(post deleted by author)

Posts in category Value Pickr

Agarwal Industrial Corporation Ltd – Profitable Microcap with high growth potential in infrastructure space (11-06-2024)

Agarwal is such a simple thesis.

Consistent demand for bitumen → consistent growth + increasing margins due to own vessels (This has been playing out for last 5 years and should continue to play out)

There’s lack of any big risk factor apart from execution risk.

All they have to is keep on prudently adding logistics assets and ensure product avaliability.

A consistent compounder.

DISCLOSURE: INVESTED (2ND highest allocation in terms of cost in portfolio)

Jyoti CNC – And the Stallions it bets on (11-06-2024)

(post deleted by author)

Jyoti CNC – And the Stallions it bets on (11-06-2024)

There is an existing thread on the same.

Regards,

Raj

Shankara Build Pro – Building Materials Organised Retail (11-06-2024)

Can someone comment what is current status of demerger and approx timeline for completion (as it was announced in dec23) , also record date for eligibility of shareholding for demerger is yet to be announced right ?

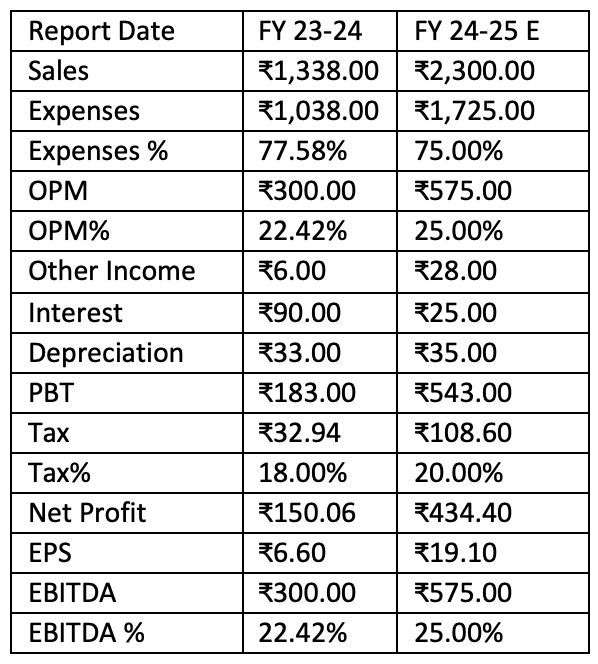

Agarwal Industrial Corporation Ltd – Profitable Microcap with high growth potential in infrastructure space (11-06-2024)

Q4FY24:

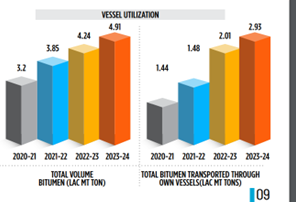

• FY24 Volumes: 4,90,813 MTs vs 4,23,925 MTs (15.78% growth)

•

•

• Company has plans to enter into the Bitumen market in North region of India, to increase its customer base and revenue

CONCALL NOTES:

• Our volume target for FY ’25 is set at 6 lakh metric tons, aiming for a 20% year-on-year increase. So we expect some increase of around 15% to 20% in terms of revenue.

• With capacity constraints in India for bitumen and AICL being the only integrated player in the private sector for bitumen, we have been able to increase our market share.

• India saw a 6% increase in bitumen consumption to nearly 9 million metric tons.

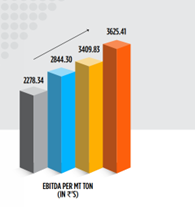

• Currently, EBITDA per metric ton is around INR3.625 which we expected to increase to INR3,800/3900 per metric ton, reflecting our ongoing efforts to enhance profitability.

• Our economies of scale achieved from own feet of bitumen logistics vessels and road transport vehicles enable us to outbid competitors, secure tenders and ensure high standards of supply and service to our customers.

• Targeting 65-70% volume through own vessels (60% this year) (25-35% growth)

• Red Sea is not a problem for us because we are not going towards that side. We are coming from the Gulf countries to India, where we do not fall in between Red Sea.

• BITUMEN REALIZATION DETAILS: The total realization for the entire year has been comparatively low. Last year, the total realization was around 42,000, which this year it is around 36,800. We have lost nearly about INR300 to INR400 crores of turnover due to the price fluctuations.

Realization for this year should be than FY24.

• So ultimately our dependency on third party will stay till the time we have in house capacity of around or more than 2 lakh tons.

• COMPETITIVE CHALLENGES: Challenges we don’t see a great challenge because the company is well positioned in terms of locations and the logistics advantage that we have. I don’t think any other player in the entire Indian state is having the setup that we have already built in the last few years. We just have to turn around the throughput from the storage tanks or the storage manufacturing capacities that the company is having. So, we don’t see a very good or much challenge from the market.

• We have always been focusing on forward and backward integration. So, in the coming future, maybe the company may produce bitumen on its own as well.

• Debt is always cheaper than equity. If there is any plan for the company to add more vessels in terms of capex, the company will not dilute.

Jyoti CNC – And the Stallions it bets on (11-06-2024)

Jyoti CNC Automation Ltd (updated as of 24th May/24)

Company

- Jyoti CNC Automation Ltd, est. 1989, currently operates with two manufacturing facilities in Rajkot (Annual capacity of 4400 machines p.a.) and one in Strasbourg, France (121 p.a.).

- Offering one of the most diverse CNC portfolios in the country, its products include CNC Turning Centers, CNC Turn Mill Centers, CNC Vertical Machining Centers (VMCs), CNC Horizontal Machining Centers (HMCs), simultaneous 3-axis and 5-axis CNC Machining Centers, as well as multi-tasking machines.

- The end users are Defense, Automobile, Electronics & Aerospace co’s.

- The company’s clientele includes prominent organizations such as the Indian Space Applications Center–ISRO, BrahMos Aerospace Thiruvananthapuram Limited, Turkish Aerospace, Uniparts India Limited, AVTEC Limited, Tata Advances System Limited, Tata Sikorsky Aerospace Limited, Bharat Forge Limited, C.R.I. Pumps Private Limited, Kalyani Technoforge Limited, Shakti Pumps (India) Limited, and Bosch Limited. [clientele]

- 3rd largest in india at 10% market share at 12th largest globally with 0.4% share. (as of 2023 & 2022 respectively)

- 2,538,822 sq. meter manufacturing facilities in Rajkot, India and Strasbourg, France.

- Acquisition of Huron Graffenstaden in 2007. This also indicates co’s long term approach and its ability to prepare for future dynamics. (as the acq. aided Jyoti to enter into Central Europe market and gain insights into 5-axis machines which caters to defence and aerospace)

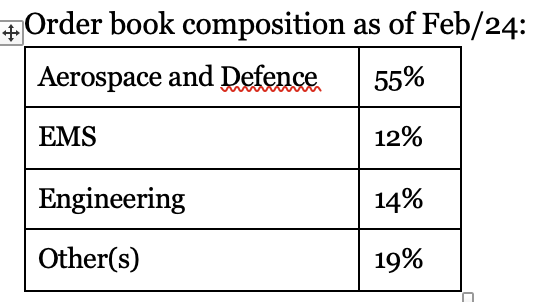

- Order book at Rs. 3300Cr as of Feb/24, and delivery of Rs. 3200 is expected to be delivered in next 18 months.

- Estimated base growth rate of CAGR ~20% for next few years for 5-axis CNC’s.

- Capacity increased to 5000 with De-bottlenecking this year.

- To be increased to 6000 by next FY.

- Vertically integrated; with their own foundry, machining facilities, sheet metal, robotic, welding and paints shops.

- Around 140+ engineers dedicated solely on R&D.

- Direct sales and marketing in case of Indian market.

- IPO proceeds worth of Rs. 475Cr used to pay off debt. (Debt/Equity @ 0.22). Reduced interest cost upto 55-60 Cr.

- Planning to go debt free in next 2-3 years.

- Inventory turnover to decrease from 300 to 210-220 days by 2024 and 170 by 2025.

- About 20-25% price competitive than ones that are imported.

- Focus on gaining market share through import substitution.

- N0. Of machines manufactured in FY23-24 @ 3495 units. (indicates a capacity utilization at ~80%)

- Closing Order Book of ₹3438 Cr.

- Expecting INR 1,500 to INR 2,000 crores of orders in FY’25.

Industry

-

India consumed $3 Billion worth of CNC machines, whereas global consumption is around $80 Billion annually.

-

Of which 65% is imported and 35% manufactured domestically.

-

Majority of imports from Germany (around 30% of global output from Central Europe) and Japan.

-

Industry divided into Metal Cutting (85%) and Metal Forming (15%).

-

Jyoti, focuses on Metal Cutting, and has been awarded “Best Metal Cutting Brand in India” multiple times.

-

Prominent player in 5-axis CNC machine.

-

Offers solutions suited for transitioning towards ‘Industry 4.0’, including their flagship multifunctional solutions package viz. ‘7 th Sense’ – which is geared towards automating sophisticated diagnostic and analytical functions enabling seamless management of productivity, health and tool life of the CNC machine.

-

The 4 Stallions that Jyoti CNC bets on :

- The Global Aerospace and Defence market size is expected to reach as ~US$ 1388 B (@ 8.2% CAGR) by 2030.

- The potential CNC Machine demand for EMS industry in India is over 1,00,000 machines within the span of next 5 years.

- The Electric Car market in India is expected to grow at a 56.0% CAGR during 2024–2030.

- The Indian semiconductor industry is expected to grow at a CAGR of 19.7% from 2022-23 FY to 2026-27 FY.

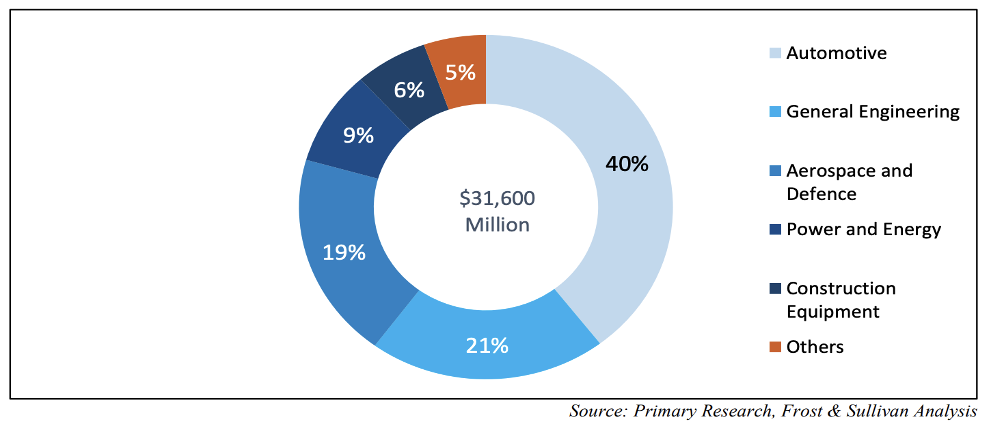

CNC Machining Center Production Share by End User CY22 (%)

Industry 4.0 is changing the CNC machining (excerpt from DRHP)

Industry 4.0 is the latest in industrial revolution and it is changing how CNC machine shops run on a day-to-day basis. With all the smart technology and integrated software available, quicker turnaround times and decreased downtime all result in increased productivity. Data collection and analysis from sensors and other instruments help CNC shops test out new products or study product use. With the application of Industry 4.0, Data helps inform CNC machine shops and manufacturers to make better products and allows business owners to examine their supply chain management process and delegate tedious tasks to the machines.

Industry 4.0 basically refers to a more complex manufacturing setup that includes IloT (Industrial Internet of Things) that monitors and measures manufacturing processes and reacts autonomously to errors. This ability helps CNC machines self-diagnose problems and correct errors in the manufacturing process faster than employees can detect and respond to errors or diagnose the reason for machine malfunction.

For the industry specific example, the medical products industry demands perfection in manufacturing processes because life depends on fail-safe components. CNC machines and Industry 4.0 technology together ensure the production of high-quality components for medical devices. CNC and CAM (Computer Aided Manufacturing) machines are a combination that produces top quality, flawless products, regardless of the industry a manufacturer serves.

Qualitative Factors

- One of the leading CNC machine manufacturing companies globally as well as in India with presence across the CNC metal cutting machinery value chain.

- Well diversified customer base.

- Constant focus on R&D and new product development.

- Vertically integrated.

- Experienced promoter group.

- Provides an extensive range with over 200 variants across 44 series.

Thesis

- The end-user industries are growing at a faster pace.

- Strong order book providing revenue visibility.

- Financial Strength improvement. To be debt free in nest 2-3 years.

- Addition of new customers.

- Focus on EMS rising as the industry is getting groomed.

- Multiple Engines of growth:

- CNC sector to grow at around ~10% CAGR.

- Base growth rate 20% CAGR for 5-axis CNC’s.

- Capturing market share through import substitution on high-end machines.

- Capturing market share in Central Europe through Huron. (turned EBITDA +ve, and expected EBITDA margin of 20% at optimal capacity)

Anti-Thesis

- The growth probably is already priced in, as evident through its current valuation.

- Material cost is a huge chunk of COGS, and can further increase due to underlying raw goods prices.

- Business is highly dependent on skilled workers, and attrition rate was around 25% in 2023 as stated in its DRHP.

- Customers (even the larger ones) don’t usually go forward with long term contracts, and it can take away a huge chunk of revenue if a price competitive player enters in the market.

Disc: Invested. DYODD. Not a Buy/Sell Recommendation.

Shankara Build Pro – Building Materials Organised Retail (11-06-2024)

Would anyone know why Ashish Kacholia and Mukul Agarwal reduced their holding in the company?

@ranvir any idea?

Disc: have a small position

Tinna rubber – recycling a rubbery growth path (11-06-2024)

Insightful video on tyre recycling:

Royal Orchid Hotels – Available at good valuation! (11-06-2024)

The tides have turned for the hotel industry with surge in tourism. Royal Orchid has been regularly adding new properties at key tourist locations like Gangtok, Sakleshpur, Puri etc. Sales from the newly added properties will reflect in top line in some time. In this market I think Royal Orchid is a value pick and can be bought. You will have to be patient but it can easily double in 2 year’s time.

Disclaimer: Invested / Biased.