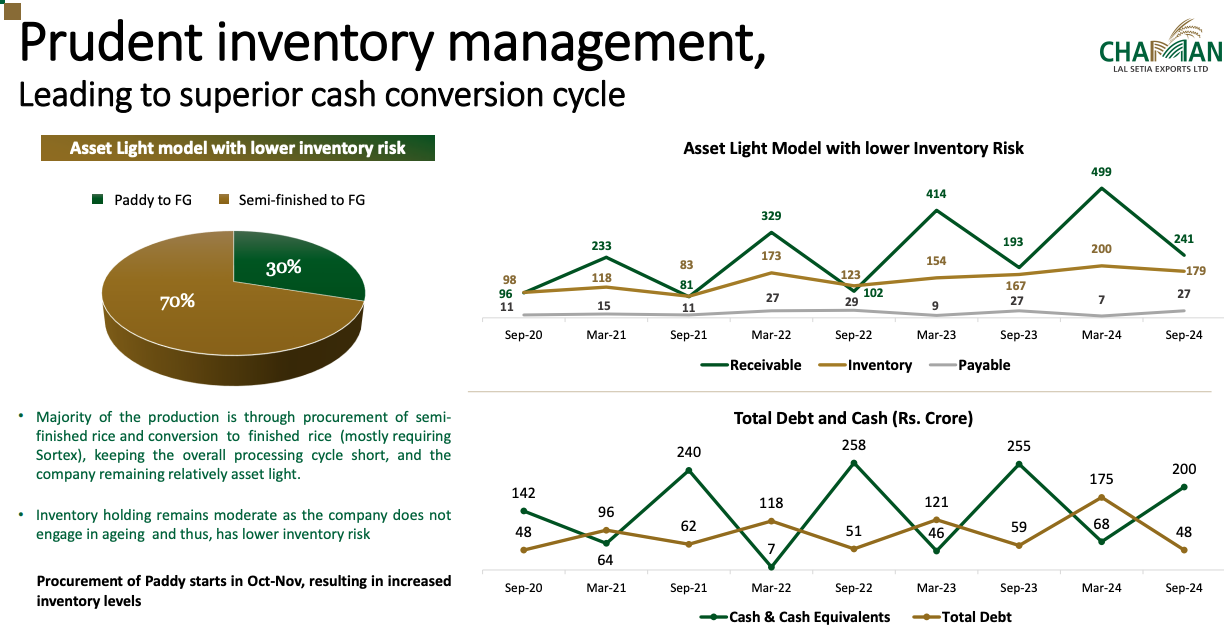

ChamanLal also doesn’t engage in ageing. Lower inventory risk vs LT foods or KRBL

ChamanLal also doesn’t engage in ageing. Lower inventory risk vs LT foods or KRBL

Sorry I thought this was a google review. My bad.

@BuyRightSitTight I also found the management’s responses during the conference call very evasive – be it on capex plans or growth. It seemed as if they were trying to hide something.

Interestingly enough, in the latest concall, management was not ready to give any indication about their capex plans for the next couple of years, in spite of persistent questioning by the analyst from Lucky Investments. I quote:

“So we have no upper limits in our mind with regard to how the growth block should grow. It

completely is driven by the demand. So we are able to like set up our deployment in a way that

like we are prepared for large capacity expansion.

But obviously, we keep building the capacity as the demand keeps coming in and as the

customers keep getting signed up onto our platform. So based on that velocity, we keep on

building the infrastructure. Now, obviously, there is some sense to this fundraise.”

I understand being ambitious in wanting to capture as much of the demand you can, but in business you do plan your capex, fund raising, etc couple of years in advance right? Can’t be open ended! I found this part of the call interesting and perhaps a bit strange.

That’s what they said in 2000 for Cisco

Good growth from past year, what resulted in such double digit growth?

Results view:

These results reflect a company in transition, and how effectively Kirloskar executes its restructuring will significantly impact corporate health.

Positive progress in debt reduction and asset monetization will fuel the turnaround, while any setbacks could derail the process.

I see resilience with strategic restructuring efforts, and the future depends heavily on successful asset monetization, liability management, and cost controls. Legacy business and decades of experience should bring them increases in order inflow.

Potential Q3/Q4 candidate. Very high risk. If it performs, then the next few years belong to KECL.

The dip at 1pm offered a good opportunity, and today, it’s become my largest holding.

Will hold. Will wait. May rejoice.

Thank you for your perspective!

In this sector, companies specialize in a specific niche (e.g. a subdomain in a sector) or cater to a specific clientele. E.g. GLG is stronger in public market investors globally whereas the companies like Infollion drive most of their business through management consultants.

Fair point. However, how does specialisation get built? IMHO, it gets built by the expert network you build for that domain/sub domain/client vertical and the knowledge base that gets built over time by the experts and the consultations. If the experts decide to go with GLG rather than Infollion (for quality of clients, pay, whatever) over time the expert network and consequent the knowledge base gets built at the competitor instead, right?

However, its believed that this is not their India business growth, rather outsourcing of services from foreign markets to India.

By ‘outsourcing’ did you mean getting their overseas clients’ needs met by experts in India?

Annual Report 2023-2024

My view is that …As long as demand tail wind exists , even basic infrastructure provider will grow at rapid pace and returns will justify capex as margin profile is way way superior to cost of capex . As of now looks like demand shall stay for long in India considering data generation and on the go analytics trends