@ Naval Latest concall

Posts in category Value Pickr

Investing Basics – Feel free to ask the most basic questions (26-05-2024)

Cost to carry of futures (i.e., the interest rate of leverage) in future market is considerably high – almost 10 to 15% per year – if you add cost of rollover, opportunity cost of cash held for margin requirement, transaction charges, taxes etc. combined.

Using futures to leverage over long term is usually not worth it and comes with considerable risk. You would have to get the timing incredibly right for it to make money.

Shivalik Bimetal Controls Ltd (SBCL) (26-05-2024)

US recently announced heavy duties to be imposed on Chinese imports into US viz . EV batteries, cars, solar cells, aluminium among others . With these duties the export to US will be impacted so the next big market for chinese to dump the extra production will be india .

EV and batteries uses shunts, so if cheap producta from china are getting flooded into the market than domestic demand for shunts will be affected unless India also announces similar duties like US or YS lifts these duties, both look unlikely at the moment. This is one of the main reasons i think SBCL is see a price correction

Shivalik has had a tremendous run and the long term prospects look good, not to forget that shunts are also used in electric meters and many cities are looking to adapt these smart meters

Disc : not sebi registered . Not a buy/sell recommendation

Manappuram Finance (26-05-2024)

if asirvad got listed separately then it will lose all the parental protection of manapuram including not able to expand operations through manapuram getting loans from parent and getting loans from third party at a discount and cross selling does not make sense to separate them except for short term gains in value as they say if you want to go faster go alone if you want to go further go together

other views are welcome

P.E. Analytics Ltd (PROPEQUITY) – Another Data Analytics Platform for Real Estate Players (26-05-2024)

Judging from the discussion so far, the following points seem to be the consensus view:

-

Investors find the subscription business unexciting.

-

The valuation vertical seems promising, but no one seems to have more insights to share.

-

The cash on the balance sheet is a common concern.

I have done a significant amount of work on the industry in the last year with @nirvana_laha. I have met with management a few times since listing, spoken to several of Prop Equity’s clients as well as competitors in the valuation vertical. In the interest of raising the quality of the discussion on the company, here’s my view on how one should look at the company.

1. The valuation vertical has the highest probability of scaling successfully

I spoke to senior management at one of the largest PSUs, as well as a private bank, both are Prop Equity’s clients. Here are the key points:

-

Banks get valuation reports made for loans against property as well as new developments. For almost all private banks and PSUs, this is outsourced to companies like Prop Equity.

-

Depending on the ticket size, they need either two or three reports per property, and use the consensus to determine the loan eligibility / amount.

-

A vast majority of these reports are done by small brokers that operate out of a few districts in a city. (Example: Patwardhan Consultants that cover Mumbai / Pune / Nashik) There are only two or three companies that offer valuation services pan-India. Prop Edge and Adroit are in this list.

-

Banks have their own issues working with smaller regional brokers:

-

Lack of a uniform reporting format – A valuer in Bangalore may provide a different kind of property report from a valuer in Kolkata. This quickly becomes a headache with scale.

-

Small brokers don’t have bandwidth – The last week of a month is extremely busy, as banks try to clear pending loan cases. During this period, smaller valuers who run a 5-6 person office get overloaded, and they can’t cater to everyone at the same time. During this period, the turn around time for a report gets stretched to several days, while every bank wants them asap.

-

-

Larger organisations like Prop Equity or Adroit don’t run offices as lean (40-50 employees in major cities), and therefore have more people. This allows them to meet TAT targets during these busy periods. They also have standardised reports from across the country.

In cities where Prop Equity and Adroit have scaled successfully, they have taken 30% wallet share each from a large bank, displacing smaller unorganised brokers.

The thesis here is a shift from the unorganised to organised given a lack of serious pan-India players. There is room for 3-4 pan India companies to empanel with a bank, as banks have limits on how much wallet share a single valuer can take.

I leave it up to the reader to determine the market size for this vertical in India, but I have high confidence in Prop Equity scaling this vertical to 100 Cr. topline, with 40% EBITDA margins in the next few years.

2. The subscription business does not deserve bandwidth

It’s very difficult to raise prices for the subscription vertical as it stands right now. They have onboarded almost every large developer and bank. The TAM for this subscription business is at its infancy in India, and it’s far more profitable to build and sell value add services on the data they have collected.

This business will continue to bring in 40-50% margins as the costs are fixed, and this is why management calls this a cash cow. Any incremental effort spent on this vertical wont be as rewarding as the other new verticals that management has incubated, so it’s completely reasonable for management to focus efforts elsewhere.

The proof of this is in the valuation vertical: in 3 years, they have built this business from scratch and scaled to the size of the subscription business already, with over 400 employees and a topline of 20 Cr.

3. The cash on the balance sheet will be used on new verticals

Management’s model here is to incubate a new vertical, provide equity to the partner running the vertical, see how it fares with clients, and only after seeing success, spend on scaling the business.

There are three new verticals being scaled at the moment: developer management, project monitoring, and the vehicle valuation. Management mentioned that if project monitoring sees good traction in the next year or two, they’ll increase the spending on sales & marketing to increase visibility and win clients.

4. There are several dormant optionalities

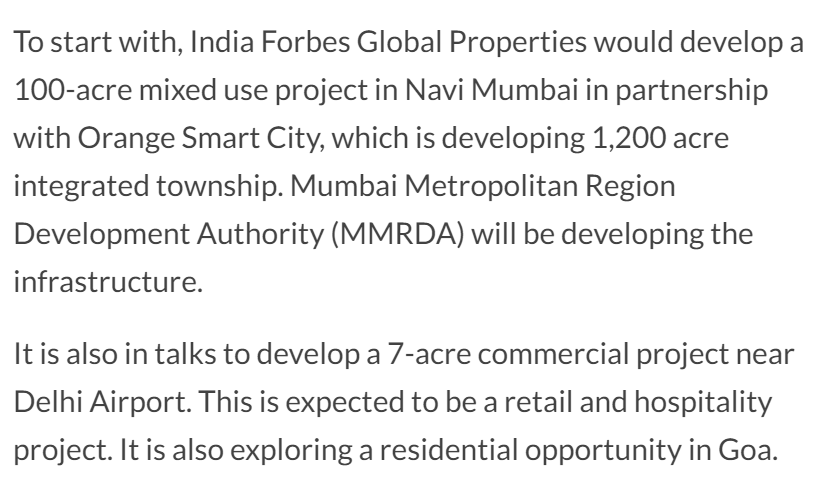

- Developer management is a vertical with Forbes Global that could have a large leap for Prop Equity given the profit sharing agreement. The JV will earn 10% of the sales value of any property developed and sold by the JV, and distributed to the partner that brought in the deal. They also have an agreement to develop one such property within five years.

-

Project Monitoring is the B2C vertical that management has been working on for the last 3 years. His claim is that this market is larger than the valuation vertical, and there is no competition in this space in India right now.

-

YouTube can be a very powerful platform with scale. There are numerous success stories of people who have started with producing videos, gaining a following, and then starting a business / selling a product to subscribers. If management can scale this to 100k followers and beyond, this could be a great platform for lead generation for all the other verticals.

In my opinion, I think investors should focus more on the valuation vertical scaling, and treat project monitoring, developer management and the automobile valuations as an optionalities without pricing them in.

D: invested in family accounts, no transactions in the last 30 days.

I’m amazed by how confidently people can write such things about others they’ve never met. Especially on a first name basis. I feel it’s undeserving of this forum.

Schneider Electric Infrastructure: A global company with advantage of a industry tailwind: (26-05-2024)

Anyone can put more insights please on recent result : Mainly about the provisions they have made this year and also the expenses incurred for shifting the plant from one place in Kolkata to the new place ( any insight will help to understand ) and how these points will affect the balance sheet.

My portfolio updates and investment journey (26-05-2024)

@Sandeep777 thanks for writing in.

I have not studied other businesses so difficult to comment.

On Fino, management guided 20% topline and 30% bottom line. I checked with someone who knows management somewhat, feedback is that management is good.

I have small position and shall ramp-up as maangement delivers.

@A.R_PAWAR Nuvama is mainly catering to UHNI and HNI’s so market regulator might not be that sensitive in this area.

Disclaimer: I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example purpose. I may buy more, exit or partly sell the stock/bonds without any prior intimation . Also note that I recently joined a investment advisory firm. My portfolio is not a recommendation for anyone. Some of these stocks might be in clients portfolio as well so please be aware of vested interest.

Time technoplast (26-05-2024)

The result were in line with expectation. Pbt at 132 v/s 92 cr yoy. Management has guided for 15% growth with better ROE and debt free in 2-3 years. With all future earning & ROE with debt reduction playing out there is a scope for some rerating .

I personally believe it will slowly playout over next 1-2 years.

I expect a 50-70% upside in next 18-24 months

Disc -personal view only

Invested recently added in tranches

Ranvir’s Portfolio (26-05-2024)

KOPRAN –

Q4 and FY 24 results and concall highlights –

Q4 outcomes –

Revenues – 186 vs 158 cr, up 18 pc

EBITDA – 22 vs 12 cr, up 76 pc ( margins @ 12 vs 8 pc )

PAT – 19 vs 7 cr, up 168 pc

FY 24 outcomes –

Revenues – 615 vs 551 cr

EBITDA – 74 vs 52 cr ( margins @ 12 vs 9 pc )

PAT – 51 vs 27 cr

Total API sales @ 94 cr vs 76 cr YoY ( exports @ 50 pc )

Total formulations sales @ 89 cr vs 76 cr YoY ( all exports )

Company has a product basket of 26 commercialised APIs. Company is a major player in Carbapenems and is a leader in Atenolol. Other APIs made by the company include – Macrolides, Cephalosporins, Pregabalin. All API blocks are located at their plant @ MIDC Mahad, Maharashtra

Formulations plant located @ Khopoli, Maharashtra. It’s WHO compliant. Also approved by US FDA, EU GMP for non-sterile products

Company’s new API plant is ready @ Panoli

(Gujarat). Expected to start commercial production in Q3 FY 25

Company is guiding for 18 – 20 pc revenue growth without factoring in anything from the new Panoli plant. Also guiding for 100 cr EBITDA without the Panoli plant

Company’s gross margins stay in the band of 32-37 pc depending on competition from China, general demand scenario, RM prices etc

Company has submitted validation batches of Atenolol to the largest Atenolol ( anti-hypertensive ) – formulation player in US. Expect the commencement of commercial supplies in about 6 months from now. Also expect the commencement of supplies of Nitroxoline ( antibiotic ) into EU mkts wef June 24

Not looking at any major Capex for this FY. Next leg of Capex is expected at Panoli – ie addition of a new block, commencing sometime next FY. Capex for next 3-4 yrs shall only be brownfield – ie at existing facilities

Disc : hold a tracking position, looking out for margin expansion, biased, not SEBI registered

Kopran Ltd. – Has its time finally come?! (26-05-2024)

KOPRAN –

Q4 and FY 24 results and concall highlights –

Q4 outcomes –

Revenues – 186 vs 158 cr, up 18 pc

EBITDA – 22 vs 12 cr, up 76 pc ( margins @ 12 vs 8 pc )

PAT – 19 vs 7 cr, up 168 pc

FY 24 outcomes –

Revenues – 615 vs 551 cr

EBITDA – 74 vs 52 cr ( margins @ 12 vs 9 pc )

PAT – 51 vs 27 cr

Total API sales @ 94 cr vs 76 cr YoY ( exports @ 50 pc )

Total formulations sales @ 89 cr vs 76 cr YoY ( all exports )

Company has a product basket of 26 commercialised APIs. Company is a major player in Carbapenems and is a leader in Atenolol. Other APIs made by the company include – Macrolides, Cephalosporins, Pregabalin. All API blocks are located at their plant @ MIDC Mahad, Maharashtra

Formulations plant located @ Khopoli, Maharashtra. It’s WHO compliant. Also approved by US FDA, EU GMP for non-sterile products

Company’s new API plant is ready @ Panoli

(Gujarat). Expected to start commercial production in Q3 FY 25

Company is guiding for 18 – 20 pc revenue growth without factoring in anything from the new Panoli plant. Also guiding for 100 cr EBITDA without the Panoli plant

Company’s gross margins stay in the band of 32-37 pc depending on competition from China, general demand scenario, RM prices etc

Company has submitted validation batches of Atenolol to the largest Atenolol ( anti-hypertensive ) – formulation player in US. Expect the commencement of commercial supplies in about 6 months from now. Also expect the commencement of supplies of Nitroxoline ( antibiotic ) into EU mkts wef June 24

Not looking at any major Capex for this FY. Next leg of Capex is expected at Panoli – ie addition of a new block, commencing sometime next FY. Capex for next 3-4 yrs shall only be brownfield – ie at existing facilities

Disc : hold a tracking position, looking out for margin expansion, biased, not SEBI registered