Yes, it is NSE SME stock. You need to buy min 1200 qty per lot. You can find this info on NSE website

Posts in category Value Pickr

Basilic Fly Studio Ltd (22-04-2024)

Is this still listed as SME stock? I tried buying small quantity of this and couldn’t buy it from ICICI Direct. Does anyone know if there is a specific quantity of shares I need to buy or I cannot buy it at all?

Gujarat State Petronet Limited (22-04-2024)

This is a serious setback. Even if tariff gets revised this action from PNGRB will remain an overhang which means stock will take a very long time to recover.

HDFC Bank- we understand your world (22-04-2024)

Merger is not working out as well as planned… has led to higher deposit costs and statutory deposits… financial performance will improve only after few years… operational performance will be good… but will not add to profits…

most likely to stagnate at lower levels for a year… at least.

Hitesh portfolio (22-04-2024)

-

I do not know what you mean by FIRE. Pulling the plug from my work (job) was mainly pre decided because I needed to finish minimum 20 years of continuous service to be eligible for pension. So this decision was partly out of my hands. And after resigning from job, I continue to do my private practice, but it is on my terms and conditions and timings.

-

Finding fundamental bets in small caps or any other caps is very well discussed in various threads on VP. Simplest solution is to read a few good books beginning with One up on Wall Street and Zebra in a lion country. (both specifically with respect to small and midcaps)

-

For techno funda picks there is a whole thread on 52 weeks high and all time highs. It has run into a lot of pages and I feel has a lot of useful resource material and examples. It just needs effort to go through the thread. I would also suggest the thread on technical picks by @phreakv6 …

-

I don’t know how my CAGR is going to help you in your learning curve. It will suffice to say that its “satisfactory. ” VP is not the forum like twitter etc where making claims and bragging is encouraged. I stand by that.

Hitesh portfolio (22-04-2024)

I usually have a universe of around 40-50 fundamentally and/or technically strong stocks and keep this on watchlist. These are the names where I have done fundamental research by the usual annual report/concall/presentation resources. These are the names I keep watching during market corrections.

I am usually fully invested and hence have nothing to do except watch the show from sidelines during most corrections. ( I feel going ahead I should be taking partial cash calls, but that’s a work in progress) But what I often end up doing is tinker with some weightages in portfolio and raise some funds to add to a new better option, or replace the weakest link in my portfolio with a new stock. But most of the times its just sitting pat with whatever I have.

HDFC Bank- we understand your world (22-04-2024)

Q4FY24 and FY24 results observations:

Standalone Q4FY24 YoY:

- Other Income doubled due to one-time transaction gain: 7,340 Cr from stake sale in subsidiary HDFC Credila Financial Services Ltd

- Operating expenses include one-time staff ex-gratia provision of 1,500 Cr.

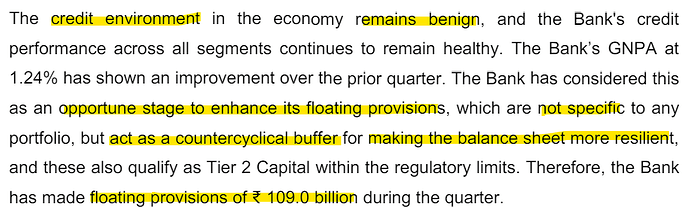

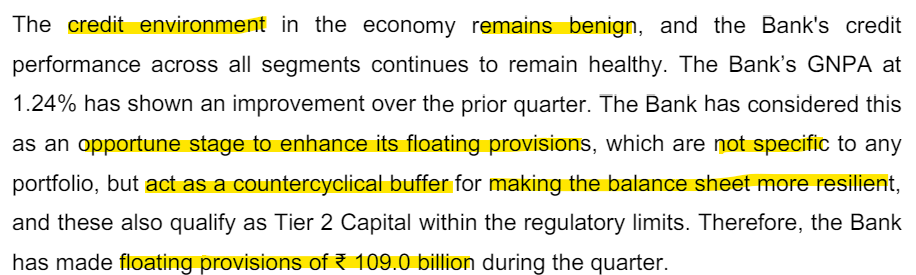

- On creation of the floating provision of 10,900 Cr in Q4FY24.

- Tax expense was (749) Cr due to Tax credit of 4,400 Cr

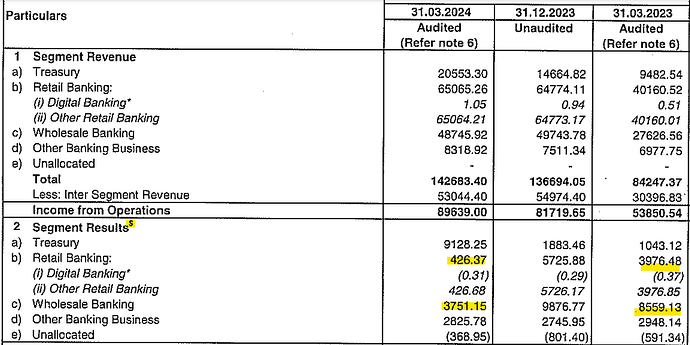

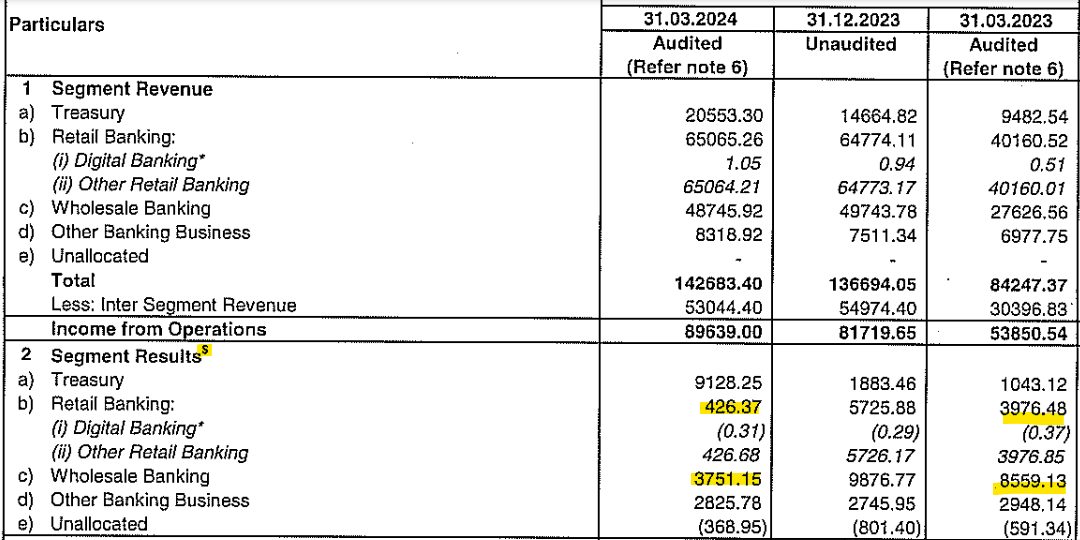

- Segment breakup:

-

-

-

- Deposits increase benefitted from March quarter seasonality. Do not extrapolate as Q1 is always slow historically.

Overall:

- HDFC Limited merged with HDFC Bank effective July 1, 2023. Prior period numbers are not comparable.

- LDR will stay elevated than the past benchmarks for a couple of years. Need to keep reserves to repay the obligations of the eHDFC’s Bond that mature as per their maturity pattern

- No anchor on NIM. Will not chase growth for sake of growth and will neither go down the risk ladder or price ladder. Profitability is extremely important and drop-off in volume is ok, Deploy basis what gets mobilzed. Stable margin is the focus with a positive bias over the next 2~3 Yrs.NIM improvement should be a function of how we substitute the high cost bonds that come up for maturity over a period of time with deposits.It will take time to happen in a gradual manner. Till then (over a period of 2~3 Yrs) stability of metrics (ROA, NIM) remains the focus. Once high cost bonds are exhausted, the bank will have liquidity and ability to unleash growth with profitability coming back to the core level.

Nutshell:

Still settling down. Better growth and profitability seems possible after 2~3 Yrs as high cost borrowing maturity will start to happen from FY25 onwards.How much YoY? Upcoming AR might help.

Hitesh portfolio (22-04-2024)

Trent chart is that of a super stock. It goes up relentlessly irrespective of market situations and fundamentals. If its any comfort to you, I had a look at around 1370 levels and was put away by valuations. ![]() So there goes the better and far thinking mind claims.

So there goes the better and far thinking mind claims. ![]()

Amara Raja Energy & Mobility Limited: Powering Ahead (22-04-2024)

Agree. Low promoter holding is not much of a concern.

Also know that, Nalanda capital is invested in AREM. That means quality of the promoters has to be really good.

Amara Raja Energy & Mobility Limited: Powering Ahead (22-04-2024)

The increase is not because they bought it from open market but because they merged on of their companies with AREM and that increased their shares in AREM.