The article suggests that the transformer companies will need massive capex to meet the demand.

Posts in category Value Pickr

Jindal Drilling – Beneficiary of a sustained offshore upcycle? (04-11-2024)

Thanks for the great write-up @nirvana_laha .

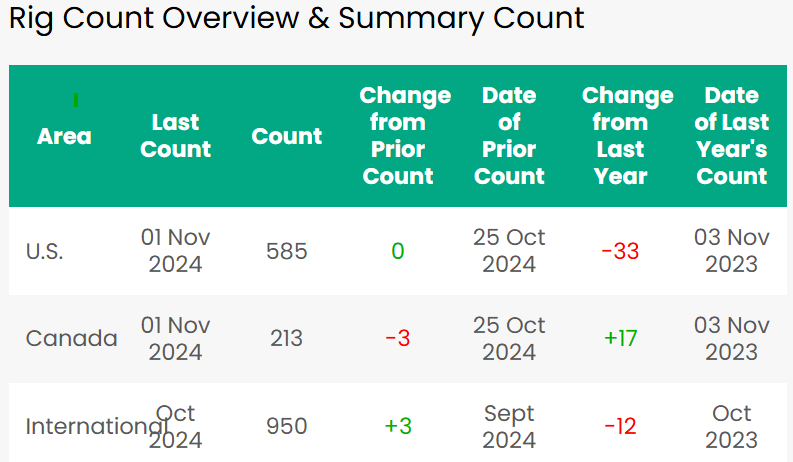

https://rigcount.bakerhughes.com/ is great source to track drilling activity of oil and gas industry across the world.

It releases worldwide data of active rig count during first week of every month. (Active rig: drilling activities occurred during the majority of week).

overview of latest data:

Monthly break up region wise/offshore/land drilling:

| October-24 | September-24 | October-23 | |||||||||||||||

| Land | Offshore | Total | Month Variance | Land | Offshore | Total | Month Variance Year Ago | Land | Offshore | Total | |||||||

| Latin America | 115 | 40 | 155 | -2 | 118 | 39 | 157 | -20 | 147 | 28 | 175 | ||||||

| Europe | 97 | 25 | 122 | 1 | 95 | 26 | 121 | 0 | 87 | 35 | 122 | ||||||

| Africa | 89 | 11 | 100 | -6 | 94 | 12 | 106 | -11 | 90 | 21 | 111 | ||||||

| Middle East | 301 | 41 | 342 | 5 | 302 | 35 | 337 | 5 | 293 | 44 | 337 | ||||||

| Asia-Pacific | 124 | 107 | 231 | 5 | 126 | 100 | 226 | 14 | 126 | 91 | 217 | ||||||

| International | 726 | 224 | 950 | 3 | 735 | 212 | 947 | -12 | 743 | 219 | 962 | ||||||

| United States | 568 | 18 | 585 | -2 | 567 | 20 | 587 | -37 | 600 | 23 | 623 | ||||||

| Canada | 217 | 2 | 219 | 2 | 214 | 3 | 217 | 27 | 191 | 1 | 192 | ||||||

| North America | 785 | 20 | 804 | 1 | 781 | 23 | 804 | -10 | 791 | 24 | 814 | ||||||

| Worldwide | 1511 | 244 | 1754 | 4 | 1516 | 235 | 1751 | -22 | 1534 | 243 | 1776 | ||||||

we can also track active rig count activity country wise/yearly/quarterly as mentioned in the below report.

October-2024 WorldWide Rig Count Report.xlsx (1.1 MB)

Baker Huges also provides separate data for North-America(USA and Canada) which is more detailed.

Discl: Invested recently. Not significant allocation of portfolio.

Jindal Drilling – Beneficiary of a sustained offshore upcycle? (04-11-2024)

Thanks for the great write-up @nirvana_laha .

https://rigcount.bakerhughes.com/ is great source to track drilling activity of oil and gas industry across the world.

It releases worldwide data of active rig count during first week of every month. (Active rig: drilling activities occurred during the majority of week).

overview of latest data:

Monthly break up region wise/offshore/land drilling:

| October-24 | September-24 | October-23 | |||||||||||||||

| Land | Offshore | Total | Month Variance | Land | Offshore | Total | Month Variance Year Ago | Land | Offshore | Total | |||||||

| Latin America | 115 | 40 | 155 | -2 | 118 | 39 | 157 | -20 | 147 | 28 | 175 | ||||||

| Europe | 97 | 25 | 122 | 1 | 95 | 26 | 121 | 0 | 87 | 35 | 122 | ||||||

| Africa | 89 | 11 | 100 | -6 | 94 | 12 | 106 | -11 | 90 | 21 | 111 | ||||||

| Middle East | 301 | 41 | 342 | 5 | 302 | 35 | 337 | 5 | 293 | 44 | 337 | ||||||

| Asia-Pacific | 124 | 107 | 231 | 5 | 126 | 100 | 226 | 14 | 126 | 91 | 217 | ||||||

| International | 726 | 224 | 950 | 3 | 735 | 212 | 947 | -12 | 743 | 219 | 962 | ||||||

| United States | 568 | 18 | 585 | -2 | 567 | 20 | 587 | -37 | 600 | 23 | 623 | ||||||

| Canada | 217 | 2 | 219 | 2 | 214 | 3 | 217 | 27 | 191 | 1 | 192 | ||||||

| North America | 785 | 20 | 804 | 1 | 781 | 23 | 804 | -10 | 791 | 24 | 814 | ||||||

| Worldwide | 1511 | 244 | 1754 | 4 | 1516 | 235 | 1751 | -22 | 1534 | 243 | 1776 | ||||||

we can also track active rig count activity country wise/yearly/quarterly as mentioned in the below report.

October-2024 WorldWide Rig Count Report.xlsx (1.1 MB)

Baker Huges also provides separate data for North-America(USA and Canada) which is more detailed.

Discl: Invested recently. Not significant allocation of portfolio.

TGV SRAAC erstwhile Sree Rayalseema Alkali (04-11-2024)

EPS growth is seen in this quarter. However, the share price is still not reflecting the same. There is a probability that market expects that EPS growth might not sustain. another thing being, the chart structure looks good to move up. Volumes coming u=in the stock. Let’s wait and watch.

TGV SRAAC erstwhile Sree Rayalseema Alkali (03-11-2024)

(post deleted by author)

Clean Science and Technology Limited (CSTL) – A clean and green future ahead (03-11-2024)

CSTL will be firing all cylinders in upcoming quarters. Enough consolidation despite good results. As per SOIC, stage 2 is almost over. Lets wait for results.

Disc: only chemical stock in folio with 4% allocation (XIRR 7% )

Tips Industries Limited – Ready to RACE ahead! (03-11-2024)

Lets see… I am also planning to exit partially depending on share price moves.

EFC – Entrepreneurial Facilitation Centre (03-11-2024)

If you are interested in this space, please do watch the documentary on We work

One of the main reason of its earlier collapse was the huge asset liability mismatch and exponential but super aggressive growth on unsustainable lease terms.

Companies in this space working on Straight lease model with supernormal growth will suffer one day.

Aaron Industries Ltd- The Elevator Play (03-11-2024)

Please go through the below posts:

Sugar Cycles: 7-8 years of losses followed by 2-3 years of super gains! (03-11-2024)

We don’t know their time horizon, what if they’re riding the IPO momentum and have no plans to stay invested? Borrowed conviction is useless anyways without understanding their actual thought process.