Press release on Hard Kill

New Patent sanctioned for TZS (Laser Boresighting)

Press release on Hard Kill

New Patent sanctioned for TZS (Laser Boresighting)

Please read forum guidelines properly before initiating a thread.

https://forum.valuepickr.com/faq

To nurture a vibrant community ValuePickr does not restrict anyone from starting a thread on a stock of his/her choice. Only Caveat is if you are going to introduce a discussion on a stock, we expect you to do your homework and start the thread with some basic info-set, and 1st level analysis such as growth drivers, a few positives & negatives, immediate triggers if any, and enumerate some RISKS. Nothing very heavy is required, but enough to set the tone for 2nd level of discussions.

Thread initiators are usually alerted to edit their post, and make necessary changes before thread is opened up again. So you/colleague and look to edit the post in order to meet prescribed guidelines. We have the responsibility – especially the thread initiator (assumption is he/she is a savvy investor) – to cater to bringing everyone on same page – quickly – if you know what we mean.

You need to add detailed risk analysis.

Grill Splendour Services Limited is a chain of gourmet Bakery and Patisserie spread across Mumbai through 17 retail stores 5 are under franchise model. It has a centralized production facility and multiple corporate clients.

In 2019, they acquired the bakery and confectionary business along with brand Birdy’s Bakery and Patisserie from WAH Restaurants Private Limited.

Co. Engaged in the sale of following broad categories of products:

Cakes & Pastries

Food Sale

Beverages

Desert Sales

Revenue Breakup

B2B Sales – 68%

B2C Sales – 32%

Online- 63%

Retail- 37%

Loan of 25Cr from BRFL to used for acquisition of rights in brands Pizzeria, Roti, China Joe.

To Raise 16 through IPO to used for loan repayment (11 cr), Wc requirement, other.

Promotor holding decreases significantly after the listing

Srinidhi V Rao: Age 52 He has done Diploma in hotel Management. Holding 18% from 25%

Vandana Srinidhi Rao: Age 52 has done Diploma in hotel Management. Holding 18% from 25%

Experience: Both has 30 yrs experience in hospitality sector

Co. revenue per store is only 37 lakh which is very less and some store are not even recovering the rent cost. It has high debt of 14 Cr with Mcap of 38 Cr

Ah i see. Thank you for the explanation

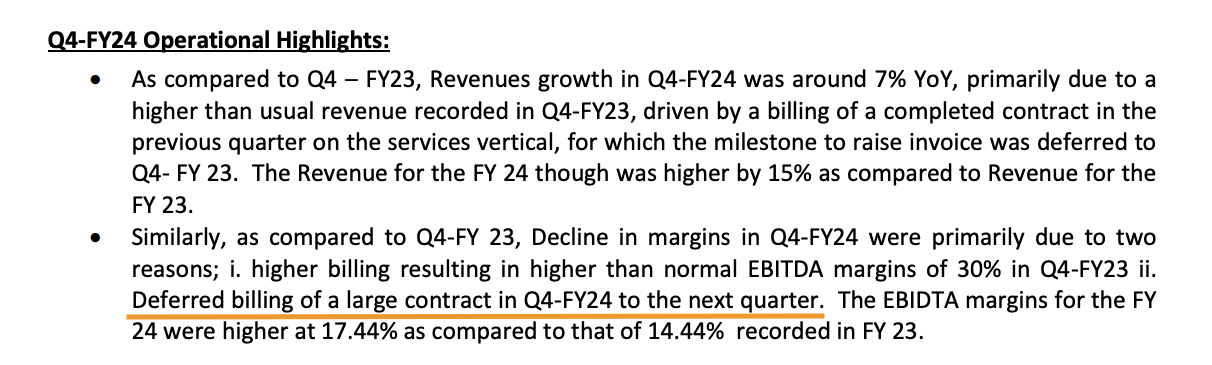

This was indeed the reason. For a company like this, we shouldn’t be comparing quarters but years since they aren’t selling soaps or shampoos but executing large lumpy orders with different revenue recognition modalities by project.

The company came out with first investor presentation yesterday which is quite detailed unlike its ARs. There’s a definite intent here to grow the business and the market cap, with the hiring of high-caliber professional CEO and MDs and giving them hefty options and also hiring Valorem to help investor communications. Disclosures should only get better from here hopefully.

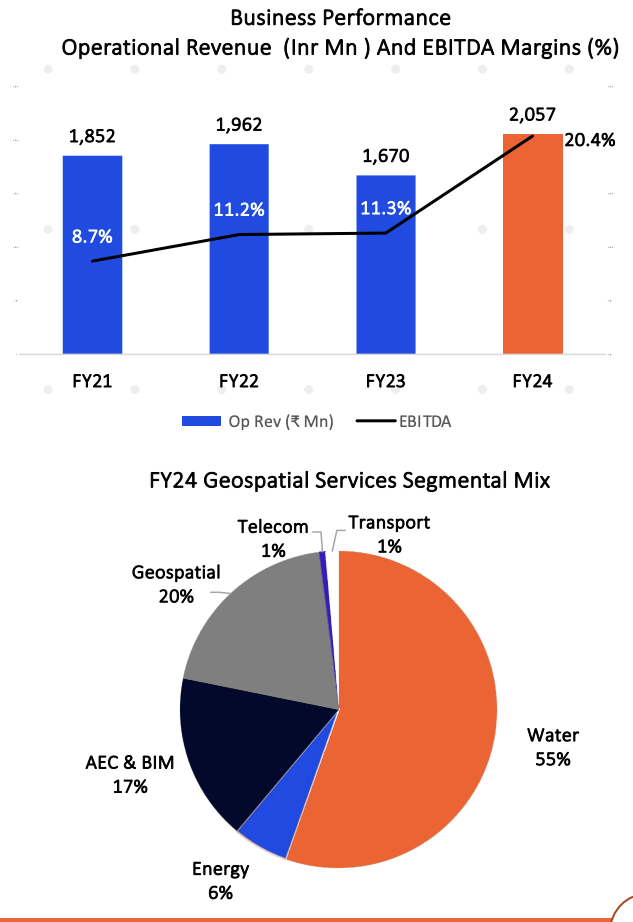

There’s also some very useful information in the PPT like the geospatial segment growth, margins and also segment-wise split-up. The margins in geospatial have gone up substantially in FY24.

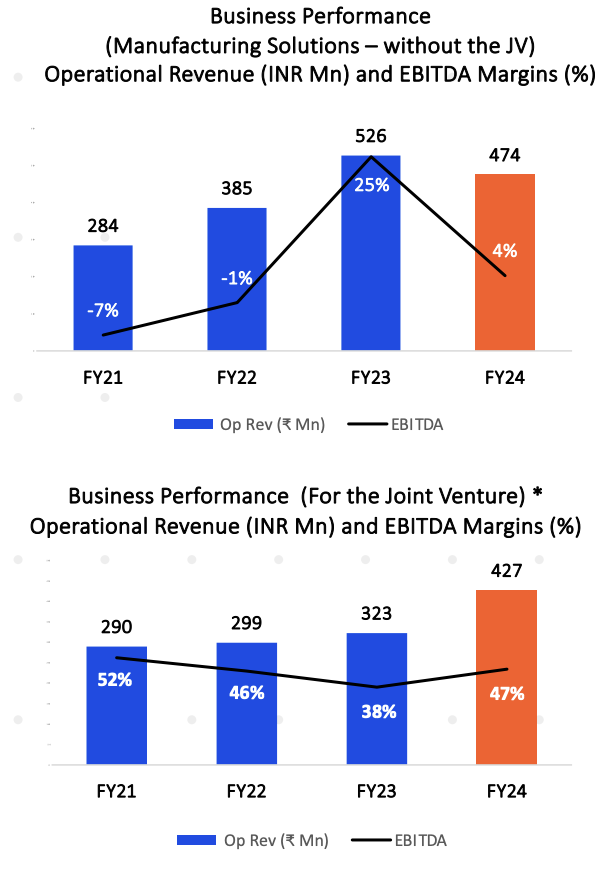

The performance of AllyGrow and AllyGram, their JV with Grammer AG. There’s a severe compression of margins in AllyGrow in FY23 while there’s healthy growth in AllyGram. Not sure if this is due to movement of business from AllyGrow to AllyGram but if its not, then an increase in revenue in FY25 could mean margins coming back in AllyGrow which could be a good kicker on top of geospatial business growth.

The order book position as well is updated. I had mentioned order book was 650 Cr. Looks like it stands at 710 Cr. The deferred large order in Q4 could show up in Q1 or Q2 and hopefully should lead to healthy growth. Overall I don’t see the business performing poorly but on the contrary, could actually be performing quite well.

Taal, Weekly – This is an old position which has been underperforming somewhat. There’s lot of volatility contraction and consolidation within that triangle last 6 months.

There was severe margin contraction in Q3 which led to big selloff post results but the margins are back this quarter back to 27% levels it used to be at.

Disc: Invested in both as disclosed before

Can be positive for this.

[Slide 1 – Time-Technoplast-Monthly-Pick.pdf|attachment]

(upload://4Y1S5sjL64X3UPUz1gy9Vx8eQIg.pdf) (1.1 MB)

If you come here just for fun and only to crib about the company while staying invested in competition, probably your opinion is biased.

No offence. Just want to highlight that you could have offered a comparative snapshot between the two companies instead of just informing the forum that you moved your capital to another and are happy about it.