Hi @ayushagrawal is this opportunity still open?

Posts in category Value Pickr

Addictive Learning Technology limited (LAWSIKHO) (10-05-2024)

https://twitter.com/caswapnilkabra/status/1788917271278043427?t=pMchcdmHbYwtW9pWneZ6mA&s=19

Concall updates by SwapnilKabra

Investment journey of a late starter (10-05-2024)

i am really bullish on Wockhardt like you…so many interesting drugs and the antibiotics in pipeline are so exciting as the efficacy of antibiotics dwindle in the world…I bought at 220 so obviously one well but no desire to sell.

I think one needs to have money in smallcaps…especially in this era…I just find largecaps (like Titan,HUL etc) so overvalued.even many midcaps…and even if they arent there is little chance because FIIs and fund houses buy them crazily…

I like buying comanies when they are out of favour and have bought Spicejet and Vascon at much lower prices…And I just like to hang on…

Low Volatility Stocks (10-05-2024)

I had done a trial by investing in ICICI Prudential Nifty 100 Low Volatility 30 ETF. After remaining invested for 2 years , I exited last year as my return was only 15% per annum , though my return from flexi cap and multi cap fund was 30-40% during the same period.

However, the same ETF seems to have given a descent return this year with 29%, though some multi cap/.flexi cap funds have given 50% + this year. ( kotak multicap , quant flexi cap)

the portfolio of icici LV390 ETF is given below.

Low Volatility Stocks (10-05-2024)

@Chandragupta Thank you for this reference.

I went through the short thread. Very interesting.

-

@Viraj_Kawatkar has not defined the universe. He talks about doing both large caps and others; therefore, I guess he has used the entire universe (N750). My plan is to use N200 which is a mix of large and midcaps (Nifty 50 + Nifty Next 50 + Midcap 100).

-

He stopped in a few months and shifted completely to Momentum. Don’t know what his experience was. I have been doing DIY momentum for the last 18 months and looking to add this low volatility pf.

-

He talks about adding a touch of momentum by considering stocks that are close to their 3 year highs (2nd layer of short listing). This is a good suggestion and I might try and use it. I had already planned for 1 year positive change and CMP > 200 DMA.

-

Don’t know if @manojh is still continuing with this methodology. If yes, would like to hear his experience.

Par Drugs & Chemicals Ltd (10-05-2024)

For the past 9 quarters, the bottom line is almost flat. What is happening here?

however the margins have improved a lot.

Investment journey of a late starter (10-05-2024)

Posting today as this is the day when I have finally sold off intellect design arena. When I bought it in 2020 end at around 600,I was very convinced that it is going to be a multibagger for me and I would hold on to it forever.It was my highest conviction bet back then apart from globus spirits ,then it even went up to 1050 and then dropped back to 600 .I started adding again and it became my largest holding by invested amount in 2023 beginning. At one point it even to below 400 and . I still held on with 40% loss. Overall after holding it for 3.5 years,I booked out with 55% profit And zero satisfaction.

It is going to be very nice not to worry about their endless products that solves all banking issues but adds nothing to the bottom line and endless ESOPs.

Such a relief!

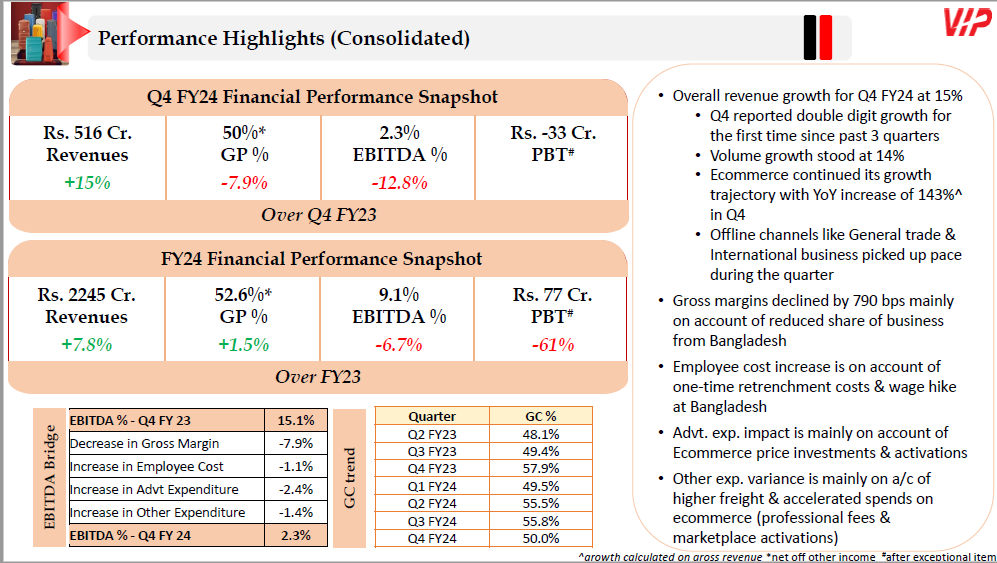

VIP Industries : Luggage (10-05-2024)

Another bad quarter for VIP with just 2.3% EBITDA margin and Rs.33 cr PBT loss.

Moreover, deteriorating balance sheet is another concern. Inventory has shot up from Rs.587 cr in Mar 2023 to Rs.916 crore in Mar 2024, which translates into a very stretched inventory holding period of 315 days. Sales growth was 8% in FY24 as compared to 56% increase in inventory level.

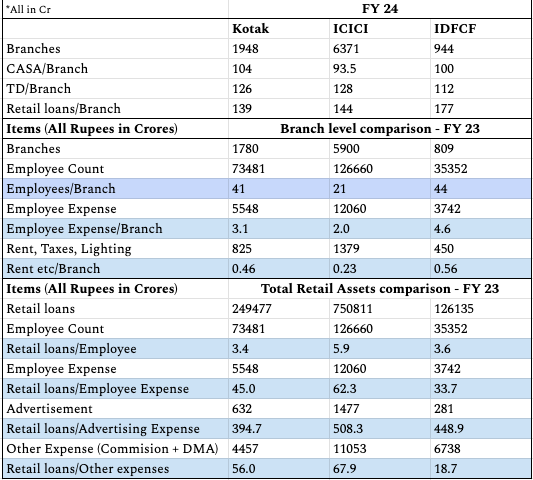

IDFC First Bank Limited (10-05-2024)

I looked at the operational performance of IDFC bank at branch level and compared it with Kotak and ICICI Bank. Please have a look and share your thoughts.

Branch level highlights of IDFCF:

-

IDFCF branches have similar or more average CASA than ICICI & Kotak. It will be interesting to understand the reason since almost 40% of branches are <3 yrs old.

-

IDFCF is distributing ~20% more retail loans/branch than Kotak/ICICI – although at much higher commission ratio (see point 7 for details).

Insights into higher Opex of IDFCF:

-

IDFCF has similar employees/branch as Kotak – but its average employee is paid almost ~40% more than Kotak’s. This difference can be slightly off as banks deploy employees differently but the general idea is fairly accurate.

-

IDFCF has ~20% higher rental etc expense per branch compared to Kotak and almost 2.5x that of ICICI – probably because most of its branches are in urban areas at good locales.

-

It is also interesting that IDFC’s per employee retail loan is similar to Kotak, but almost ~40% less than ICICI. Retail loans/Employee expense is a drag in Opex for IDFCF – it is almost ~30% lower, which should improve over time as the branches mature.

-

Advertisement expense is actually fairly similar to Kotak and sligly more than ICICI, relative to its retail asset and liabilities size.

-

Other expense – which mostly includes commissions is the biggest drag on Opex – IDFCF spends 3x more than Kotak and ~3.6x more than ICICI to generate same amount of retail loans.

-

Other Expenses should continue to be a major watchout for the investors as the commission expense per loan may not come down with scale. The bank will need to work hard and innovate in its distribution strategy to reduce this expense. Other expenses can also include different items for different banks, I have tried to make the comparison as fair as possible.

** Overall comparison with Kotak is more fair since its retail:corporate split is similar to IDFCF.

HDFC Bank- we understand your world (10-05-2024)

HDFC bank traded at 4 times book because the profit growth and RoE were 20% in the past. But if an investor has to take a conservative estimate of book value increase of only Rs70 per share, then it leads to a profit growth of 0% and a decrease in RoE of at least 3% every year (15% in FY25, 12% in FY26 and so on).

BHEL was consistently delivering RoE of 20% and hence traded at P/B=9 till 2010 but then between 2016 and 2023, it traded at P/B of 0.6-0.9 when fundamentals changed.

So if HDFC bank profit growth is mid single digit and RoE is 10-12% (I am not of the view that HDFC bank will go this way in the next 10 yrs), then it will trade at 1.2-1.5 times book like Bank of America.

Hence such conservative estimate of EPS should also change the Price to book multiple assigned to the stock. It is mandatory for HDFC bank (or any other bank) to maintain a EPS growth rate of 10% to even trade at 2.5Xbook (assuming NPA remains same).