Personally believe that numbers are shady. Their raw material cost has just went down from 60%+ to less than 30%. This just doesn’t make sense.

Posts in category Value Pickr

Delta Corp – A huge but risky opportunity (11-04-2024)

Delta Corp.’s investment thesis has become more uncertain due to a lack of clarity on future online gaming business plans, as identified through my research. Additionally, the company’s competitive moat and long-term growth prospects in the Indian casino industry appear limited, particularly given the government’s regulatory influence. Considering these factors, I believe Delta Corp. is a riskier proposition at this time and would avoid the stock for the moment.

Delta Corp – A huge but risky opportunity (11-04-2024)

I personally would have taken position in Delta if there online arm Adda52 was doing well. Coz thats one area they can expand tremendously in future as market is ripe for poker a sport to grow. I have been in the poker space for 10 years and i think i understand the space some what. Adda52 is one of the poker sites where in most of the top management doesnt even know the game. Poker used to be a small community and all that was needed was a customer centric approach… they just never cared… made policies in corporate meeting rooms without understanding what players want. Poker baazis management are all players themselves and they sucked the market share out of adda52 and now are doing brilliantly even in a tough gst scenario. I just dnt see add52 doing anything good and is losing more and more space day by day. Adda52 basically spent a lot in promoting poker as sport by doing events in companies and colleges accross the country but sites like baazi took advantage of the new folks coming in. And without a good online presence i dnt see much future in the gaming space for delta. And hence am nt entering this stock even at present pricing.

Buy Unlisted Shares (11-04-2024)

Is Matrix Gas & renewables shares available in unlisted market. Matrix is one of the company selected under PLI scheme for electrolyser for producing Green Hydrogen. Matrix have recently raised 350 crs from preferential shares where some famous and noted investors have participated like Gunvanth Baid, NAV capital.

Investing stoics (11-04-2024)

I hoped to start my own blog on investing where I work on various topics that can help my readers. I begun 2 months ago but this is my first attempt to publish them on valuepickr

one of my favorites: https://www.investingstoics.com/post/uncovering-opportunities-the-power-of-signalling-theory

Glenmark – Will Innovation Pay? (11-04-2024)

Hi Ranvir, can you please share your views on how you came up with the 14000cr figure for next year, as if I’m not wrong GLS will not be part of the consolidated rev next yr which is currently at an annual rev of approx 2300. I’m just trying to figure out if that is even possible. Thanks!

Anshul’s investing journey (11-04-2024)

I will summarize here, but I will share my thesis and financial model as well.

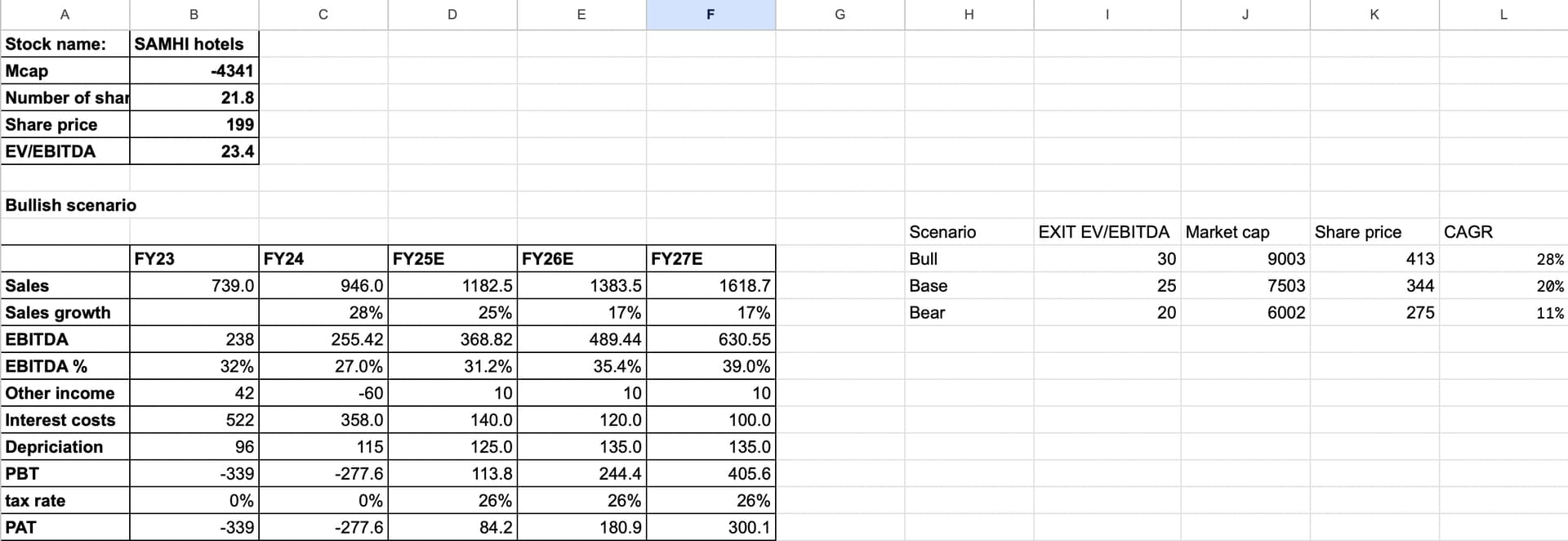

My bet was on the hotel sector, as the demand is increasing while supply will take a few years to catch up. This will lead to operating leverage and excess cash. My bet is that SAMHI will not only become profitable, but also deleverage its balance sheet as sectoral tailwinds are the ideal time to strengthen themselves.

My detailed reasoning

Thesis

Sales growth

FY25 will see addition of around 10-12% more keys which are being added or will get ready from renovation. Moreover, we can expect a RevPAR in double digits, although we are seeing RevPARs in high teen or in the twenties, I don’t know if that can sustain and hence a growth rate of around 13% has been assumed until FY27E

The decline in growth rate from FY26 and FY27 is because not a lot of keys are being added, and we can only expect the newly renovated ones to start(around 900 are under renovation)

EBITDA

The business aims to increase the margins to around 38-40%. Moreover, they shared a chart in one of their presentations that talks of types of costs. 20% was variable and after looking at it, I thought of an additional 20% being semi variable in nature. Despite the fact that semi variable won’t rise as much as revenue, I assumed 60% of the additional revenue each year trickling down to EBITDA.

That is how the model has been made!

Other income

It shouldn’t be negative the next few years because the current year had a one off event and the company took the worst possible scenario and wrote off 70 crores.

Depreciation

It shouldn’t really increase because no keys are being added, only existing portfolio is getting renovated

Interest costs

for FY25, the debt is assumed as 3.7x their EBITDA which is their target. The cost of capital for the business is around 10% and hence the interest cost. Although the management hasn’t guided towards interest cost reduction or anything for FY26 and FY27, the free cash generation does make me believe that a bit of reduction might happen. I have taken a moderate reduction in interest costs post FY25

Va Tech Wabag (11-04-2024)

I think the promoter holding being low has to do with the history of the company. How it diversified from Siemens water business, etc. Comparatively, even Ion Exchange has promoted holding of c. 25% (Comparatively low when compared to other Cos).

I don’t think EMS and Va Tech are true comparables as they both address different markets. EMS is all within India whereas Va Tech gets more than 50% revenue from outside India.

On a related note, you might want to look at corporate governance of EMS. I recollect their DRHP spoke about they being black listed for 2 incidents – 1) inferior quality leading to death of 5 workers and 2) incorrect disclosure for bid. I may be wrong but suggest deep diving into it if you plan to invest in EMS

Walchand Peoplefirst Ltd Dale Carnegie master franchisee (11-04-2024)

The court cases you are referring to are rent disputes, eviction after the lease has expired and other matters.

In case of Walchand Peoplefirst, this plot of land was leased from Mumbai Port Trust in 1936. It is for a period of 99 years. So the lease is valid up to the year 2035.

Many companies which have leased land from Mumbai Port Authority continue to occupy the land despite the lease having expired. The lease which Walchand Peoplefirst has is still current. There is certain rent due which is disputed and shown as a contingent liability in the AR FY23. This amount disputed is shown as a contingent liability of Rs.2.23 crores. This is a small amount given the cash position of the company. It relates to the period 1st Jan 1999 to 31st March 2020. (See pg 42 of the FY23 AR).

There are many precedents of ports having monetized their land. There have been proposals of this sort for Mumbai Port Authority but nothing concrete has materialized.

Some proposals of the past:

Demand to stop eviction and reduce rents (March 2024):

Redevelopment possibility:

[2019]

Whether the proposal which gets finalized benefits the tenants or goes against them is something to be seen.

Smallcap momentum portfolio (11-04-2024)

Don’t you think that it would be risky at this level as you don’t get into cash if it underperform index returns?