@Mudit.Kushalvardhan Very true and also perfectly useless comment, sometimes my post can be difficult to comprehend, it held very true price-wise for 6 months. It still holds true if you read it carefully ![]()

Posts in category Value Pickr

Tinna rubber – recycling a rubbery growth path (16-06-2024)

Smallcap momentum portfolio (16-06-2024)

Hi @visuarchie Sir,

I have checked every date value with Google Finance and Yahoo Finance for each day.

I can confirm all the data is correct from my side and there is 1 issue I found that is causing this changing data from Google Finance.

googleFinance function returns 2 rows but sometimes it returns 3 rows and our index function is picking 2,2, causing the same data to be picked for different dates.

Please find an updated formula which I tried in my sheet.

=INDEX(GOOGLEFINANCE(“NSE:”&C$4,“price”,$B7-1), ROWS(GOOGLEFINANCE(“NSE:”&C$4,“price”,$B7-1)), 2)

I got the same list as yours, but the order is different for some stocks.

Doubt: You have not made price changes for last week, which can cause the order to be different as we are considering 1-year and 6-month data in the standard deviation formula.

I downloaded the data from Bhav copies and verified them for the 3rd and 14th of June.

No difference I found in the price for these 2 dates.

Please check and verify the same.

KEI Industries Ltd – A consistent performer over the last decade (16-06-2024)

- Keeping trailing stop loss at 15% from 52 week high( or recent high) makes more sense, so your gains doesnt wipe out if stock price starts its downward journey furiously.

- 10 week EMA will be too early to exit. Stan weinstein suggest 30 week EMA, but our entry itself is at very high level or stock price is hovering 30% or 40% above its 30 week EMA, then its too much.

- V-STOP ,i am unsure of, as its derived indicator, if you are already following price and volume, you are anyways dealing with direct data, i suppose.

- Taking out capital and leaving profit to compound , is a psychology bias of treating your own capital and profit differently. Thats a wrong way of looking at money. If my capital is 1 crore and it gets eroded by 30% , I am supposed to be more sad while if my profit of 1 cr getting eroded by same amount should not make me sad as that money is not mine, its market money. This thinking itself has a big flaw. I consider all money, whether my own money or my profit , same and treat then with same attitude. All is my money whether my initial capital or profit. I ought to protect my all money at any cost.

KEI Industries Ltd – A consistent performer over the last decade (16-06-2024)

Hi

There is no fixed Rule for this.

1.Some people put trailing stoploss ( say 10-15 percent from 52 week high)

-

Some follow 10 week ema

-

Some follow Vstop- the intervel is tighned to 2, 1.5 like that

-

Some people take away their investment and leave the remaining like free shares ( as ling as company is growing). There are people who made 100’baggers like this by leaving the free shares like this for years together

So in nut shell, it all depends on ones risk appetite etc

KEI Industries Ltd – A consistent performer over the last decade (16-06-2024)

Hi

There is no fixed Rule for this.

1.Some people put trailing stoploss ( say 10-15 percent from 52 week high)

2. Some follow 10 week ema

3. Some follow Vstop- the intervel is tighned to 2, 1.5 like that

4. Some people take away their investment and leave the remaining like free shares ( as ling as company is growing). There are people who made 100’baggers like this by leaving the free shares like this for years together

So in nut shell, it all depends on ones risk appetite etc

Anshul’s investing journey (15-06-2024)

Hi Anshul, Can you help me with your rationale for investing for

Max Estate – based on Mcap to presales, what is your POV for the next 2-3 years of growth?

Anshul’s investing journey (15-06-2024)

Hi Anshul, Can you help me with your rationale for investing for

Max Estate – based on Mcap to presales, what is your POV for the next 2-3 years of growth?

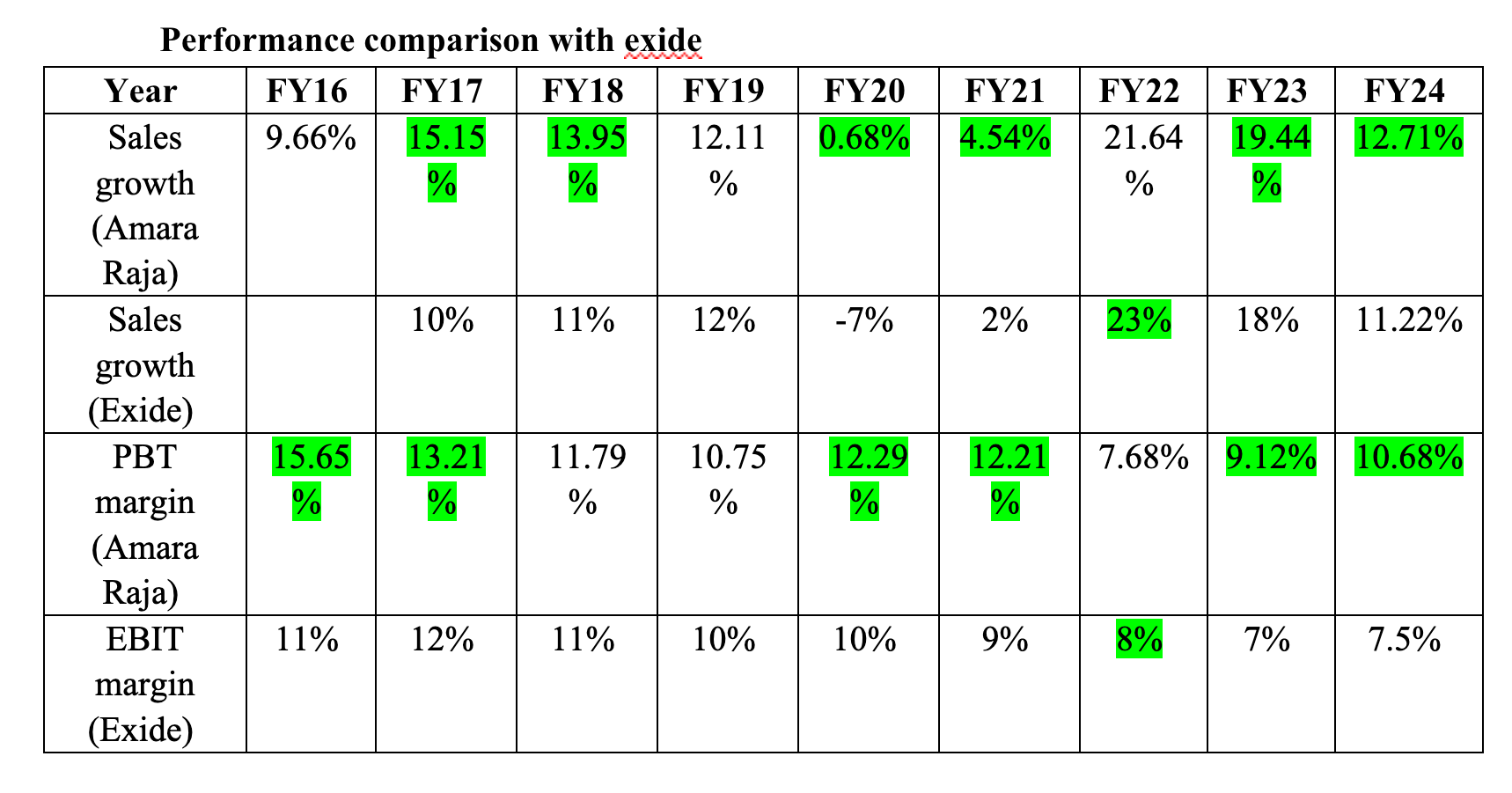

Amara Raja Energy & Mobility Limited: Powering Ahead (15-06-2024)

Amara came with good results with sales growing by 19.5% and EPS by 50%. They continue doing better than Exide. Concall notes below

FY24Q4

-

Lead acid battery : 16% YOY volume growth domestic + 30% exports

-

4-W volumes : OEM: 2%, after-market: 15%

-

2-W volumes : OEM: 15%, after-market: 18-19%

-

Industrial volumes : growth of 5-6%

-

Exports grew by 19% in FY24

-

Export growth is driven by new markets (USA/Africa) + APAC + Middle east. Ranked #1 in UAE and #2 in GCC

-

Made international inroads on UPS products in existing geographies in Southeast Asia and Middle East, and in Europe and North America

-

Trading revenue of 10-11%

-

-

New energy business :

-

116 cr. (vs 148 cr. in Q3FY24 and 88 cr. in Q4FY23)

-

FY24: 522 cr. (vs 249 cr. in FY23; 110% growth)

-

Batteries: 80%, Chargers: 20%

-

Invested 650 cr. so far

-

Commenced 2-W battery packs

-

Looking for partner with technology + R&D pipeline + reliable supply chain

-

Have submitted PLI application

-

Considering asset turns of 1.3-1.4x and 10-11% EBITDA margins, can get ROE of 12-15% once they reach 10-11 Gwh

-

Expect commercialization of 2Gwh line by end of FY26 (cost ~1500 cr.)

-

-

Lubricant : 25 cr. in Q4. Targeting 150 cr. in FY25 (same margins as lead acid). Reflected in standalone numbers

-

Related party mergers : Companies selling significant quantities to the listed entity has been merged or acquired. There is a construction company that will not be merged as majority of their sales comes from outside. An electronic manufacturing company providing home UPS systems going into Amaron Power Zone won’t be merged as its not seen as core

-

Distribution increased to 550+ franchisees and 115,000+ retailers

-

Battery recycling plant (150,000 MTPA capacity) – 80% completed, expect commercialization in Q2/Q3FY25. Consume 3 lakh tonnes of lead per annum with 70-75% coming from recycled sources. The plant will recycle both lead and plastic. Expect 2-3% increase in gross margins and 0.5-0.7% increase in EBITDA margins

-

Tubular plant (1mn+ battery capacity) should commercialize by Q4FY25

-

20 cr. one-time expenses due to stamp duty payments for merger with plastic division

-

FY24 capex: 800 cr.

-

FY25 capex: 1500 cr. (300-400 cr. lead acid + 1000-1100 cr. new energy)

Disclosure: Invested (position size here, sold shares in last-30 days)

Amara Raja Energy & Mobility Limited: Powering Ahead (15-06-2024)

Amara came with good results with sales growing by 19.5% and EPS by 50%. They continue doing better than Exide. Concall notes below

FY24Q4

-

Lead acid battery : 16% YOY volume growth domestic + 30% exports

-

4-W volumes : OEM: 2%, after-market: 15%

-

2-W volumes : OEM: 15%, after-market: 18-19%

-

Industrial volumes : growth of 5-6%

-

Exports grew by 19% in FY24

-

Export growth is driven by new markets (USA/Africa) + APAC + Middle east. Ranked #1 in UAE and #2 in GCC

-

Made international inroads on UPS products in existing geographies in Southeast Asia and Middle East, and in Europe and North America

-

Trading revenue of 10-11%

-

-

New energy business :

-

116 cr. (vs 148 cr. in Q3FY24 and 88 cr. in Q4FY23)

-

FY24: 522 cr. (vs 249 cr. in FY23; 110% growth)

-

Batteries: 80%, Chargers: 20%

-

Invested 650 cr. so far

-

Commenced 2-W battery packs

-

Looking for partner with technology + R&D pipeline + reliable supply chain

-

Have submitted PLI application

-

Considering asset turns of 1.3-1.4x and 10-11% EBITDA margins, can get ROE of 12-15% once they reach 10-11 Gwh

-

Expect commercialization of 2Gwh line by end of FY26 (cost ~1500 cr.)

-

-

Lubricant : 25 cr. in Q4. Targeting 150 cr. in FY25 (same margins as lead acid). Reflected in standalone numbers

-

Related party mergers : Companies selling significant quantities to the listed entity has been merged or acquired. There is a construction company that will not be merged as majority of their sales comes from outside. An electronic manufacturing company providing home UPS systems going into Amaron Power Zone won’t be merged as its not seen as core

-

Distribution increased to 550+ franchisees and 115,000+ retailers

-

Battery recycling plant (150,000 MTPA capacity) – 80% completed, expect commercialization in Q2/Q3FY25. Consume 3 lakh tonnes of lead per annum with 70-75% coming from recycled sources. The plant will recycle both lead and plastic. Expect 2-3% increase in gross margins and 0.5-0.7% increase in EBITDA margins

-

Tubular plant (1mn+ battery capacity) should commercialize by Q4FY25

-

20 cr. one-time expenses due to stamp duty payments for merger with plastic division

-

FY24 capex: 800 cr.

-

FY25 capex: 1500 cr. (300-400 cr. lead acid + 1000-1100 cr. new energy)

Disclosure: Invested (position size here, sold shares in last-30 days)

Tinna rubber – recycling a rubbery growth path (15-06-2024)

@vikas_sinha , After you said that its overvalued, its been 7-bagger. Valuations are truly very difficult to comprehend ??