i think TAN business is what looks more lucrative to me as mining as a theme will rise in india their tan facility and Consultancy services which they are providing, as discussed in latest concall will be of key competitive edge.

post demerger things will be interesting & i am looking forword to it.

Posts in category Value Pickr

Deepak Fertilizers and Petrochemicals (06-04-2024)

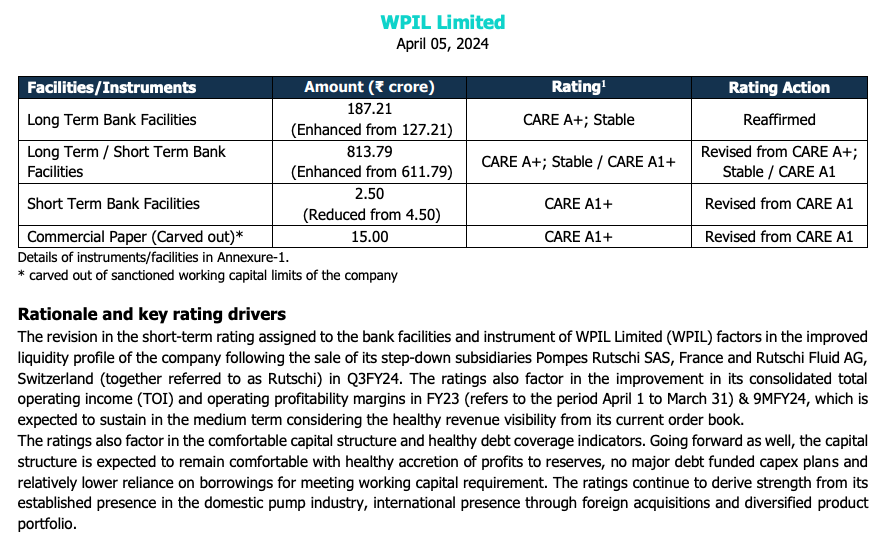

WPIL Ltd – Global Water Pumps (06-04-2024)

WPIL has cost escalation clauses in most of its long-term contracts for supply of engineered

pumps and execution of turnkey contracts

WPIL’s business is inherently working capital intensive with long operating cycle. It receives 10-15% of the contract value on finalisation of design, 50-60% on delivery of pump and the balance on successful erection and commissioning. F

Rain Industries – An oversold de-leveraging play (06-04-2024)

Notes from the Rain Annual Report FY 2023.

- Largest producer of coal tar pitch (CTP) in the world

- 2nd largest producer of calcined petroleum coke (CPC) in the world

- 16 production facilities in seven countries

Calcined petroleum coke (CPC)

- Raw material: Green petroleum coke (GPC) is a byproduct of crude oil refining.

- Mfg process: CPC is produced using rotary-kiln and vertical-shaft technologies in a high- temperature process called calcining, which removes moisture and volatile matter from GPC.

- Use: CPC serves as a crucial raw material for anodes used in primary aluminium production as well as in the steel and titanium dioxide industries.

Coal tar pitch (CTP)

- Raw material: Coal tar is a byproduct of metallurgical coke used in the iron and steel industries.

- Mfg process: CTP is produced by distilling of coal tar, which separates the components based on different boiling points.

- Use: CTP is a critical raw material for anodes used by the aluminium industry, as well as in the graphite and refractory industries.

Cement

- Brand Priya Cement

- Started selling loose cement

Vice Chairman’s statement

- RAIN’s business model converts byproducts into essential raw materials.

- Historically, finished goods prices lead raw material prices, allowing for higher margins during market rises.

- And lower margins seen in falling markets.

- But keeping our margins within a general range as the markets move through cycles.

- Exceptionally long market rise experienced during the 18-month post-COVID (late 2021 to early 2023)

- Led to new market highs and unsustainably strong 2022 performance.

- 2023 saw significant margin decline due to slow drop in raw material prices following a sharper finished product price fall.

- Stabilization of downturn may take over 12 months which is longer than usual.

- RAIN historically faces challenges after strong years.

- Current downturn expected to last 1-2 more quarters.

- Price stabilization for both raw materials and finished goods anticipated.

- Significant operational improvements anticipated across segments following price stabilization.

- RAIN’s India calcination plants previously operated at low capacity due to GPC import restrictions.

- Recent relaxation of GPC and CPC imports by CAQM (Commission for Air Quality Management) allows for increased capacity utilization.

- Expects higher capacity to significantly improve overall performance.

- Increasing demand for CPC in and around India.

Outlook:

-

Carbon Segment:

- Increased capacity utilization due to relaxed GPC import restrictions.

- Positive outlook due to rising demand for primary aluminum in:

- Infrastructure development (emerging economies)

- Lightweight vehicle manufacturing

- Electric vehicles & renewable energy

-

CPC Outlook

- 85% CPC sales comes from primary aluminium smelters

- Despite short-term challenges, the long-term outlook for aluminium remains optimistic.

- Primary aluminium smelting remains the key driver of the world’s CPC and CTP sales.

- Smelter production reached record levels in 2023 despite a challenging economic environment.

- CPC products serve the titanium dioxide (TiO2) industry, primarily used in paints.

- TiO2-related CPC volumes faced challenges due to slowing construction activity, growth is likely as economic outlooks improve.

-

Advanced Materials Segment:

- Economic recovery expected across end-user industries.

- Growing demand for bio-based & eco-friendly product lines.

- Promising future growth in battery anode materials.

-

Cement Segment:

- Cement demand rebounded strongly in 2023, growing by 7 – 8% on a per annum

- Rising infrastructure development & government initiatives.

- Expected Indian cement demand increase to 525 MNTPA in 5 years.

Capacity utilisation

- Carbon: 65%

- Advanced Materials: 75%

- Cement: 80%

Misc

- No planned major capex projects for 2024

- Cash from ops: Rs 3,063 crore

- Rs 1,391 cr of cash freed from inventory reduction

- Cash up from Rs 1,167 cr last year to Rs 1,405 cr

- Trading below book value. But it always has.

JTL Industries – Fast Grower at an inflexion point (06-04-2024)

Recently I got a call from there IR stating that there is being investor survey going on as they have on boarded gensol as there new client but idk why they are trying to sell the story so much I believe that the company is fundamentally strong the. Why they are selling this all?

Force Motors – racing ahead! (06-04-2024)

Also this time they released the data 24 hrs in advance

Security and Intelligence Services (India) Limited (05-04-2024)

Investment in emoha senior is also a very good move. More investment woukd have been better (5% is too low)

Security and Intelligence Services (India) Limited (05-04-2024)

Investment in emoha senior is also a very good move. More investment woukd have been better (5% is too low)

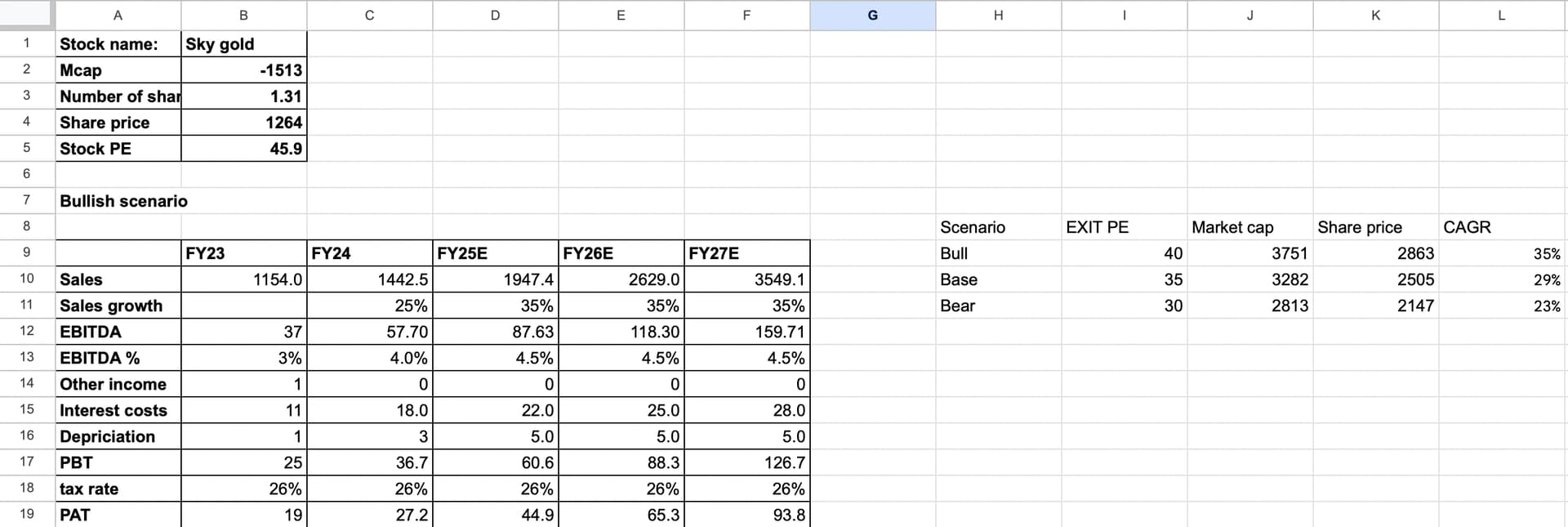

Sky Gold ltd. – Will it reach the sky? (05-04-2024)

Not a buy or sell recommendation. Disc: Bought in the last 30 days

Here is my thesis

Thesis

About the business

Sky gold is a B2B business that manufactures designs for jewellery retailers like Malabar, Kalyan etc.It is a proxy to the gold jewellery and is mainly catering to the domestic market, however they are in talks to produce for retailers in Malaysia and some gulf countries as well.

Revenue growth

The company produced around 250-300 kgs per month of gold jewellery before the factory, but they have recently moved to a much bigger facility which should produce around 700-800 kgs per month. The company, according to the guidance of the promoters, should reach 5000 crores by FY26, which basically means the business starts functioning at full capacity.

Honestly, I found that number too stretched, however found data point where organised manufacturing only has a 15% market share, which is quite less compared to organised retail and hence this will need to catch up to the organised market share of the retail jewellers. Yet, i did not want to aggressive and have used a 35% growth from FY25( 35% seems big but knowing the story and plans in place by the company, it might just happen)

Ebitda

Since it’s down the value chain, we can’t expect them to have Operating margins of retail businesses we have studied. Due to the fact that they are expanding almost 4x, The company believes a 5%+ margin is possible. However, due to the nature of the business and the fact that competition is only going to get tougher, I am assuming a 4.5% margin which is what they have been doing for the past few quarters

Depreciation and Interest costs

The capex required isn’t much and hence depreciation too won’t be very significant. The interest costs should rise, however not as much as the revenue growth because of a number of measures regarding their contracts with customers, starting the use of Gold metal loan, reducing working capital days and not holding gold bullion inventory by just taking them from customers.

Possible antithesis

• Concentrated customers: top 10 make 70% of their revenue and hence any potential loss of customers could be a big blow. However, they are very close to signing Tanishq and hence it could be negated

• The business has a negative CFO at the moment, however it is mainly due to the working capital pressure which came from the aggressive growth, the promoters said that they should be cash flow positive due to the transition being complete and the measures being taken to reduce working capital. However, I would still wanna observe and see how this aspect turns out.

• The data found is extremely limited, and hence the corporate governance could be questionable.

• Valuations: Even though the growth promised is really good, I would want to wait for at least a 10%-15% correction to increase the margin of Safety.( we got this correction in the recent fall)

Sky Gold ltd. – Will it reach the sky? (05-04-2024)

Not a buy or sell recommendation. Disc: Bought in the last 30 days

Here is my thesis

Thesis

About the business

Sky gold is a B2B business that manufactures designs for jewellery retailers like Malabar, Kalyan etc.It is a proxy to the gold jewellery and is mainly catering to the domestic market, however they are in talks to produce for retailers in Malaysia and some gulf countries as well.

Revenue growth

The company produced around 250-300 kgs per month of gold jewellery before the factory, but they have recently moved to a much bigger facility which should produce around 700-800 kgs per month. The company, according to the guidance of the promoters, should reach 5000 crores by FY26, which basically means the business starts functioning at full capacity.

Honestly, I found that number too stretched, however found data point where organised manufacturing only has a 15% market share, which is quite less compared to organised retail and hence this will need to catch up to the organised market share of the retail jewellers. Yet, i did not want to aggressive and have used a 35% growth from FY25( 35% seems big but knowing the story and plans in place by the company, it might just happen)

Ebitda

Since it’s down the value chain, we can’t expect them to have Operating margins of retail businesses we have studied. Due to the fact that they are expanding almost 4x, The company believes a 5%+ margin is possible. However, due to the nature of the business and the fact that competition is only going to get tougher, I am assuming a 4.5% margin which is what they have been doing for the past few quarters

Depreciation and Interest costs

The capex required isn’t much and hence depreciation too won’t be very significant. The interest costs should rise, however not as much as the revenue growth because of a number of measures regarding their contracts with customers, starting the use of Gold metal loan, reducing working capital days and not holding gold bullion inventory by just taking them from customers.

Possible antithesis

• Concentrated customers: top 10 make 70% of their revenue and hence any potential loss of customers could be a big blow. However, they are very close to signing Tanishq and hence it could be negated

• The business has a negative CFO at the moment, however it is mainly due to the working capital pressure which came from the aggressive growth, the promoters said that they should be cash flow positive due to the transition being complete and the measures being taken to reduce working capital. However, I would still wanna observe and see how this aspect turns out.

• The data found is extremely limited, and hence the corporate governance could be questionable.

• Valuations: Even though the growth promised is really good, I would want to wait for at least a 10%-15% correction to increase the margin of Safety.( we got this correction in the recent fall)