@samm2211 @UrvilShah acquisition cost for bonus shares is zero. For demergers, the company in the scheme document gives a ratio / percentage as to how you should split your original cost of acquisition between the two shares

Posts in category Value Pickr

Heritage Foods Ltd (10-06-2024)

I disagree with this hypothesis. Attaching a video which I completely resonate with and the reason for which I wouldn’t let go of Heritage or think of it as just a short 5 year story. As long as they keep delivering on their business plan, I’ll retain the company in my portfolio

https://x.com/FundamentalGems/status/1799496350385463337?t=-nkPWpRMUSVJT-OTY8cYLA&s=19

Sundaram Clayton (10-06-2024)

Hi Kandukuri,

Your comments above have been super helpful, so firstly, thank you so much for educating all of us.

I have 2 questions:

- How do I value TVS holding business other than its stake in TVS motors?

Context: today the market cap of TVS motor is ~115k. TVS holding has ~50% stake and then factoring in 50% discount due to holding structure of TVS holding, the market cap that TVS holdings gets due to TVS motors is ~25k, which is where TVS holding is exactly at today. So I want to see how much fuel do we still have in TVS holding?

- What is your perspective on Sundaram Clayton valuation?

Context: I feel it is suppressed because its profit have been taking a huge hit due to non operation of USA factories and fixed cost from them. However this may improve on some years. Also, I think the huge Chennai land they have in the prime area, is worth a lot which they may sell some day. Whatever I am saying here is not with a lot of confidence, so looking for guidance from you as well. Thank you!

Avenue Supermart: a compounding machine? (10-06-2024)

I had also seen popcorns and ice-creams at few DMART stores earlier. But seeing them selling Pizza with it’s volume and scale pleasingly surprised me!

Companies with 20%+ growth guidance for next few years (10-06-2024)

Hi Folks, is there a screener for companies guiding for more than 20% growth in the current and next years?

Avenue Supermart: a compounding machine? (10-06-2024)

its been years here in hadapsar store of Pune city. started with ice cream softy cone, then added branded icecreams and popcorn etc…all at the exit gate of the store. so after shopping, one is exhausted and will look for something quick to eat…so yes it is a good idea as it seems to me.

Avenue Supermart: a compounding machine? (10-06-2024)

I recently visited a DMART store in Bengaluru, which has started selling as well(I don’t know since when they are selling it as I moved in to this area recently).

Pizzas’ cost were really cheap(₹99 – ₹159) and taste was decent. I even saw few people buying multiple Pizzas and taking them home. I think they are selling ~500 orders(not Pizza, but order) per day from that store only. So even if I assume ~₹200 / order, a single store is earning ₹1L / day of revenue. Considering that they just have ~10SKUs(4-5 Pizza, all with same size + 4-5 cold drinks) and very low cost, this was really good to see.

If DMART will scale it to even 25% of their stores, it will add ~₹300 Cr of topline with ~20-30% of net margin without much hassle in next year. This seems like too good to be true to me. Please enlighten me if I’ve wrong assumptions here.

Disclaimer: I have extremely limited understanding of food sector and it’s scaling challenges. People will working experience in this sector can suggest.

Megatherm – Mega Opportunity (10-06-2024)

That $85M is supposed to be the how much the industry will grow by I think, not the entire market size

IDFC First Bank Limited (10-06-2024)

I understand your perspective on the investment in non-lending finance companies, and you make valid points. However, the dynamics of the lending business for banks and NBFCs are somewhat different, and it’s important to consider these distinctions.

One crucial aspect to highlight is the relationship between loan growth and equity dilution due to regulatory requirements for core equity capital. Regulatory capital adequacy norms mandate that every lender must have a certain amount of core net worth invested in their lending activities. This means that if a bank or NBFC generates a ROE of 14-15% and wishes to avoid diluting equity, their growth potential is limited to around 11-12%.

For instance, a bank like IDFC First, which generates an ROE of approximately 11% but aims to grow its loan book by over 20%, has no choice but to continuously dilute its equity. This scenario applies not only to IDFC First Bank but also to other banks and lending NBFCs, including prominent names like Bajaj Finance, ICICI Bank, Axis Bank, SBI, and HDFC Bank.

In my experience, the only financial institution that has managed to avoid this trend was the erstwhile Gruh Finance, which generated an impressive ROE of over 27-28% while maintaining a lower growth rate of 18-20%. This exceptional performance allowed them to grow without the need for frequent equity dilution.

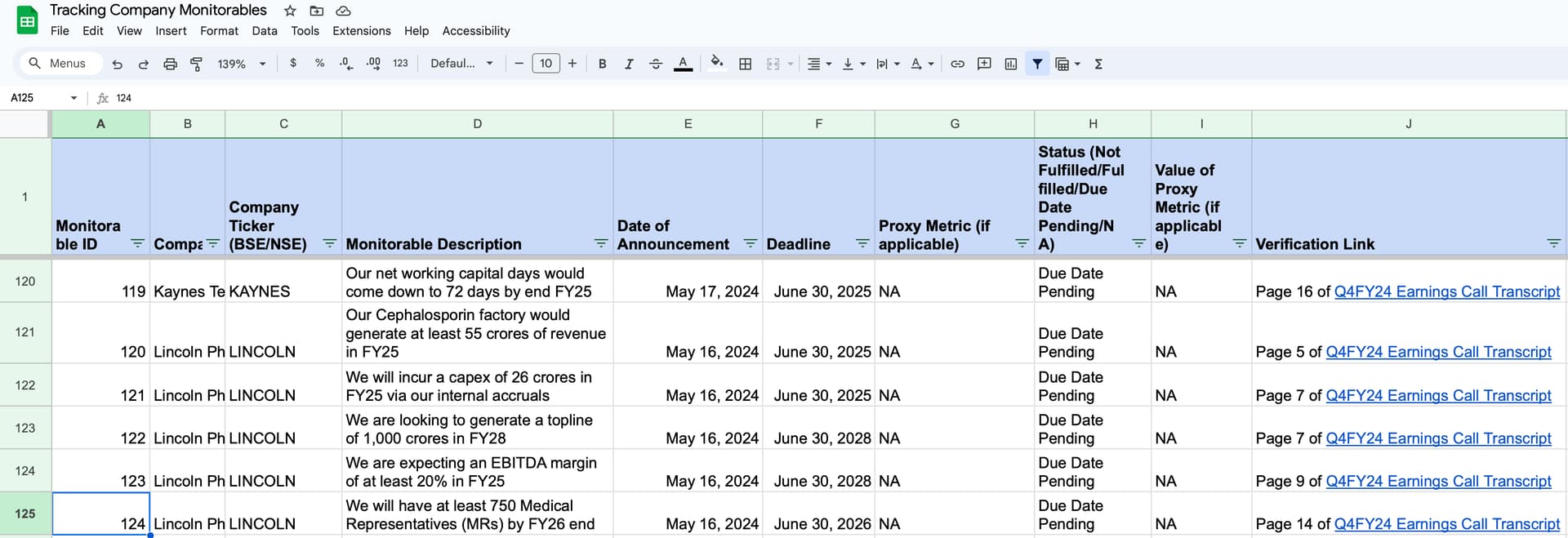

Lincoln Pharma … the next mid-cap pharma in the making …? (10-06-2024)

Hello,

In the below tracker, I have started tracking important company goals for Lincoln Pharmaceuticals.These goals are referred to as ‘monitorables’ in the tracker.I will update this document regularly to reflect the current status of these goals.

Here’s a snapshot of what the tracker includes:

- Company Ticker: For identifying the company

- Monitorable Description: Description of the goal or metric being tracked

- Date of Announcement: When the monitorable was announced

- Deadline: Target date for achieving the monitorable

- Status: Current progress (e.g., Not Fulfilled, Pending)

- Verification Link: A link to see where I got the information about the goal.

I hope this information makes it easier to observe how well companies are progressing towards their stated goals.

Screenshot of the tracker below:

Full tracker attached below:

Tracking Company Monitorables.xlsx (122.2 KB)