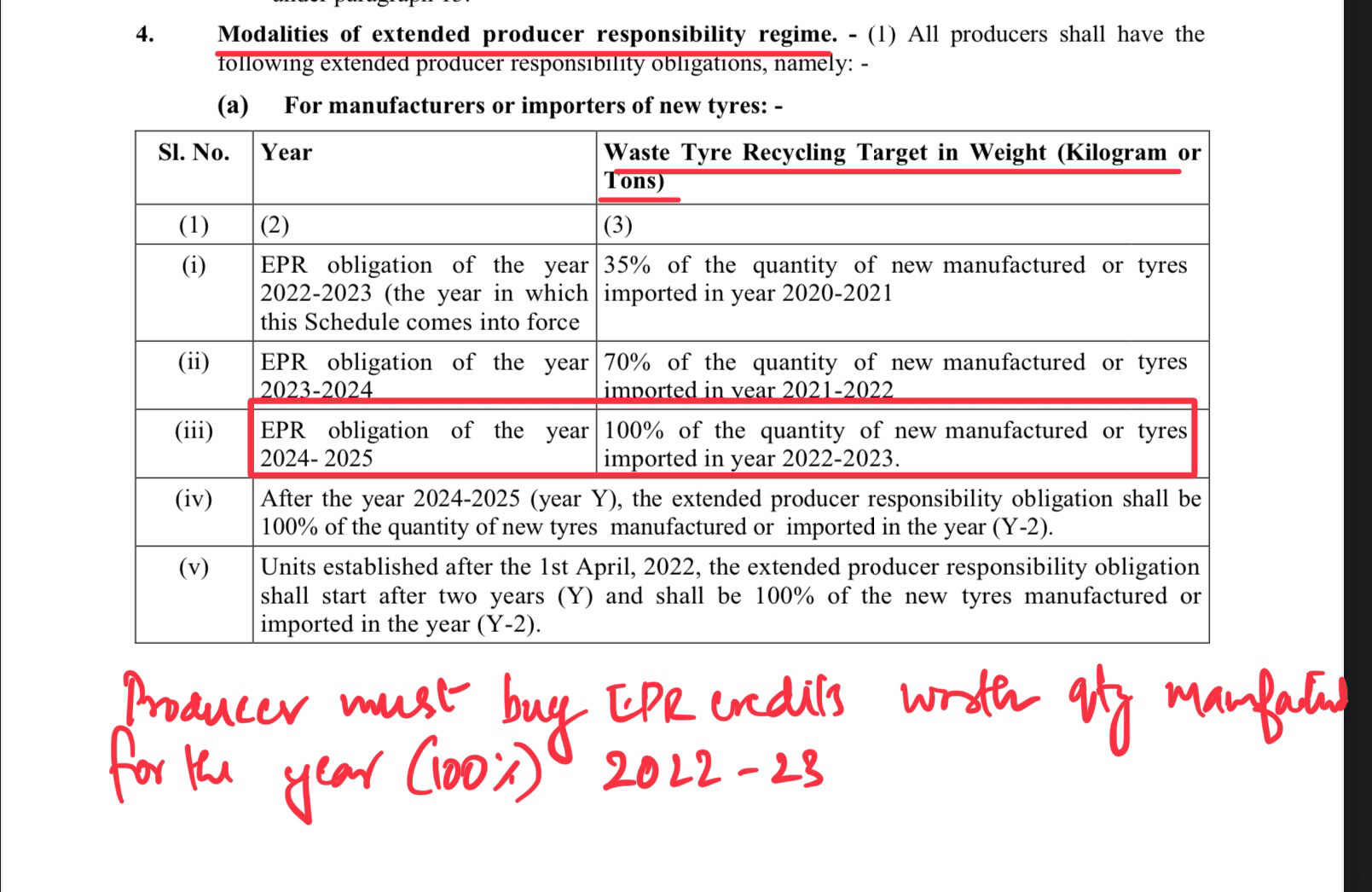

Part of the reason for this bumper performance is due to EPR (Extended Producer Responsibility). I believe this has the potential to change the fortunes of this once loved now forgotten company.

Back of the Envelope Calculation on the EPR credits for GRP:

Current Capacity: 72000 MT

Capacity Utilization : 85%

Production : 60,000 MT

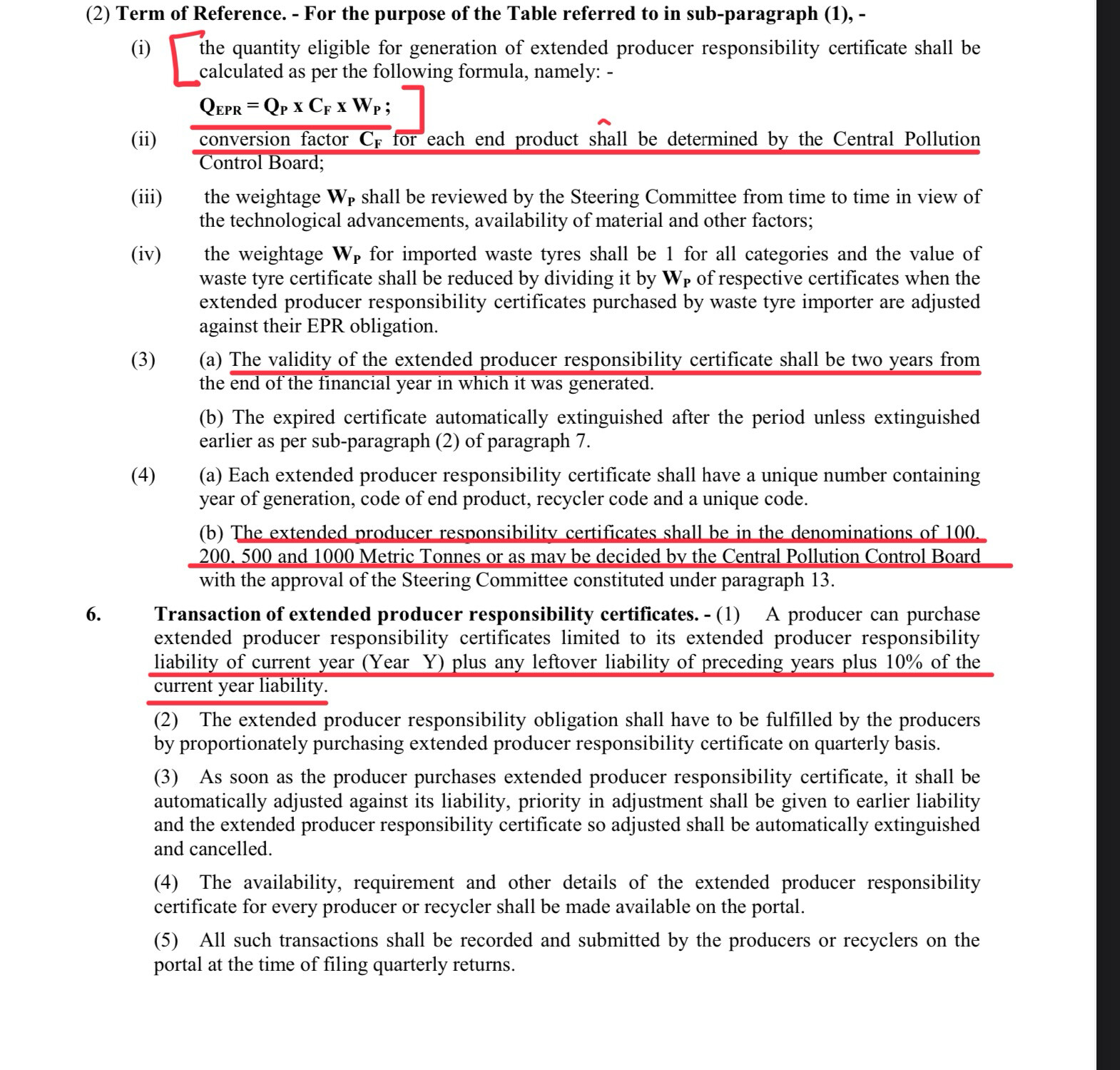

Q(EPR) = Q(P)x C(P) x W(P) = 60000x .78x 1.3 ~ 60000 certificates/ 600 certificates of 100 MT denomination.

In Q4 FY24 GRP has realised 15 Cr from EPR credits (As per management only partial credits realised for FY 22-23 ).

Assuming 60% of the credits are realised for FY 23 we can arrive at approx Rs 4000/MT as addnl realisation due to EPR credit .

The beauty of this is that this amount directly flows into the the EBITDA and boosting the margins as evident from Q4 .

P.S : Realisation for EPR credit is negotiated one on one with the tyre manufactures and this value is bound to vary depending on the demand and supply. However since GRP has several years long relationship with major tyre manufactures they have a natural advantage.

Brief Note on the company :

Concall Notes :

-

EPR for tyres started after 3 years of extensive work including the govt. /CPCB/ Tyre brands etc.

-

Partially realised EPR credits for FY 22-23 . Company has generated credits in CPCB portal for FY 22-23, 23-24 and 24-25 .

-

Global brand owners are also focused on the sustainability initiatives of the recyclers. GRP is the first Indian company to be certified for ISCC- ” International Sustainability and Carbon certification “

-

100% subsidiary launched for repurpose Polyolefins business . Applications in paint and Lubricant sector.

-

Successful approval of Engineering plastics business by a European major , paving the way for entry into major auto OEMs.

-

Successfully commissioned new technology for manufacturing reclaimed rubber.

-

Additional land acquired in Sholapur for crumb rubber plant and venture into down stream recycling.

-

EPR regulations in plastics is getting delayed for implementation , expected in current FY.

-

New range of products in engineering plastics business from ocean plastics. Eg : Fish net waste.

Conclusion:

GRP is positioning itself not as a tyre recycler but as the most important cog in the circular economy .Their entire business is in the ESG domain. With the current tailwinds on environment, recycling etc and with introduction of EPR looks like good times are ahead.

Disc: Invested after Q4 results.

MapMyIndia – The Map Company (27-06-2024)

The new company would be doing consulting business using the data of mapmyindia…

Consulting is a high profit business with no loss potential… I feel that is wrong as this profit should not go to the new unlisted company but rather to mapmyindia…

Sealmatic India Limited (27-06-2024)

Disc: Invested

All fine to be an optimist. However it is not ok to deny your own prior statements.

Rather, since the company is making an honest effort to keep it’s shareholders (particularly the small retail investor), address why your numbers went awry. It is a place of learning, not of denial.

If we find our management to be leading us astray, this is a very bad sign.

I have great faith in this company and it’s ip, it’s concept of the annuity style return of it’s products, the fact that the promoters have deep expertise in it, that they are willing to have regular concalls, answer questions from investors, that they discuss future plans, and have invested in capex. It is not with a little hope that we have invested with them, but denying previous statements begins to make one nervous.

I think it is an appropriate concern that has been brought up in the forum and we, as vulnerable investors, must be alert too. The very best minds were fooled by Enron et al.

@Nimit @rinkupranjan are right to observe this lapse on our behalf.

Sealmatic India Limited (27-06-2024)

Also Mr Balwa said that once the seal is sold they have assured business for the next 20/30 years. How true is that. Once the existing seal is gone will the user should necessarily buy form Sealmatic or they can buy any other seal from other business?