561ea3e7-c630-4106-8a9d-a5e4b05cd7ba(2).pdf (790.2 KB)

Posts in category Value Pickr

Voltamp Transformers (06-11-2024)

There is always an issue of quality of disclosure. I refuse to believe that highly experienced management of Voltamp with long track record of excellent execution will face certain supply chain issues that others are not even acknowledging.

Let’s look at TRIL and Schilchar more closely.

TRIL reported good numbers because of low base effect. Company and stock did nothing for many years till Q2 of last year. Then suddenly there were 3-4 good quarters which makes their quarterly results look super duper. Stock prices and valuations went sky-high in no time. TRIL trades at 10 times sales (voltamp trades at 6 times).

Shilchar shows slightly better execution pedigree (which is to not say much) than TRIL but I can’t figure out for life of me the sudden 2X jump in their operating margin in last 1 year. You can’t have such big divergence between margins between one player and the rest of the sector. And if it’s there it’s not sustainable.

Valuation wise, the less said the better, Shilchair, trading at 15x sales, thanks to and lots of speculation seen in the stock.

In general I am wary of the companies, in tailwind sectors, that suddenly start showing good numbers after several years of average or non performance. Mostly it takes either great luck or magic for such turnaround.

I have seen many cases of book cooking or corporate governance coming to light, crashing stock prices. Look no further than Brightcom which was reporting excellent figures during a time when digital marketing industry was in a duress. Not saying TRIL and Schlchair are up to something but it’s always good to ask questions.

Nitiraj’s Portfolio (06-11-2024)

one simple advice to reduce number of stocks. If all your stocks were to crash by 50%, which stocks would you panic or hate to hold them and which ones would you be rather fine & see it as opportunity to buy more.

Caution: when you do this exercise, be cognizant of the kind of investor hat you are wearing – the short/medium term hat of a momentum investor or sector rotation or triggers for next few quarters or a fundamental long term investor (again value or growth) or a mix…Nothing wrong in any of these strategies but wearing these hats when trimming would land you with a portfolio meant for those specific purpose…

so maybe first exercise before trimming would be knowing yourself as an investor and what kind of portfolio you would want after the trim.

HDFC Life Insurance Company (06-11-2024)

I am referring to HDFC Life Insurance schemes being low innovation. They however do offer good IRR as compared with its peers for Pension Schemes.

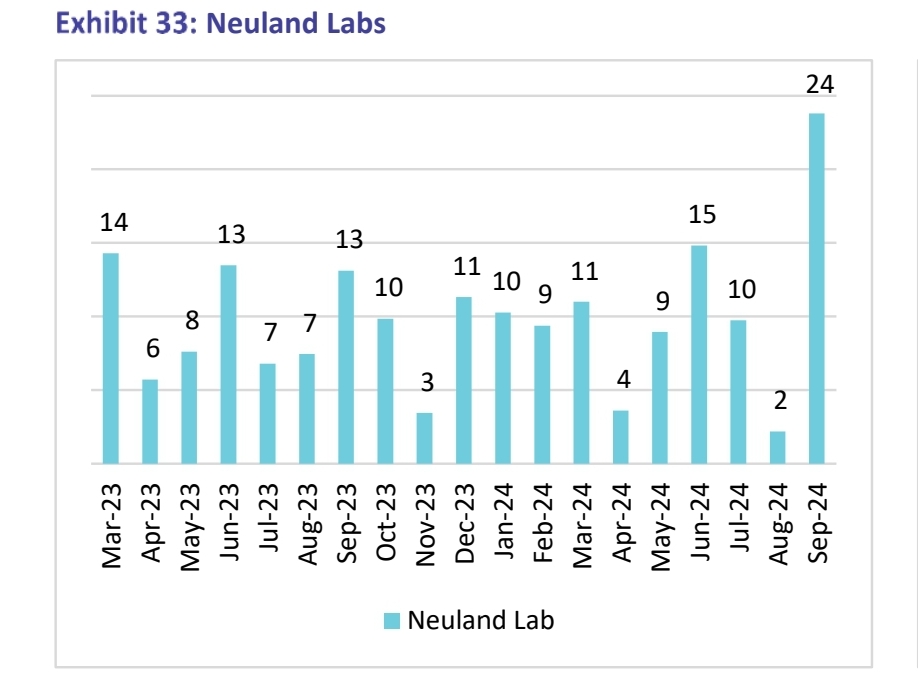

Neuland Laboratories Limited – Transformation towards niche APIs? (06-11-2024)

In the concall, they downgraded their guidance of FY25 from medium growth to flat performance YoY.

Even considering flat guidance YoY, I feel H2 will be better when compared to H1 and even compared to H2FY24 due to dismissal Q2.

In september quarter as per export data they made all time high export it seems but the q2 result was not that good. Maybe as revenue will get realised when shipment is received by client ( export data from Nomura research report)

Dis : Neuland is my top holding.

Stop the Count – US Policy impact on Indian Equities (06-11-2024)

It remains to be seen how much of the promise materializes. One does not take a politician’s words at face value. Besides there will be backlash from EU and other climate conscious countries who are friends with America against Trump’s “Drill baby Drill” (Oil) policies.

Allied Digital Services Ltd (06-11-2024)

Q2FY25 Earnings Conference Call Summary:

Strong Order Wins:

ADSL secured over Rs. 675 crore in new orders and contract renewals during the quarter.

Order across diverse sectors including

- Safe city and smart city initiatives order

- A leading life insurance company in India

- The world’s foremost specialty packaging company

- Global leader in the energy sector

- Public sector enterprise under the Ministry of Power

- India’s Central Bank

- Regulatory Authority in Maharashtra

- Prominent aluminum refinery in Odisha

- The largest bank in the UAE

- Global leader in silicon carbide and gallium nitride technology in the US

Financial Performance

- ADSL reported strong financial results for the quarter, with growth in both revenue and profitability.

- The company’s EBITDA margin was over 11% for the quarter.

- However, there was a slight dip in the margin year-on-year, primarily due to non-recurring expenses, such as an extra provision for ECL and expenses related to the company’s 40th-anniversary celebration.

- ADSL’s cash balance as of September 30, 2024, increased to Rs. 170 crore, up from Rs. 99 crore in September 2023

- The company is improving operational efficiency by reducing debtor days, which have improved from 87 to 72 days year-over-year

Guidance

- ADSL reiterated its guidance of achieving Rs. 1,000 crore in annual revenue in the next six to seven quarters.

- To achieve its goal of reaching a 15% EBITDA margin in the near future

Future Growth Opportunities

Cybersecurity Business

- ADSL sees strong growth opportunities in the cybersecurity space.

- The company is investing in its cybersecurity capabilities and is seeing increasing demand from customers.

Data Center Business

- ADSL is also focused on growing its data center business.

- ADSL is actively pursuing data center opportunities, leveraging its experience building and managing data centers for its smart city projects and pursuing contracts with enterprise customers for data center management and cloud migration services.

- The company is seeing opportunities in both the government and private sectors.

- ADSL is also working to get empaneled with the Ministry of Electronics and Information Technology (MeitY) for data center projects.

- There is big push from government’s on data localization

Key Takeaways

- The earnings call highlighted ADSL’s strong performance and positive outlook.

- ADSL is implementing strategies to improve margins, including focusing on more profitable service offerings, such as app support and AI, and improving operational efficiencies, such as reducing debtor days.

- The company is well-positioned to capitalize on growth opportunities in the cybersecurity and data center markets.

Disclosure: I am having exposure to this counter from long time(20 Rs level). My views can be biased.

Happy Investing,

Karthik

Jindal Drilling – Beneficiary of a sustained offshore upcycle? (06-11-2024)

Very informative and well written thread. Just couple of cents as an industry insider.

We need to distinguish between shallow offshore drilling and deep-water drilling both of which have different ecosystem, economics and technologies.

Deep-water drilling requires floaters which are in tight supply due to higher deep-water drilling activities and hence higher day rates.

Shallow water drilling requires jack up rigs which can be further classified into two categories: 1) Premium 2) Regular

Market for premium jack up rigs seems to be good and supply and demand remain in tight balance. However market for regular jack up rigs is still quite soft due to suspensions of some key contracts globally (e.g. Saudi Arabia) and there is currently an oversupply of rigs in the industry.

So it’s important to take a granular view of an oil field services company’s work pipeline.

Also oil prices will always be a key driver and even term contracts don’t offer much protection if there is drop in oil prices and an operator decides to suspend the drilling/workover activities. Small companies like Jindals won’t go to court to fight their big customers ONGC knowing fully well that they will need them back when market conditions improve. They will have no option but to swallow the bitter pill. That’s why there is an inherent unpredictability to cash flows due to erratic receivables especially if you are dealing with government owned companies.

Again from my last many years of experience, best times to enter the oil and gas sector, in any form, is at the bottom of cycle with favorable risk reward.

That said, I like Jindal Drilling for their execution capability and good management. And if new Trump administration doesn’t move for high tariffs against China and aggressive fracking policies, we might continue to see a quite conducive environment for the offshore rig providers.

Voltamp Transformers (06-11-2024)

Management has informed that there are pressures in sourcing CRGO sheets while the other management such as Shilchar informed that there is no issue sourcing CRGO material. TARIL has not expressed any difficulty in sourcing the material. Voltamp has seen the depressed results in the just ended qtr while TARIL and Shilchar have given bumper results. Voltamp is getting corrected while the other are in upward trend.

Discl: Invested in all the three while pruned some qty in Voltamp and increased exposure in the other two.