Q3 numbers are without BSL figures. Q4 results look good, however market is reacting negatively.

Posts in category Value Pickr

Nuvama Wealth Management: Proxy to Affluent India (31-05-2024)

@Mudit.Kushalvardhan I’m not a technical analyst, but as per the stage analysis knowledge that I have it does look like stage 3. I can be completely wrong as well.

Did Nuvama release a Draft Red Herring Prospectus (DRHP)? If so, where is it made available?

Route Mobile – Internet, Mobile & Telecom (31-05-2024)

12 months not 3 years according to this article. 7.7% stake sale in another 1 year is causing this stock hit 52 week low.

“It now holds 82.7% in Route Mobile and has about 12 months, as per Sebi guidelines, to cut its stake down to 75% to ensure the public holding in the company is at least 25%.”

AksharChem (India) (31-05-2024)

Hi Sir, what do you mean by “cyclical stock” ? is it based on price action?

Microcap momentum portfolio (31-05-2024)

I also prefer small caps, because it is there you may find hidden gems. However, as Mr Raval’s illuminating talk shows, that is not easy. Of course, as Deng Xiaoping famously said “It doesn’t matter whether a cat is black or white, as long as it catches mice .” So, even in large caps a momentum stock (like the PSEs were recently) or a beaten down sector may create enormous wealth, but every investor’s fantasy is landing a 10 or even 100 multi-bagger. They are more likely to be found in the small caps, micro or otherwise.

Magic & Miseries of Microcap Investing ft. Atul Raval | Smart Sync Services #investing #stockmarket

Aurion Pro : Yet another IP product company? (31-05-2024)

that’s not how the market/stocks work.

SKM Egg Products – thinking out of the shell (31-05-2024)

I suppose the charts are of Ovobel?

SKM Egg Products – thinking out of the shell (31-05-2024)

So, grateful, this is really exhaustive. ![]()

Solex Energy – High Growth Potential (31-05-2024)

We have existing thread on Solex. Move content there as this thread will be deleted in a day.

Krsnaa Diagnostics – what is the diagnosis? (31-05-2024)

I am very optimistic about this business for following reasons. I am looking for opposing views on my thesis and what’s the downside if we invest in it. (I am already an investor and looking to increase my holding).

The company is cheaply valued compared to all its peers. One of the obvious reasons is return ratios. Both can be seen in the below table.

| Company | Mcap Rs. Cr. | ROCE | ROE | PE | PB | P/Sales | |

|---|---|---|---|---|---|---|---|

| Dr. Lal Pathlabs | 21,861 | 25.2% | 20.4% | 61.1 | 11.8 | 9.8 | |

| Metropolis | 9,873 | 15.4% | 12.3% | 77.2 | 9.0 | 8.2 | |

| Vijaya | 8,317 | 21.6% | 20.0% | 69.1 | 12.7 | 15.2 | |

| Thyrocare | 3,253 | 18.6% | 13.8% | 45.7 | 6.3 | 6.2 | |

| Krsnaa | 1,837 | 10.1% | 7.5% | 31.4 | 2.3 | 3.1 |

Source: Screener

Now the return ratios are poor because the company is new and in high-growth phase. There is huge setup cost for diagnostics centre and income start coming with a lag. So, operating leverage kicks in after 2-3 yrs of operations.

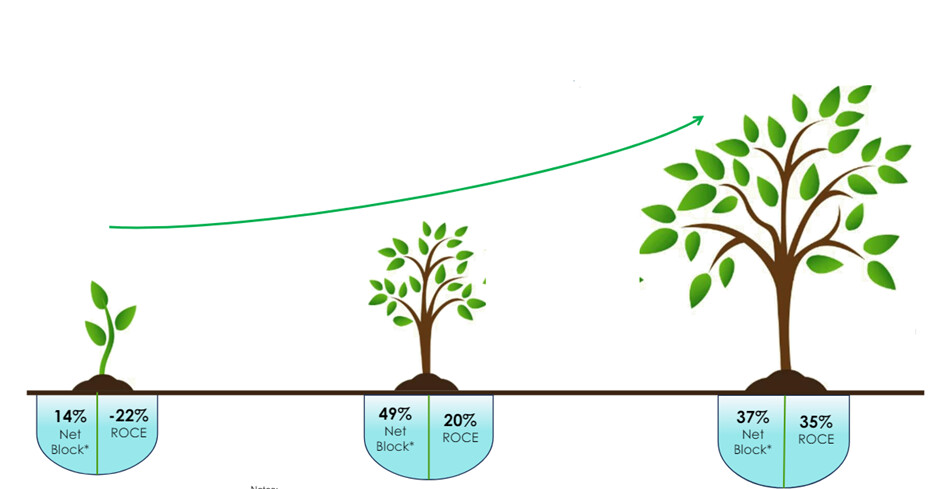

Below is the chart from Q4 FY24 investor presentation. It can be seen only 37% of net block (centres) are mature. They are generating very good ROCE. Once, the newer investments mature, ROCE for them will increase too.

Additionally, the company has huge order bank and they are establishing more centres on an ongoing basis. All the details are available in investor presentation and concall, so not going to flood my post with the same.

They are also venturing into non-PPP segment, i.e. B2B and B2C. I understand this is a competitive segment, but they already have capex (diagnostics centre) in place. They just have to juice it out with more customers which can be fetched through non-PPP route too.

As centres mature, it will increase there ROCE / ROE / Op margin. As they add more centres, business will also growth. So, there is a case of increase in margins and return ratios and also increase in profits. Isn’t it a right scenario to invest in a stock? For e.g. Lal pathlabs is already big. It will be tough for them to grow at 25% via – a – via. Krsnaa for whom it will be relatively easier. Lal pathlabs also has good ROCE / ROE so there is limited upside. For Krsnaa, this upside is also huge.

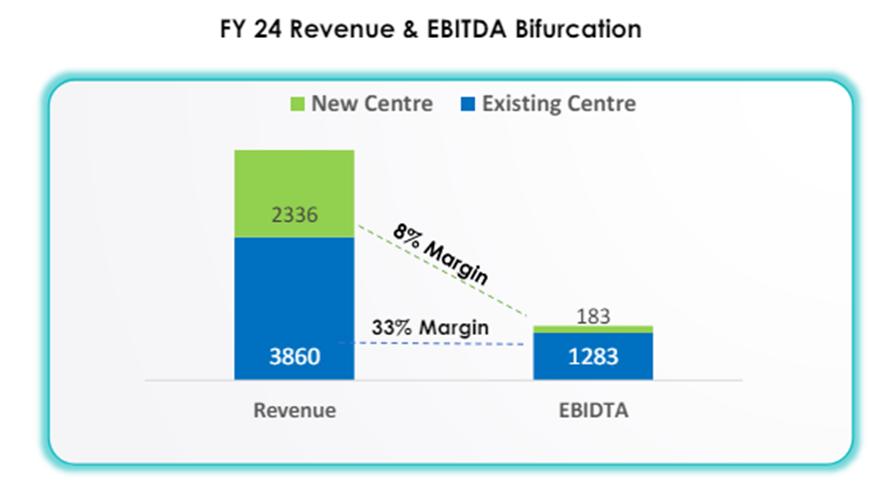

Look at the below table. Mature centres has 33% EBIDTA margin. Let us assume Rs. 234 cr is matured now. They will also have 33% margin instead of 8% margin. i.e. addition of Rs. 58 cr more EBIDTA. This Rs. 58 cr will directly go to PAT, doubling PAT from Rs. 57 cr to Rs. 115 cr. Just the maturity of existing centres can double the PAT. It will also improve ROCE and ROE. PE will reduce to 16 (Rs. 1844 cr mcap / Rs. 115 PAT).

Please provide counter points.

Disc: Invested