I mean the general quality of confidence is lower with smaller auditors. Not a capability point more related to intent and checks and balances. Especially when management description of accounts is questionable as in this case…

Posts in category Value Pickr

Avanti Feeds (17-05-2024)

They increased salaries by a good amount sometime in 2023. And unless I’m very wrong this factor has depressed both return ratios and share price reducing returns for management…

But thanks for the response. It’s quite frustrating. They’ve been gaining market share and have seemingly avoided many pitfalls better than competition (my company works with other players in theindustry so have some general idea of what’s going on), but this fact I’ve not been able to fathom.

Jash Engineering – Is it a multibagger (17-05-2024)

Read the FAQ document on their website

SmallCap Hunter : Trying to find the dark horses with triggers (17-05-2024)

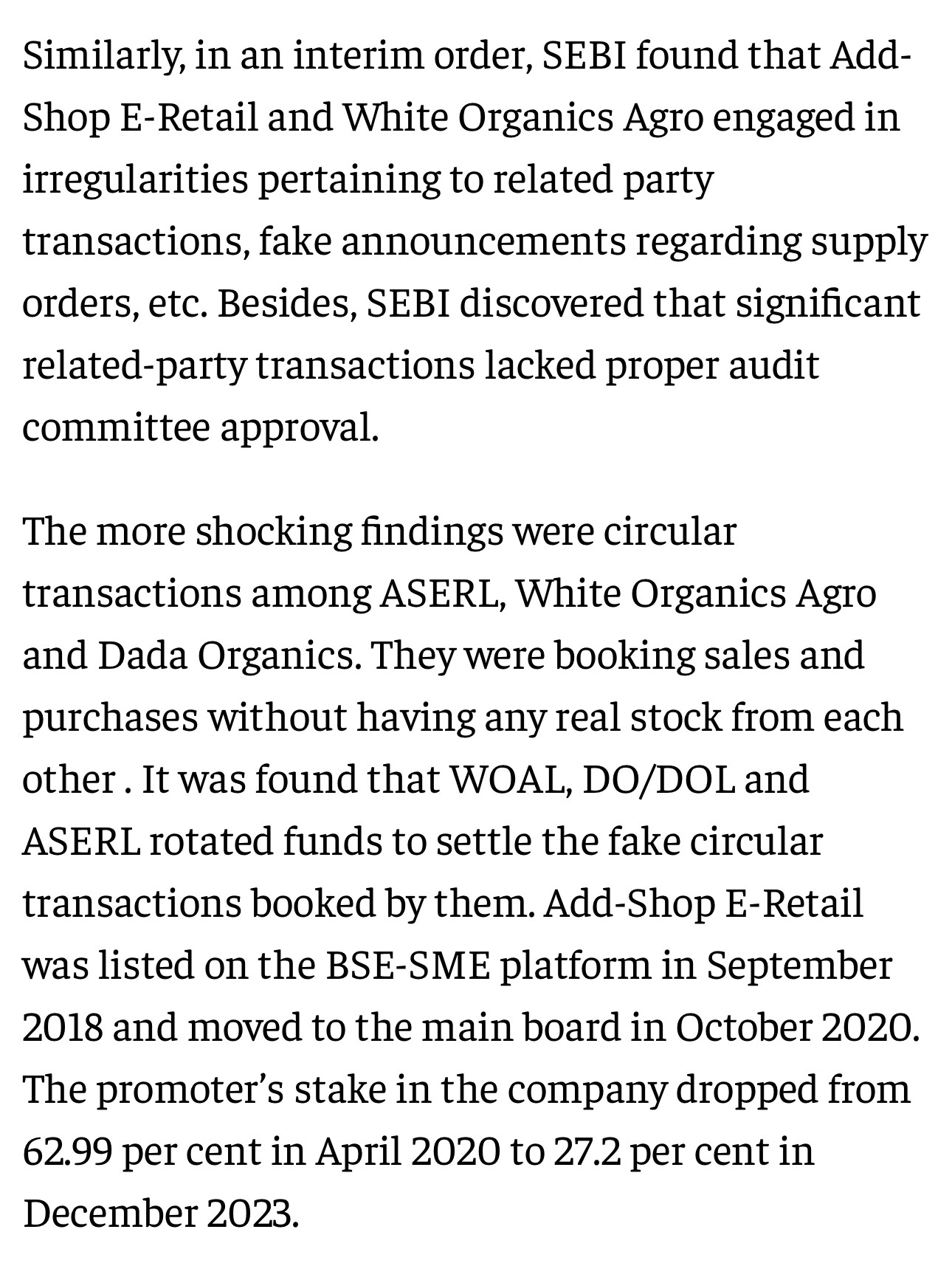

The red flags that I raised back then on this company couldn’t be any clearer and finally it all came out in the open. Interestingly, SEBI found out same things that I pointed out in my post, related party transactions and fake sales/manipulation of P&L. I am glad I didn’t invest. Market has its own of teaching a lot of things and keeping you humble. ![]()

Amoul Portfolio (17-05-2024)

I have also gone through their concalls and AR, and I also googled it but could not find anything. I am not sure, but it seems they aren’t giving them anything, as they haven’t mentioned their names in their client list.

ValuePickr Kolkata (17-05-2024)

Please plan one, guys

Hitesh portfolio (17-05-2024)

I had managed to look at breakouts in these renewable stocks and managed to ride one of them in form of Inox Wind Ltd. I exited it a bit early but with the kind of allocation and returns I was getting within 7-8 weeks, I was quite satisfied with my returns.

I had a look at other stocks in the sector like SW solar etc but somehow could not figure out how earnings are going to pan out. And often times when you are focussed on your portfolio picks and do not have too much funds to deploy to new ideas, you often miss such sectors.

In investing, these kind of misses are part and parcel of the game. As long as your winners take care of such lapses, portfolio returns are okay.

Wonderla Holidays (17-05-2024)

Because they have to prepare for exams, their teachers and parents have to adjust for the changes. Considering they have many rides catering to different age groups, and if an entire school which consists of all the classes, the students would at least be in single digit hundreds, just the students also, and if staff and some parents join, the number would be even more. And this is for one institution, so the more such entities, the more will be the footfalls. Maybe resort generates some revenue too from these footfalls. How much such revenues will be generated, and what is the % of such revenues in a quarter’s revenue, I have no idea.

Just some general thoughts, not invested but follow the thread, interested in the business.

Aarti Pharma Labs (17-05-2024)

Capex:

- Total capex for FY25 expected to be around 600 crores.

- Major projects include Atali greenfield project in Gujarat costing around 300 crores.

- Additional capex for expanding Xanthine capacity at Tarapur and intangible asset development.

Xanthine Derivatives:

- Xanthine capacity utilization currently at 90%.

- De bottlenecking project to increase capacity from 5000 to 9000 metric Tons.

- Price decline of 20-25% impacting topline, while volume growth around 12-15%.

CDMO/CMO Segment:

- Working with 16 customers on 40 projects, with 21 commercial projects.

- Added 12 new projects in the year.

- Expecting growth in this segment due to expansion of manufacturing facilities and regulatory focus.

- Majority of products in Key Starting Material (KSM) and Regulated Starting Material (RSM).

- Quarter-to-quarter fluctuations expected due to multi-stage products and campaign-based orders.

- Focus on reducing customer dependence on China for KSM/RSM.

Margins:

- Record margins achieved in Q4 FY24.

- Gross margins at 55% for standalone entity and 50% on a consolidated basis.

- CDMO business contributing significantly to margin improvement.

- Expectation to maintain close to 50% gross margin annually.

Revenue Growth:

- Expect EBITDA growth of 10-12% in FY25.

- Moderately conservative guidance given due to market volatility.

- Topline growth in Xanthine segment dependent on pricing metrics and capacity utilization.

- Sustainability of revenue growth in CDMO segment due to expansion and new projects.

Expansion Projects:

- Brownfield expansion of Xanthine capacity to be completed by end of FY25.

- Atali project progressing as per plan, commissioning expected in Q4 FY25.

- Semi-commercial block at USFDA intermediate manufacturing site in Vapi to become operational in current quarter.

- Setting up solar power plant in Akola to fulfill 1/3 of power requirement and reduce manufacturing costs. It may add to margins.

Financials:

- Highest EBITDA and net profit recorded in Q4 FY24.

- Consolidated EBITDA and PAT growth on Q-o-Q and Y-o-Y basis.

- Standalone EBITDA and PAT growth in Q4 FY24 and FY25.

- Return on capital employed improved to 18% in FY24.

Outlook:

- Expecting EBITDA growth of 10-12% in FY25, aiming for around 15% annual growth in the next two years.

- Focus on business expansion, sustainability, self-reliance, and customer needs.

- Optimistic about future growth potential, especially in CDMO/CMO segment.

Spinoff from Aarti Industries in 2023, now it can show results.

Ease of pricing pressure in US. Pharma sector is under valued not participated in Bull market since 2015.

Huge Opportunity for CDMO/CMO for small companies. Regulatory cost in developed countries are making drug delivery extremely costly, which turn give rise to Indian Pharma players due to good track record in pharma industry.

Leader in Xanthine.

Recent rally after result indicates valuation comfort. Any further surprise in earning can totally re rate the stock due to sector offers value.

Disclosure: Invested. Notes from screener.

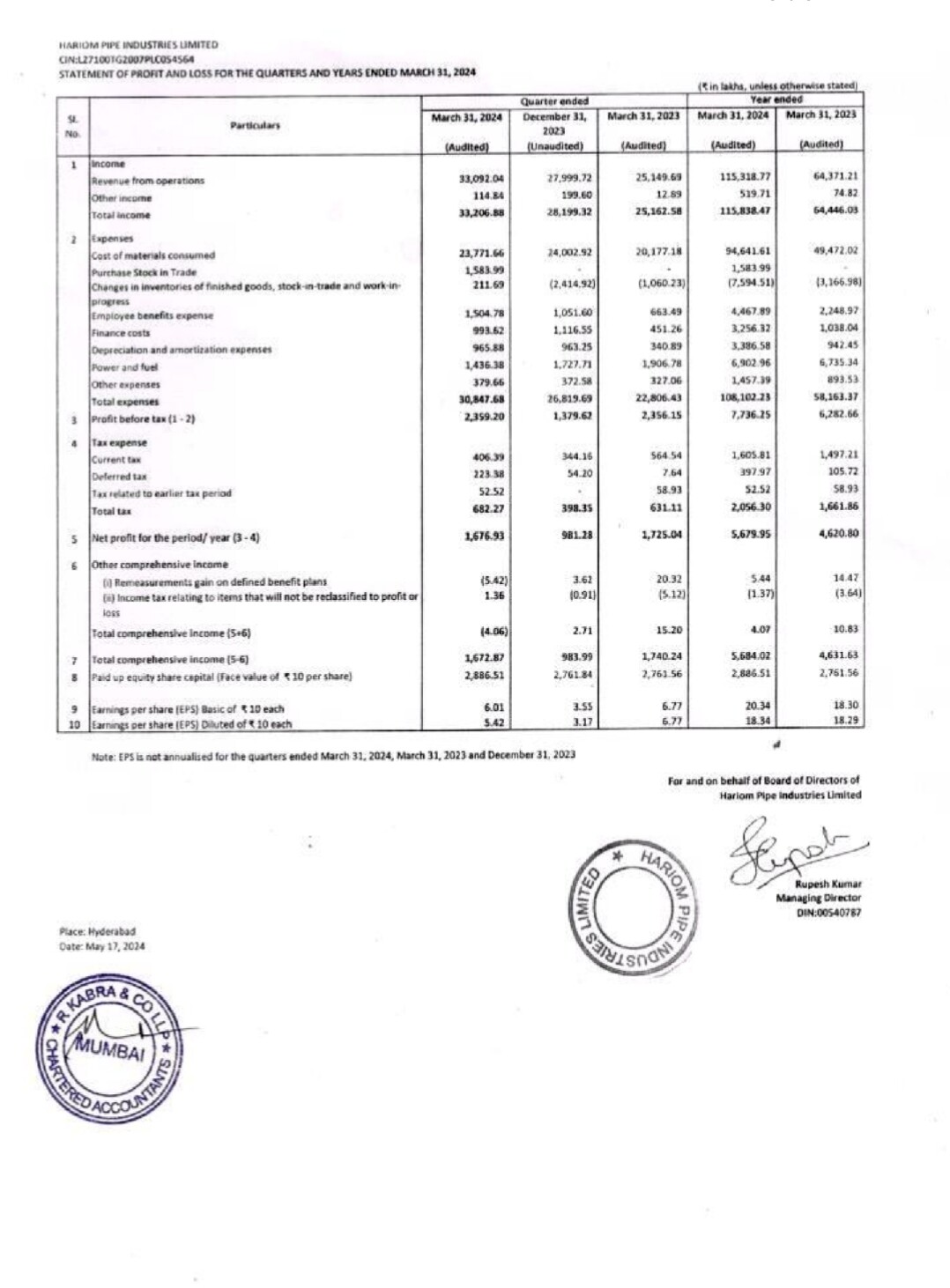

Hariom Pipes Ltd: A Capex Play! (17-05-2024)

Hariom Pipes Results

Impressive Set ![]()

Sales up 18% QoQ n 32% YoY ![]()

EBITDA up 29% QoQ n 34% QoQ ![]()

EBITDA Margin at 12.7% vs 11.64% QoQ n 12.47% YoY ![]()

PAT up 70% QoQ n -3% YoY ![]()

OCF +4.95 vs -100cr YoY

OCF +ve after 5 Qtrs ![]()

Div of 0.6₹

Expectations Beaten ![]()