May be if the trend continues for the next 6-8 quaters then we can then assume a change in the travel habits.

Also, a new trend in the travel industry is paying the trip expense in EMI format and easy personal loans available for this.

May be if the trend continues for the next 6-8 quaters then we can then assume a change in the travel habits.

Also, a new trend in the travel industry is paying the trip expense in EMI format and easy personal loans available for this.

I was going through the earnings call and there are a few observations, can someone confirm that my understanding is correct?

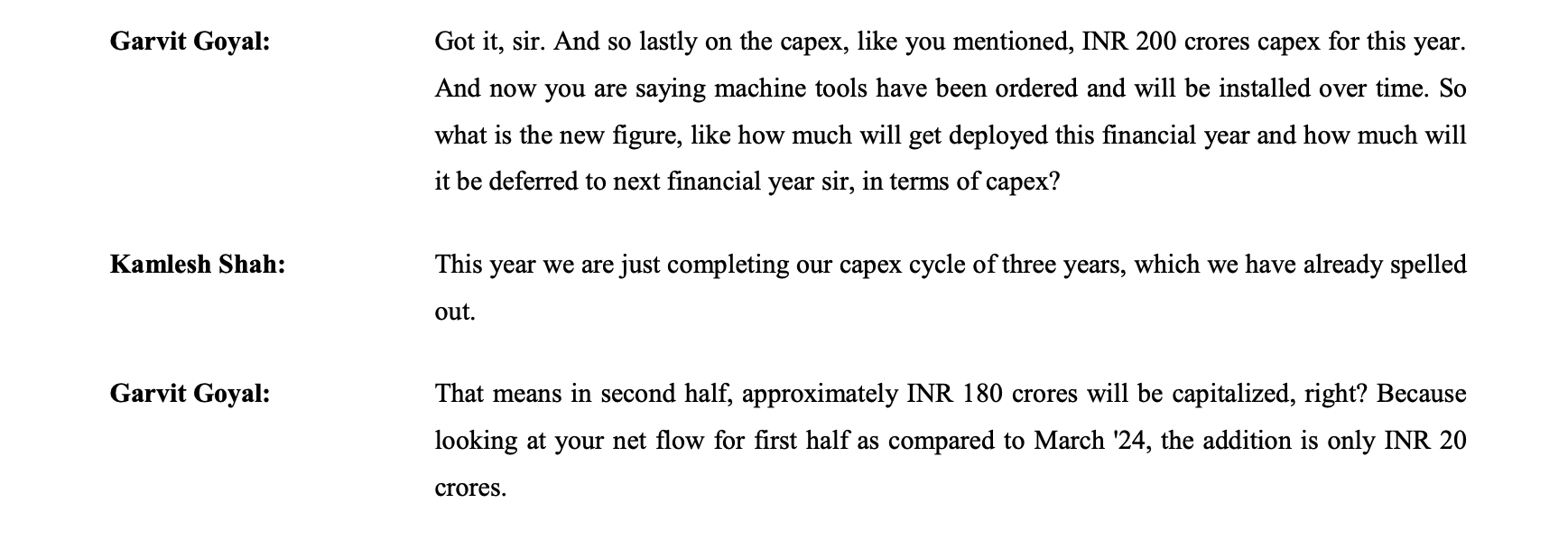

Mr Pratik Kothari here asks about the capex plan of 200 Cr of which only 40Cr has been done YTD. The answer is not very clear to me, what I understand that they have already placed the order (so essentially capex is done) but it is not yet recorded in the books as equipment isn’t delivered yet (accruals basis of accounting).

Mr Garvit goyal, here follows up on the question to get more clarity and, IMO, the Mr Kamlesh isn’t making it easy to understand with his response.

Fortunately, Mr Garvit is persistent to get clarity, and asks if 180 Cr is supposed to get capitalised. (Which, as I understand, will be added to the books as assets once the orders are delivered.) To which, Mr Kamlesh answers Yes.

Overall, I felt that answers from Mr. Kamlesh weren’t very clear and it felt like he was trying to hide something. Or maybe, I don’t understand the jargon very well and reading too much into it. Is my understanding correct? Can someone throw some light here?

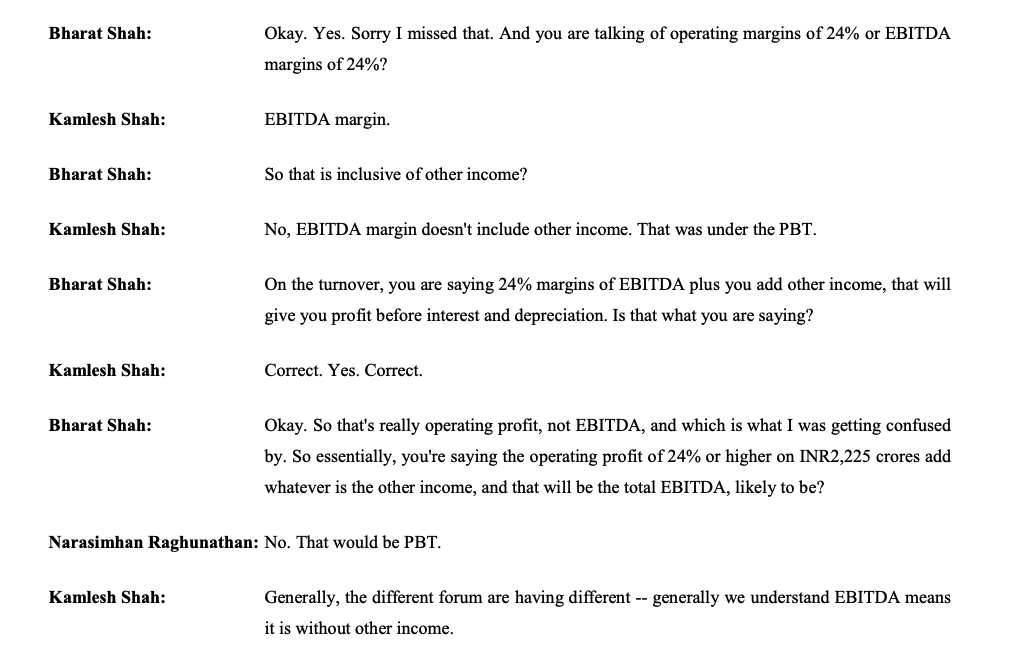

In my defence, Mr Kamlesh was earlier fumbling with Operating Margin and EBIDTA margin, so I am a bit skeptical about his answers.

Marsons Ltd. 1st presentation:

Dynamic Cables, 1st Concall, Here’s the Transcript:

1st Ever Presentation by a Nanocap, Remi Edelstahl Tubulars:

Effwa Infra:

https://nsearchives.nseindia.com/corporate/EFFWA_25102024014153_EffwaInfraInvestorPresentation.pdf

Perhaps because holding company has reverse merged into the bank.

need the full transcript, please share if you have it with you

I think they are going the right way and building capex as per the requirements once the already built capex is ensure to run with optimum capacity and have good order book in hand rather than going bust during some slow down… We have seen many a times in past in other industries like chem pharma very recently.

Kotak Mahindra Bank –

Q2 FY 25 concall and results updates –

Deposits – 4.46 lakh cr, up 16 pc YoY

Breakup of deposits –

Current account – 61.8k cr, up 6 pc

Savings account – 1.24 lakh cr, up 2 pc

Term deposits – 2.59 lakh cr, up 26 pc

CASA ratio @ 43.6 pc

Cost of funds @ 5.15 vs 4.78 pc YoY

CASA + Term Deposits < 5 cr constitute 79 pc of deposits

Total customers on 30 Sep @ 5.2 cr vs 4.6 cr YoY

Assets ( loans ) – 4.5 lakh cr, up 18 pc YoY

Breakup of assets –

Home loans + LAP – 1.16 lakh cr, up 18 pc

Business banking – 40k cr, up 21 pc

Personal loans + Consumer durable loans – 20.8k cr, up 17 pc

Credit cards – 14.4k cr, up 15 pc

CV + CE loans – 39k cr, up 26 pc

Agri Loans – 26.9k cr, flat YoY

Tractor finance – 16.1k cr, up 13 pc

Retail Microfinance – 9.7k cr, up 21 pc ( however, it was down QoQ )

Commercial loans – 91.9k cr, up 14 pc

Corporate loans – 92.8k cr, up 13 pc

SME – 32.1k cr, up 31 pc

Others -10k cr, up 33 pc

Credit substitutes – 30.9k cr, up 32 pc

Gross NPAs – 1.49 vs 1.72 pc ( @ 6033 vs 6087 cr )

NNPAs – 0.43 vs 0.37 pc ( @ 1724 vs 1275 cr )

Total provisions @ 6266 vs 6721 cr

Slippages in Q2 @ 1875 cr vs 1314 cr YoY

Upgrades and recoveries @ 681 vs 942 cr

Write Offs @ 638 vs 194 cr

P&L for the bank ( standalone ) –

NII – 7020 cr, up 11 pc

Other Income – 2684 cr, up 16 pc

Net total income – 9704 cr, up 13 pc

Operating expenses – 4605 cr, up 15 pc

Operating profits – 5099 cr, up 11 pc

Provisions – 660 cr, up 80 pc

PAT – 3344 cr, up 5 pc

Kotak AMC –

AUM @ 4.73 vs 3.36 lakh cr

PAT @ 197 cr, up 58 pc

Monthy SIPs ( in Sep 24 ) @ 1764 cr, up 23 pc YoY

Kotak life Insurance –

PAT @ 360 cr, up 106 pc

Kotak Prime –

PAT @ 269 cr, up 29 pc

Kotak Securities –

PAT @ 444 cr, up 37 pc

International Subsidiaries –

PAT @ 76 cr, up 84 pc

Kotak Investments –

PAT @ 141 cr, up 12 pc

Kotak capital company –

PAT @ 90 cr, up 233 pc

Consolidated profits @ 5044 cr, up 13 pc YoY

Bank expects to keep exercising caution on MFI loans. Expect this trend to continue for another 2-3 Qtrs before getting back to growth path again

Credit card business has been impacted by the Ban imposed by RBI on issuance of fresh cards

Consol ROE @ 13.88

Consol ROA @ 2.53

Share of profits of subsidiaries stands @ 33 pc

Embargo on issuance of fresh credit cards + bank going slow on the MFI business resulted in NIM compression in Q1

With the ongoing festive season + pickup in Govt spending in H2, bank expects pickup in the economy in H2. This should be positive for their CV+CE + tractor finance – lending business

Mid-Corporates and SME segments continue to grow strongly. Large corporate segment is seeing irrational pricing

Kotak AMC’s mkt share now stands @ 7.1 pc with an AUM of 4.7 lakh cr. Their retail AUM stands @ 60 pc

Bank believes that the trend of higher slippages should play out over next 2 Qtrs after which it should again start to fall. They have taken a lot of actions on the credit card and micro finance side to ensure that this happens

Mid-Corporates and SME segments continue to grow strongly. Large corporate segment is seeing irrational pricing

On 18 Oct, the Bank announced acquisition of personal loan book ( of 4100 cr ) of standard chartered bank. These are all standard loans of affluent customers. It also gives them access to 95k new affluent customers ( avg personal loan per customer works out to be around 4.3 lakh )

Currently, Bank’s unsecured book stands @ 11 pc of loans. They intend to take it to mid teens levels. This will help them achieve better margins and accelerate their growth

Bank is hopeful of greater recoveries in Q3, Q4 ( from the secured book ) which should help them reduce their net slippages in H2

Bulk of the slippages are happening in the Credit Card + MFI business. And that’s the nature of business

Disc: holding, biased, not SEBI registered, not a buy/sell recommendation

Hi, The details on NCGTC (Background) for CGFMU states the following which is different than what you have assumed.

“Guarantees for loans up to the specified limit (currently Rs.10 Lakh) sanctioned by Banks / NBFCs / MFIs / other financial intermediaries engaged in providing credit facilities to eligible micro units. Further, Overdraft loan amount of Rs.10,000 sanctioned under PMJDY accounts shall also be eligible to be covered under Credit guarantee Fund.”

Further, the investor presentation slides, slide 4, mentions that the 50% of their MFI loan book is insured and not that CGFMU insures 75% of the loan book. They have just said that 75% of their loan book will be insured especially because loans issued after Jan 24 will be insured by CGFMU upto the limit mentioned above.

Or am I misconstruing your comment?

I would agree with Sahil, even Ashwath Damodaran has change his views on Zomato valuation now

(post deleted by author)