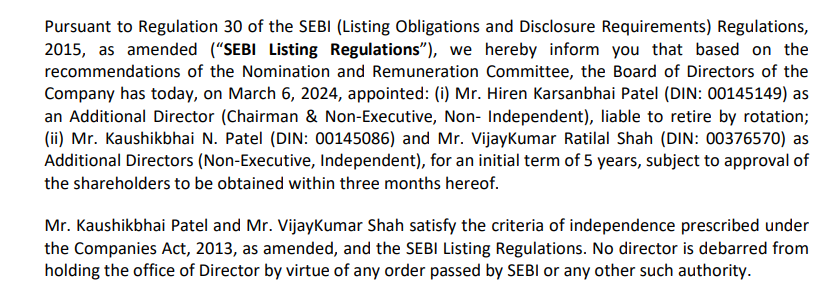

Along with the old promoter, one “independent” director exits

and two new “independent” directors belonging to the new promoter join the Board. Nice! ![]()

Source:

Along with the old promoter, one “independent” director exits

and two new “independent” directors belonging to the new promoter join the Board. Nice! ![]()

Source:

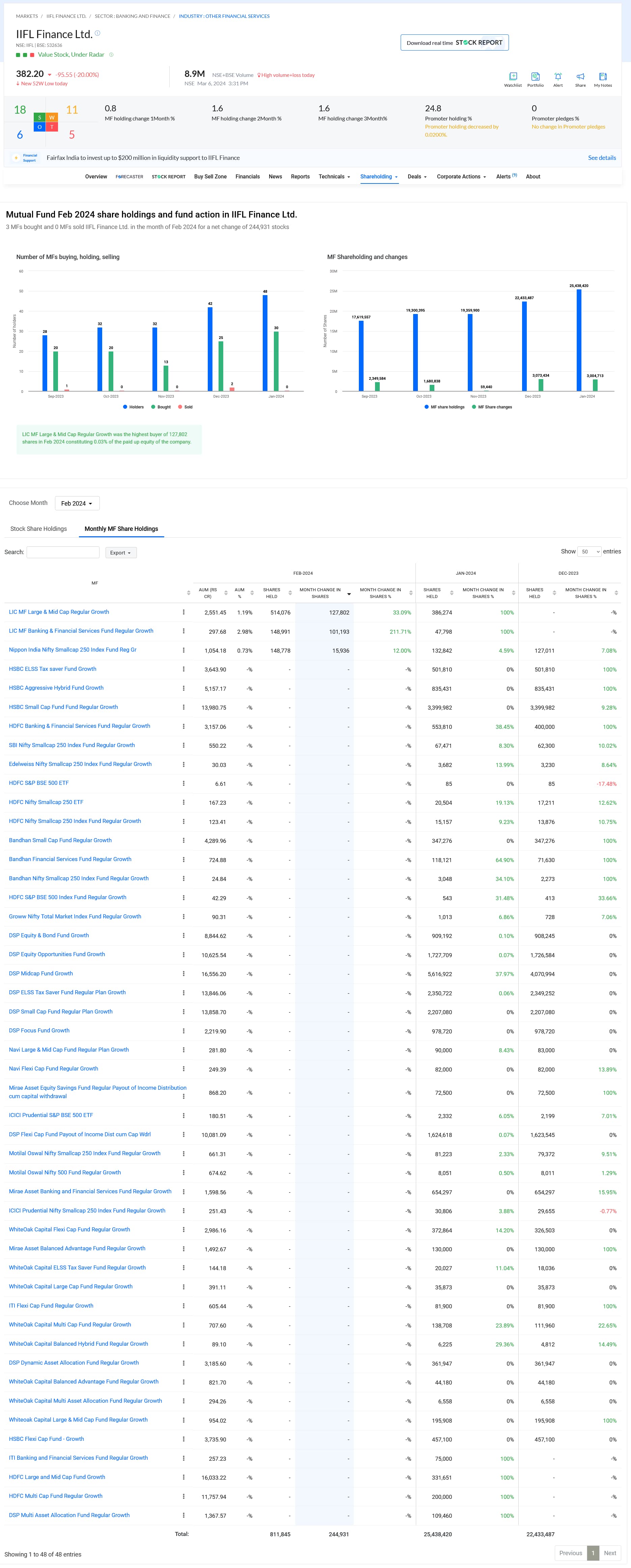

Here is the full page of what you have posted from Trendlyne.

From the same page

Mutual Fund Feb 2024 share holdings and fund action in IIFL Finance Ltd.

3 MFs bought and 0 MFs sold IIFL Finance Ltd. in the month of Feb 2024 for a net change of 244,931 stocks

Not invested in IIFL.

Thanks for the info Ayan… fully agree with you.

I beefed up my position in NH, and hopefully the issue is transient and awaiting clarity from Health Ministry.

Anyways, this recent correction is a fantastic opportunity to accumulate a multi-year growth play, with excellent execution track record and transparent management.

Disclaimer: NH is now a top holding in my portfolio

I know that Rupeevest is yet to come up with Feb data.

And even Value Research data is also getting changed. The current shares in regular funds are shown as 47,19,11,022, which is different from the screenshot you have posted for Reliance, and this can change in 12 hours. So, Feb data AFAIK, is yet to come in completely.

IIFL’s data from Value Research shows just Groww’s Total Market Index fund’s shares, which have increased. There are other Nifty 500 and small cap indices’ funds from other fund houses like Nippon, Motilal, SBI, ICICI, HDFC, Edelweiss whose AUM is more than Groww, so if Groww had bought, they must have bought too.

So I don’t think the data for Feb has completely come yet, and if funds had exited yesterday and tomorrow, complete data like this will be available after a month.

Not invested in IIFL.

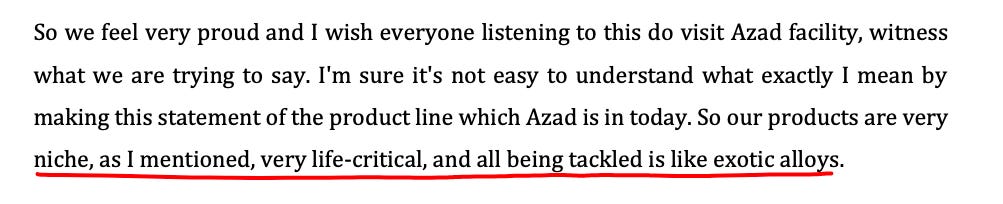

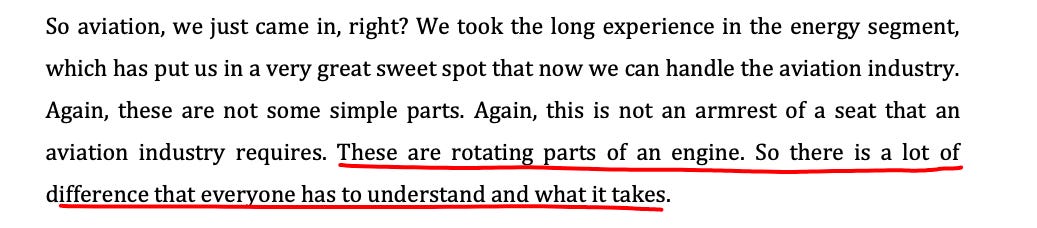

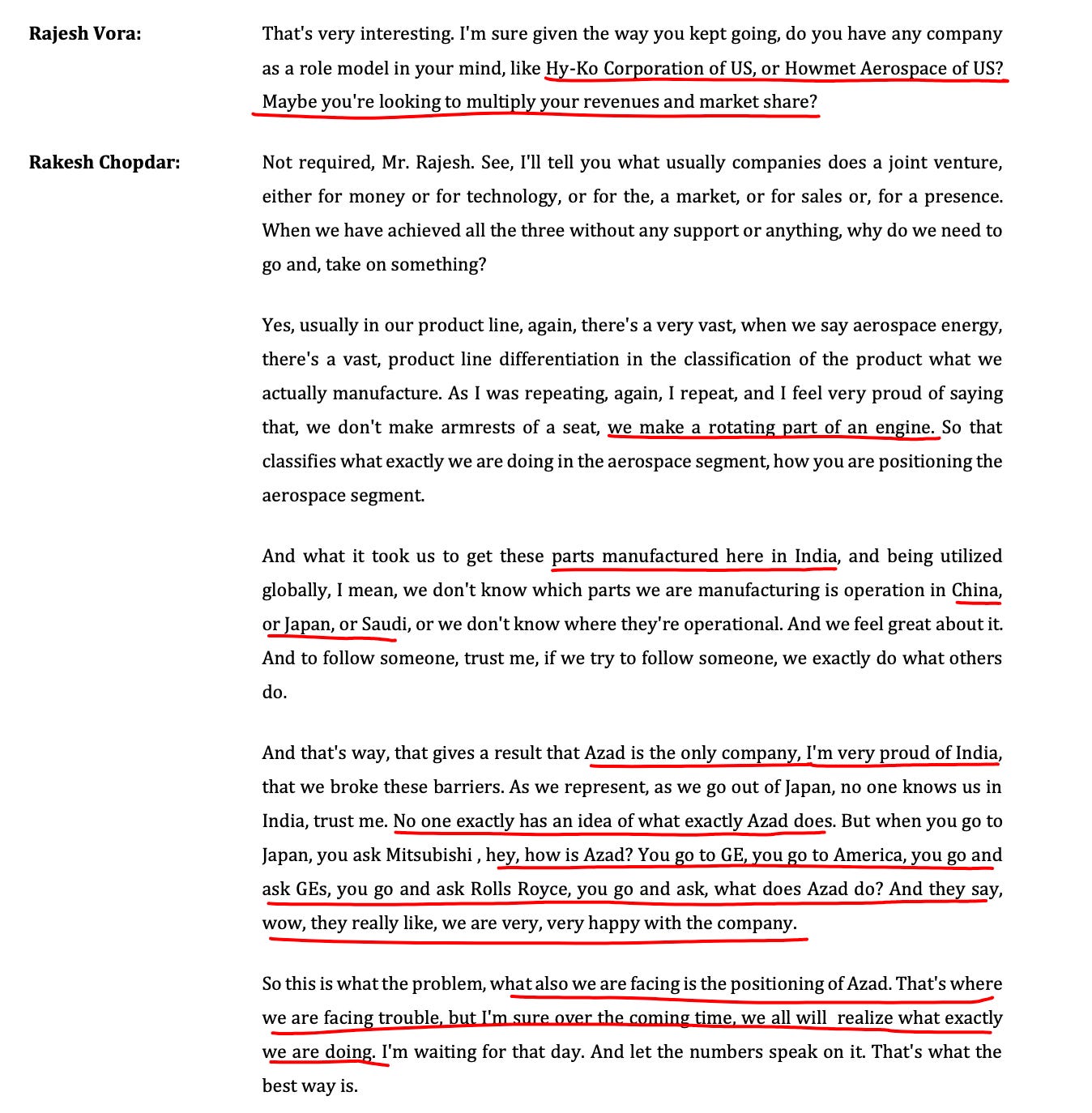

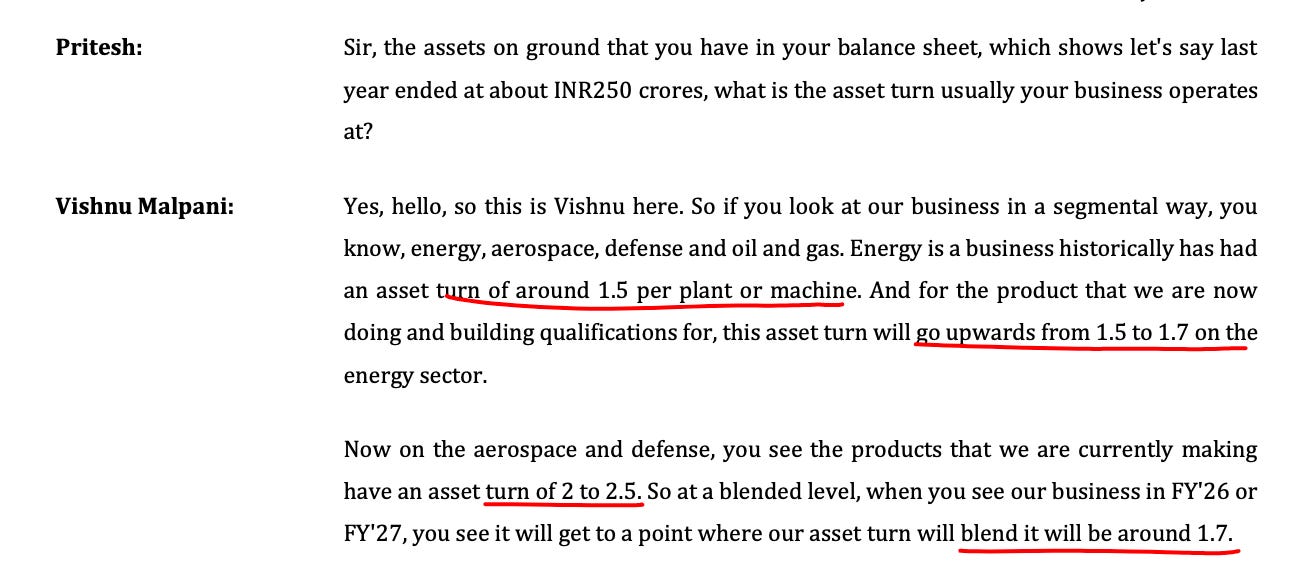

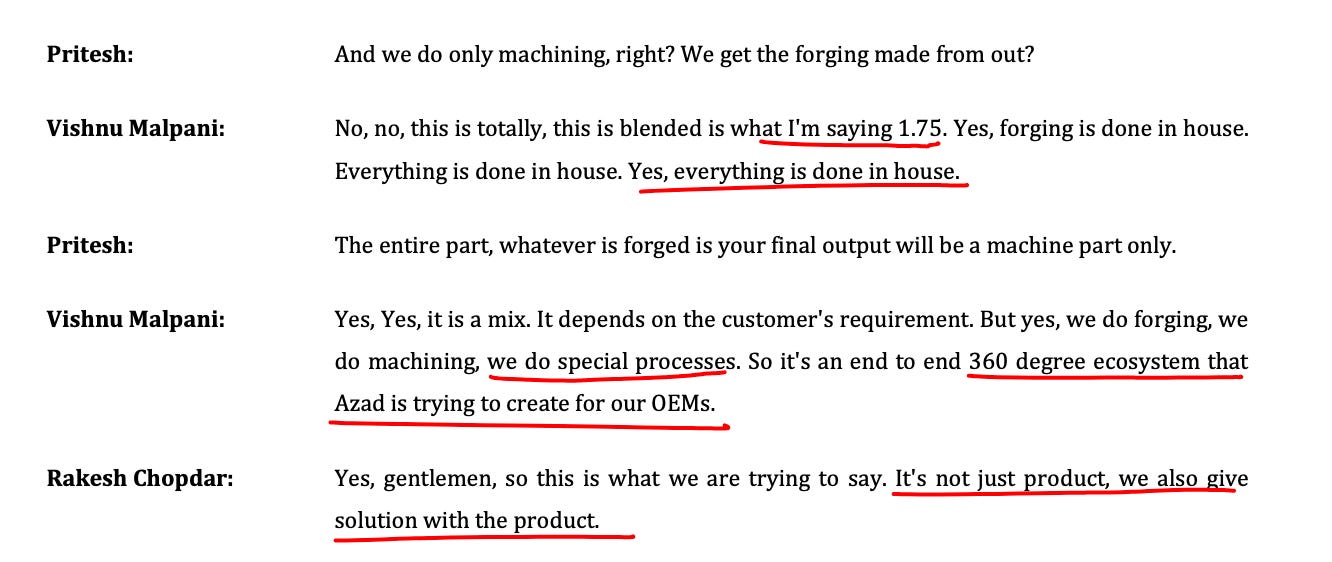

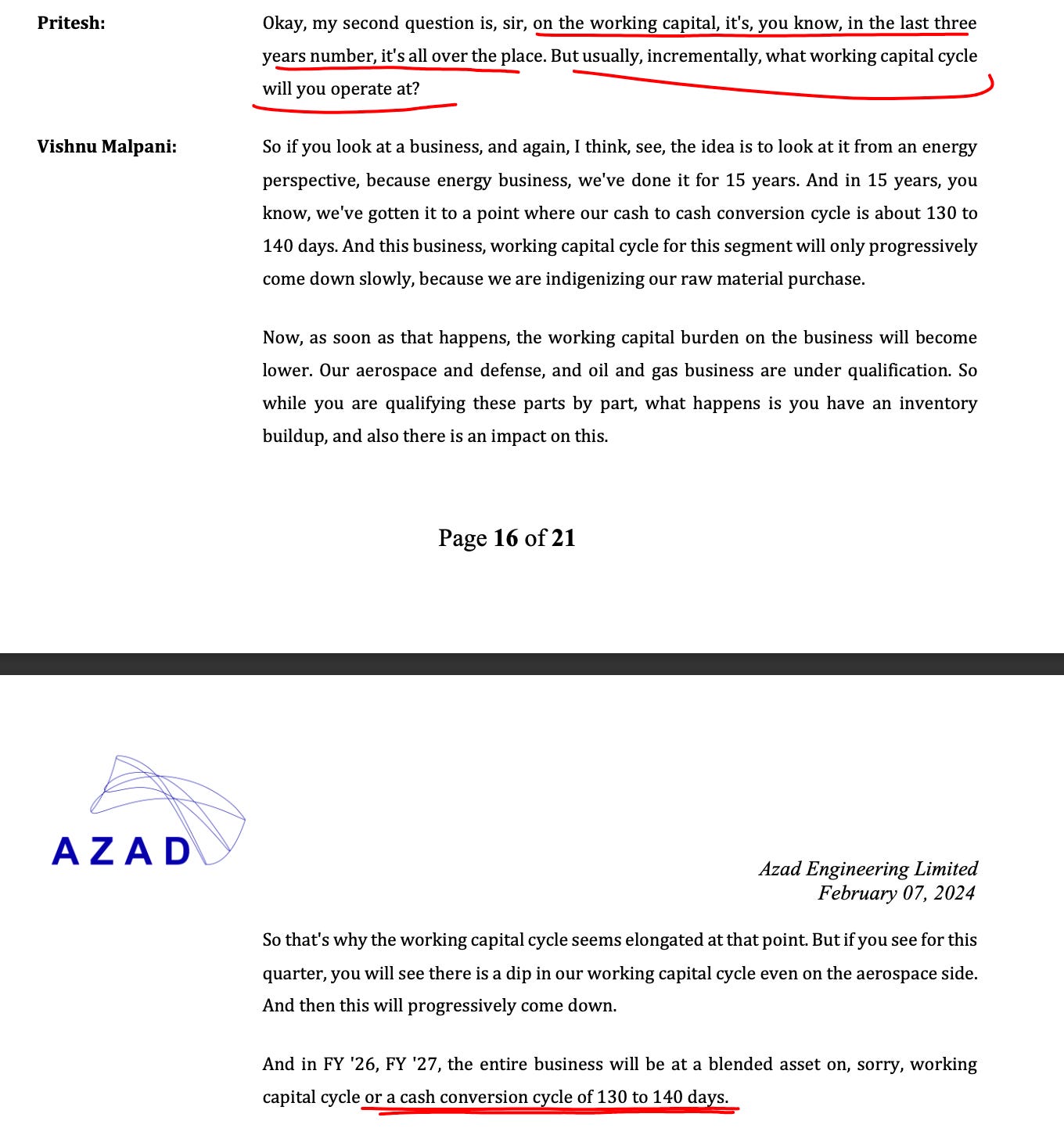

Highlights and notes from the conference call that raised concerns.

Opening remarks

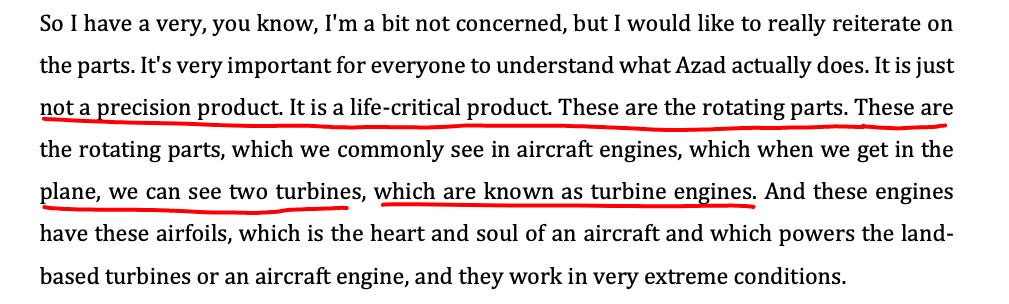

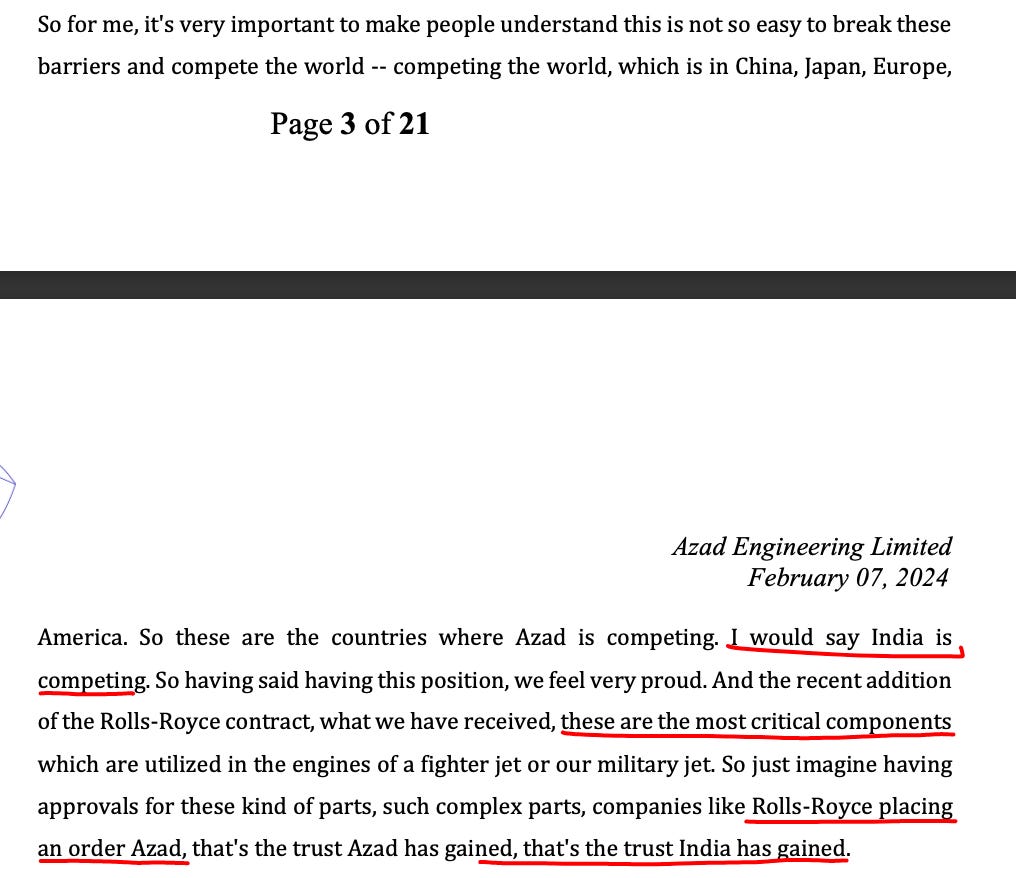

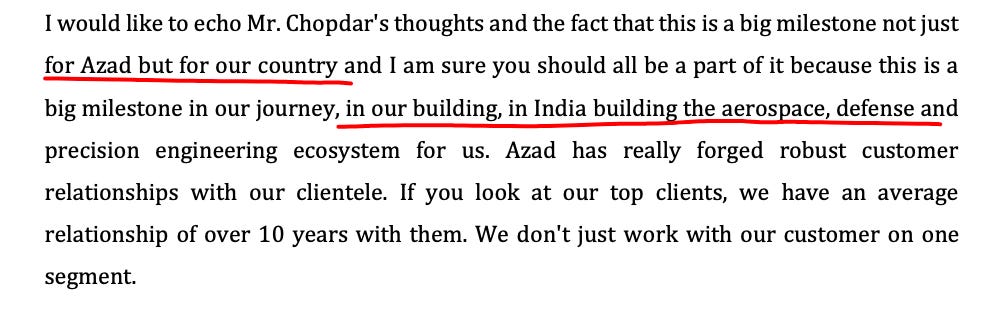

The CEO repeatedly emphasizes that they manufacture a “mission-critical,” “life-critical” product for turbines operating at 30,000 feet, making India proud or proudly manufactured in India. He concludes by suggesting that the current financials/profitability might appear deceptively inexpensive and shouldn’t be over-interpreted.

Remember the movie Drishyam?

Illusion of truth?

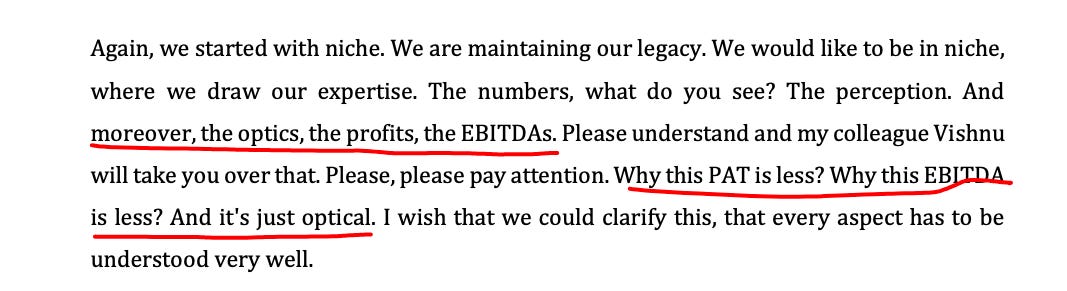

Analyst Q&A:This is where things start to get interesting

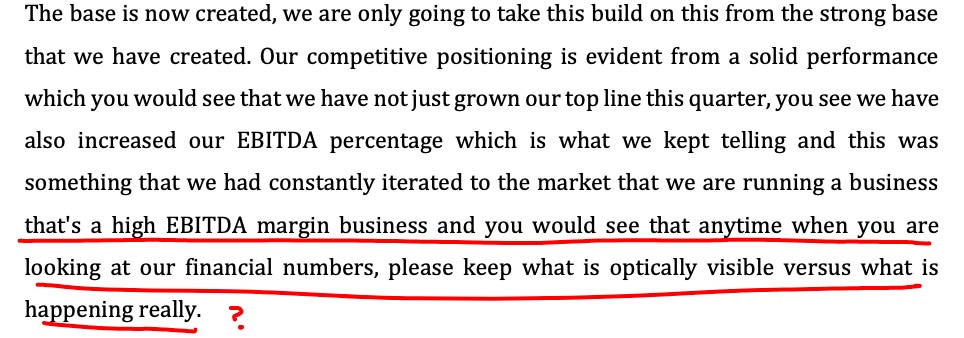

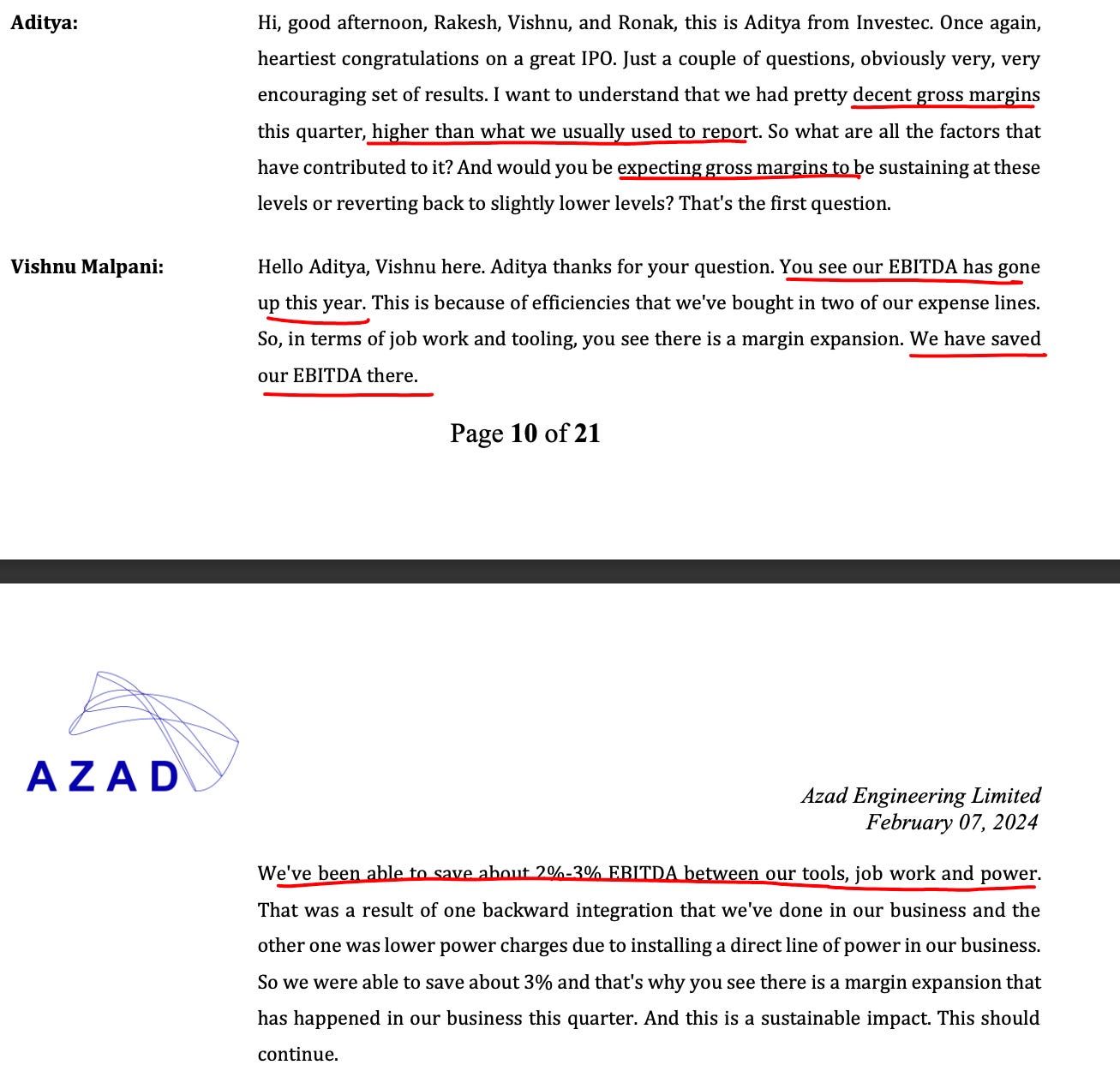

The CFO was asked about Gross Margin, but he repeatedly discussed EBITDA margin. Even the comments on EBITDA lacked substance.

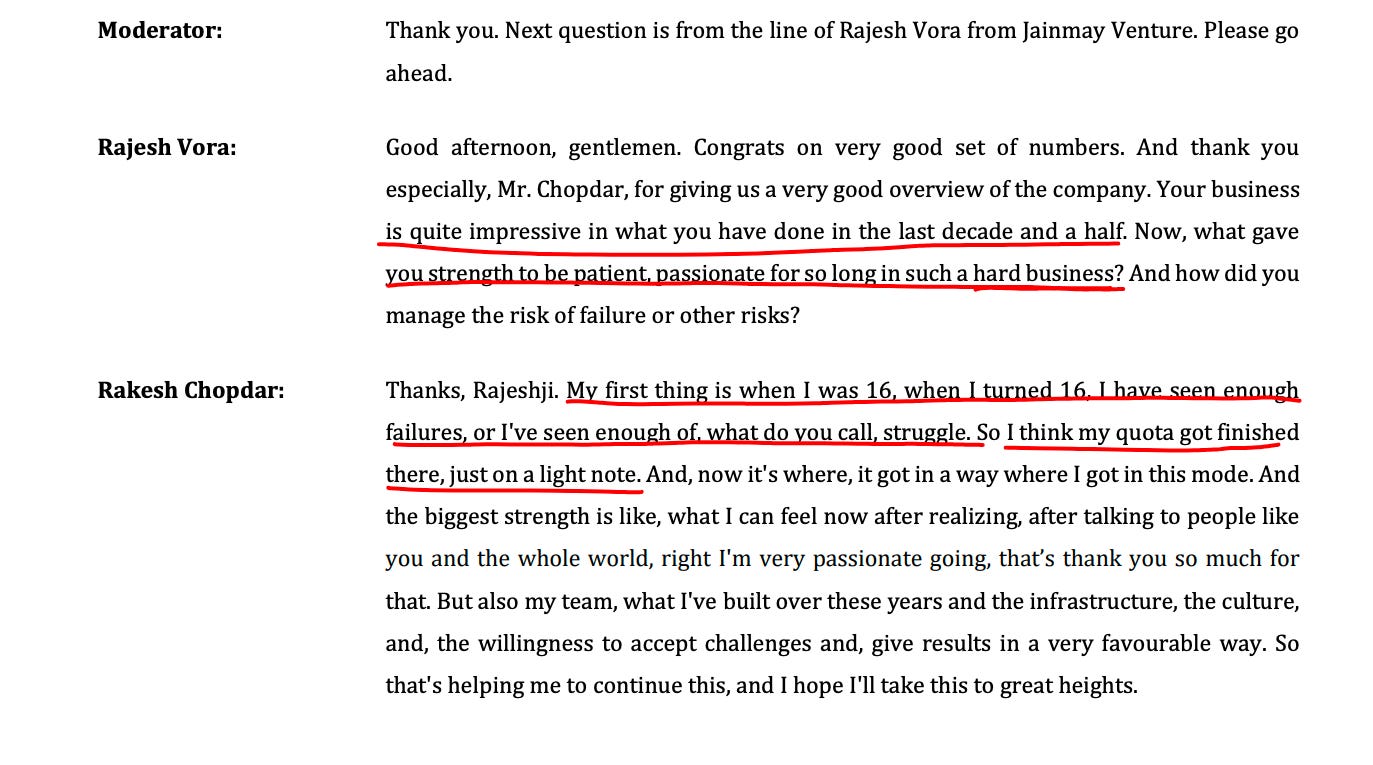

This is really odd: Why would an analyst/investor act like an appointed cheerleader? And yet again, the promoter seizes the opportunity to reinforce the Halo effect.

Cheerleading continues: Creating an illusion/hope by drawing parallels with the best in business. Moreover, promoter continues bragging (and needless mentions of its relation to India) to fuel the availability heuristic and establish correlation where none exists.

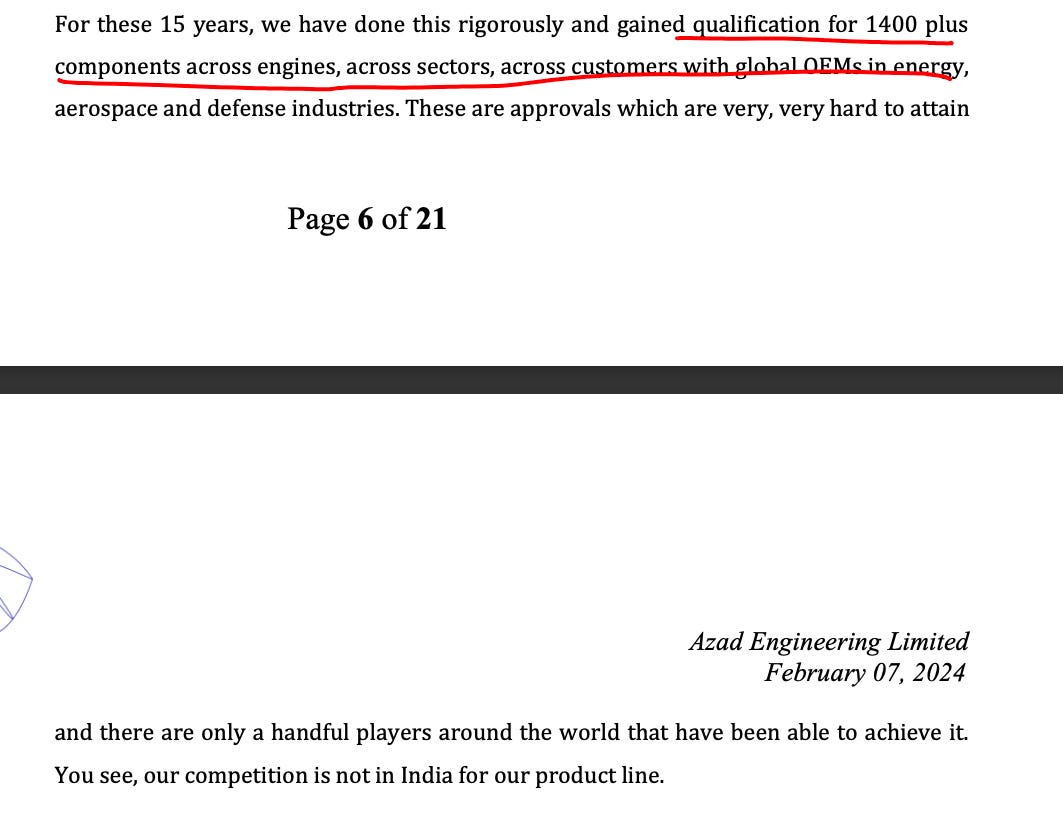

Oddness continues: Vague response to a sensible question from Ashish Kacholia’s team

Tall claim, isn’t it?

My take on Azad Engineering

In 2015-16, while working on a consulting project for a Fortune 500 parts manufacturer, I acquired limited knowledge of the A&D industry, procurement processes, and supply chain strategies.

Disclaimer: My analysis may be biased and potentially overly critical. Nonetheless, if their claims turn out to be true , this could represent a solid investment opportunity.

However, I remain cautious due to the lack of evidence supporting Azad Engg.’s valuation comparable to that of a Tier-1 A&D comps.

For a company to warrant such premium in valuation, it must possess a robust competitive advantage, advanced technology, and foreseeable high growth in the near term, among other factors.

After reading the IPO Prospectus and recent quarterly earnings transcript, I was reminded of this hilarious scene from “Andaz Apna Apna”.

Throughout the content, I sensed inconsistencies and potential red flags. See Part 3 for my detailed notes.

I’ll take a stab at and challenge the following criteria for a company to command a premium valuation.

Is there any fundamental value to this company beyond simply riding the wave of overvaluation in A&D+small/mid cap space?

I don’t have a clear answer yet, but I suspect the following heuristics/biases might be playing a role:

“Repeat a lie often enough and it becomes the truth.”- Nazi Joseph Goebbels

Excessive repetition of “mission-critical” and “life-critical” product applications without specific details to make investors believe so without questioning any further. (Details in part 3)

The promoter’s dropout status attracts attention, but can it ensure efficient management of a complex manufacturing business?

I have the utmost respect for all the sports personalities mentioned below, and I have no doubt about their skills and temperament in their respective sports.

My BS detector advises me to ignore the noise generated by celebrity investors. While celebrities may not intend harm, the media’s hunger for news often magnifies get-rich-quick schemes.

Another cheap signal fueling the confirmation bias: Marquee names in the anchor book

Second-level thinking, as advocated by Howard Marks, is key to dealing with noise (and BS)

First-level thinking : Many prominent names have invested, so they must have done their due diligence.

Second-level thinking:1 Institutions are also susceptible to biases. Rs. 220 crore is small change given the size of these funds. Hence, I must ignore this noise and think independently.

I’m sure this isn’t the first occurrence, and me-too companies often capitalize on hype during bull markets.

Second-level thinking is crucial – prioritize fundamentals over hype and independent analysis over celebrity endorsements.

Read more here

Nirma Limited is officially the new promoter of GLS after GPL transferred 55% stake to Nirma. Remaining 20% stake will be transferred soon and then the process of sale will be complete.

Nirma Limited is officially the new promoter of GLS after GPL transferred 55% stake to Nirma. Remaining 20% stake will be transferred soon and then the process of sale will be complete.

Minda recently got clearance/approval from CCI for buying stake again. How do you think event will impact Pricol?

Disc: holding from 2 digit levels.

Minda recently got clearance/approval from CCI for buying stake again. How do you think event will impact Pricol?

Disc: holding from 2 digit levels.