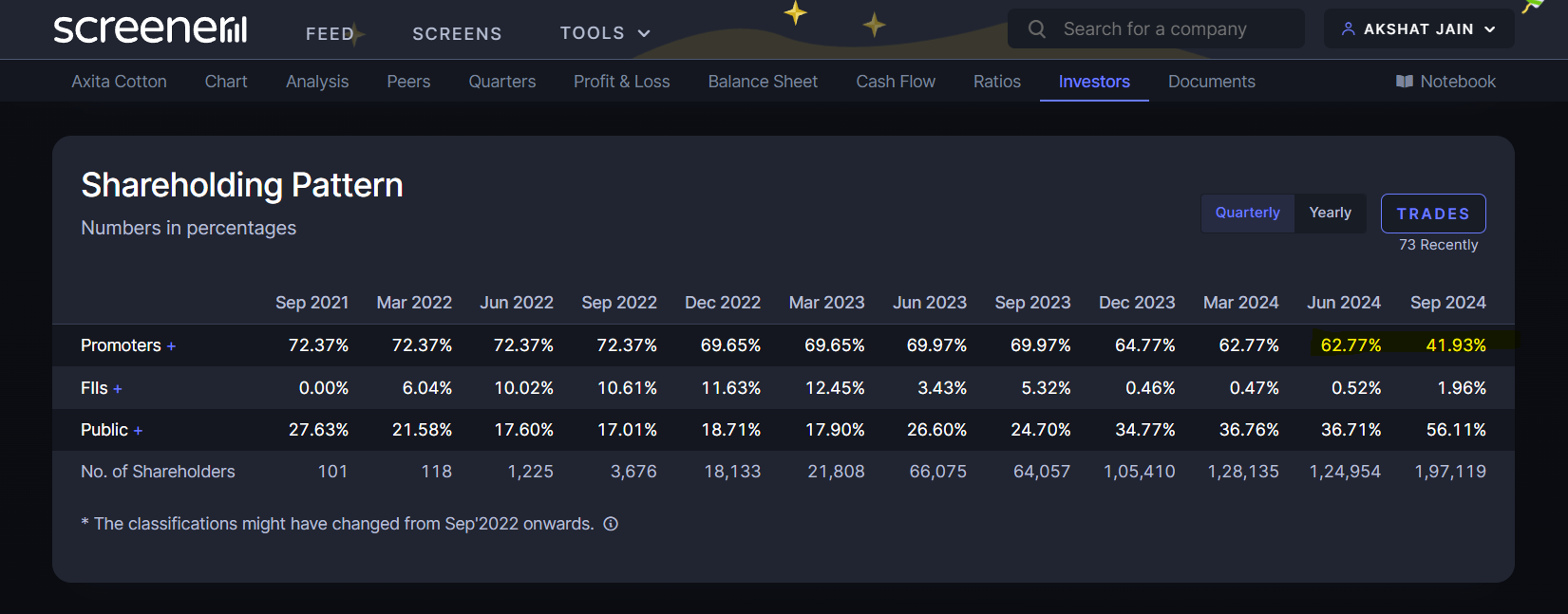

Again a dump activity has been noticed.

Promoters exited 20% of their stake.

Is there any specific reason as to why?

Again a dump activity has been noticed.

Promoters exited 20% of their stake.

Is there any specific reason as to why?

I believe it’s not fair to compare DMart with Quick commerce companies. I see QC more like a logistics provider with wafer thin margins and no entry barrier, Moat. For that matter DMart, JIO or any other brick and mortar store can easily enter this space if more customers lean towards online shopping or leverage Dunzo like services.

DMart will survive as long as the Costcos, Walmarts and IKEA draws customers who are inclined towards in shop experience

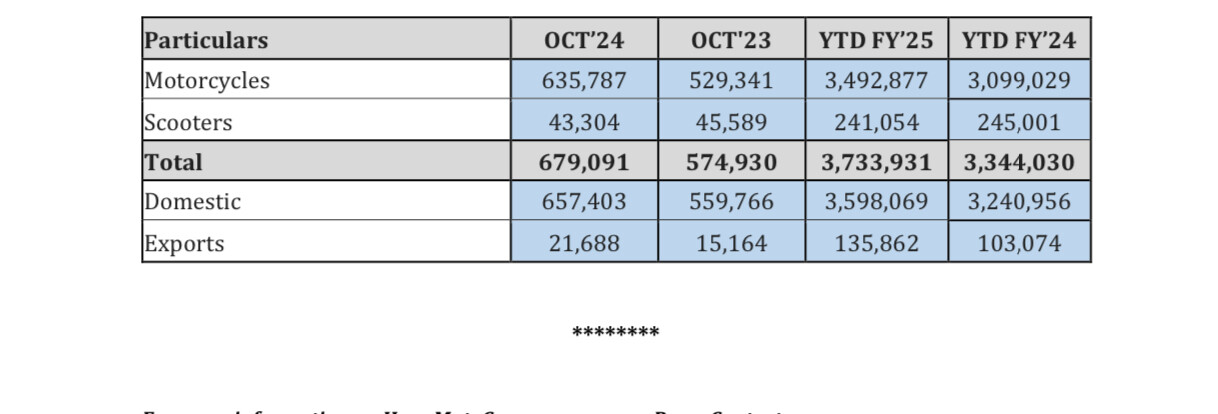

HERO MOTOCORP SELLS 6.8 LAKH MOTORCYCLES & SCOOTERS

IN OCTOBER 2024; REGISTERS 18% GROWTH

What is the source of this information ? Innovasynth technologies Ltd had a PAT of -2.9 Cr in FY 23 on a topline of 203 Cr and PAT of -0.5 Cr on a topline of 160 Cr in FY 24. Where did you get this no of 25 Cr PAT and projection of 50 Cr PAT for FY 25 ?

Hi @Deven, there is a new filter introduced recently: “Is SME” and “Is not SME” as mentioned here – Seamless Filtering of SME companies – Screener. Hope this helps!

Yes – you can google Innovasynth ICRA .

Nice analysis ,holding @160/-

“So we are advertising the Spicy Chicken BIC, which is missing from our menu, which has got a massive following. I think we expect that 50% of our chicken sales, BIC sales, will now be on this product. So we have introduced that product. We have just started marketing that product in all 360 degrees and digital channels, television and so forth. So we put that out there. So that big chunk of work is done. We have cleaned out the portfolio.

We are further looking at tightening up our G&A, which will be in the next 4 weeks. We will be working on further reducing our G&A and our overheads over there. Consolidating the total G&A down to a very minimal number. And then focusing on our restaurants and seeing if there are other restaurants that need to be closed or automized. But we have put a good team in place over there. We had the restaurants all refreshed. All the operations, equipment have been fixed.

The menu has been reorganized.

We have a fantastic CMO over there. Namita, who is doing a fantastic job, putting together a marketing program. She’s put a great menu together; she’s cleaned out menu items. So all that is in place. We’re just waiting for the headwinds to stop and the geopolitical issues to be behind us, and hopefully, some positive macros for us to turn around.”

Concall regarding indonasia

Thanks for sharing. Where can I find more details about the business? The Annual report only mentions one paragraph.

It’s an enhancement, plus it’s free.

Plugin might look average to you, but over time it will develop.

I really like it and it does look similar to what trendlyne offers with historical ratios.